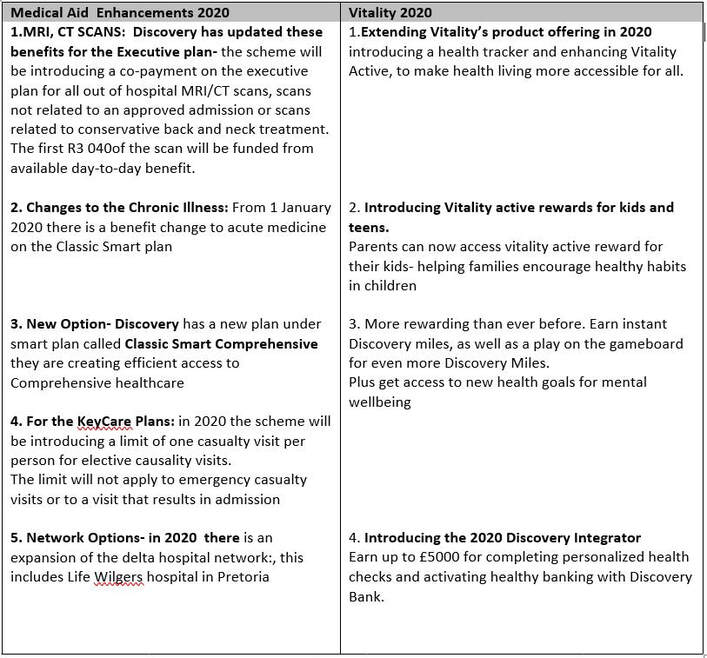

Sirago has some great great updates and additions in 2020 which are:

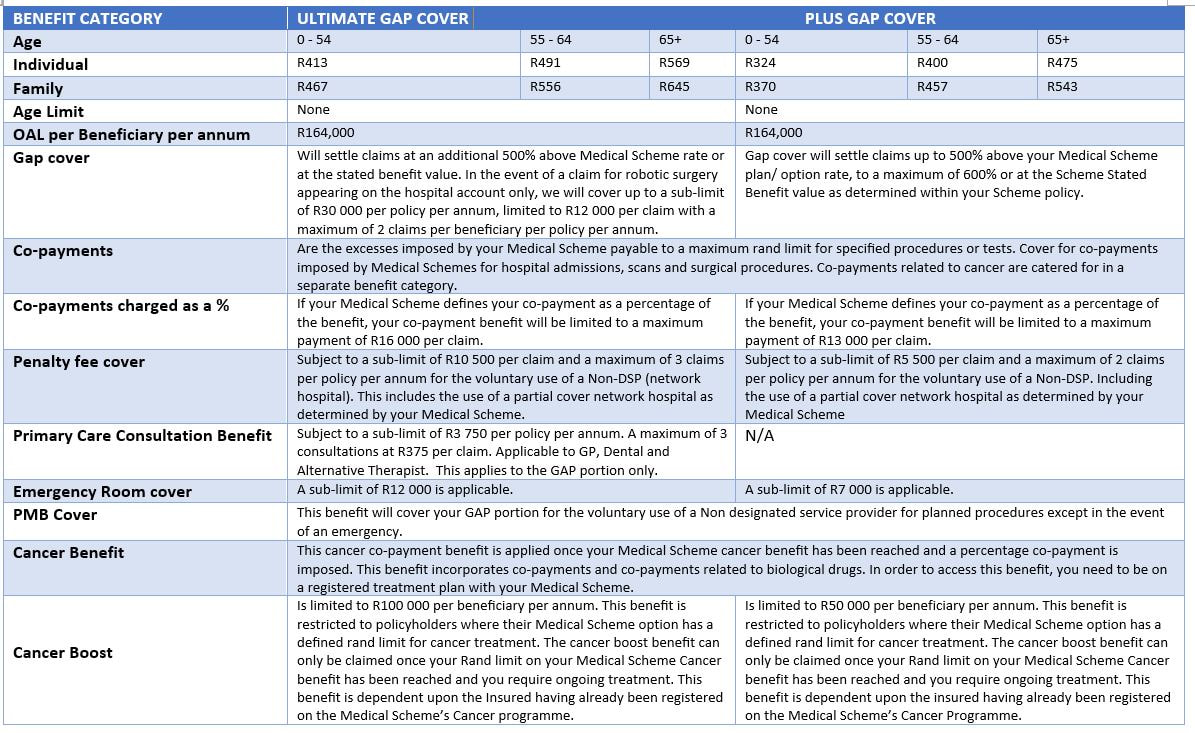

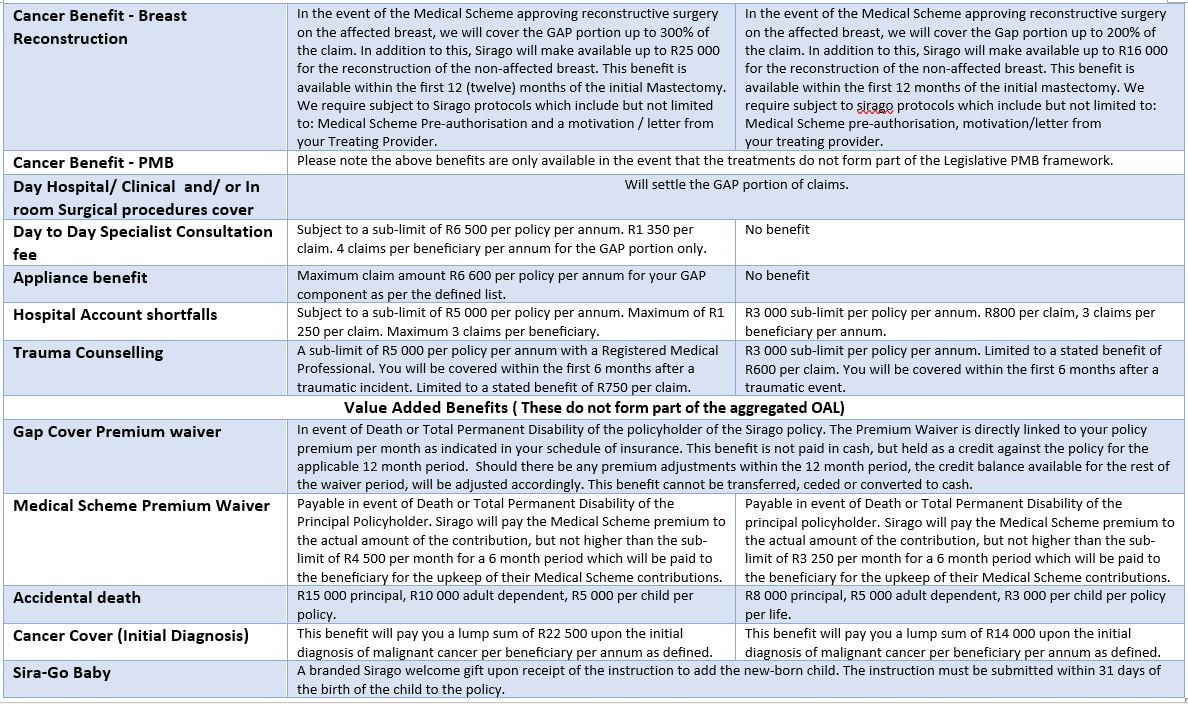

Below are the benefit comparison update for Ultimate Gap cover & Plus Gap cover for 2020:

0 Comments

o Physiotherapy consultations and treatment o Biokineticist consultations and treatment o Dietician consultations and treatment o A smoking cessation programme o Blood tests o X-rays

o New moms will also be able to access vouchers offering up to 70% off baby products at Baby City 2020 Contributions The Fund announced that the increases for 2020 range from just 6.2%, with an average increase on risk contributions of 9.4% and an average increase of 9.9%. The increases were as follows:

Click here to download the 2020 product brochure Please contact Namhla or Tammy in our Health and Wellness Department, email health@daberistic.com, if you have any queries about Bonitas Source: Bonitas  Click here to read more on Medical Aid enhancements

Please contact Namhla or Tammy in our Health and Wellness Department, email health@daberistic.com, if you have any queries about Discovery Health Source: Discovery  It’s now time to review your medical aid scheme cover for 2020. This means you have a window within which you can switch to a different plan for the new year. This window usually closes at the end of November (depending on your current provider), so don’t delay collecting the necessary information. This is not a decision to be rushed.

Why do I have to decide now? Medical aid providers allow you to switch to a higher plans once a year (at the end of the year) without penalties or consequences. If you want to save on premiums or you need to increase benefits, now is the time to do it. What if I want to change providers altogether? If you are unhappy with your medical aid provider, you can switch to another at any time of the year. But before you do, consider the following: Waiting Periods Medical Aids by law must accept anyone who applies to join their scheme. To protect themselves from older or sickly members that join without having contributed to the risk pool, they usually impose a waiting period of between 3 and 12 months. Waiting periods will apply if 1) you have not been a member of another South African medical aid for the past three months or more, 2) if you change medical schemes before 2 years of being covered with your previous medical aid provider and 3) if you have a pre-existing medical condition. Finding out about any waiting periods is extremely important before deciding to change providers. Late joiner penalty As an additional means to manage the risk of older or sickly members joining without having contributed to the risk pool, medical schemes (according to the Medical Schemes Act) are entitles to add a late joiner penalty to your premium if you were not part of a medical scheme before 01 April 2001. The late joiner penalty is calculated (using a prescribed formula) based on the number of years that you were not on a registered South African medical scheme. The late joiner fee can range between 5% and 75% of the total contribution, depending on the number of years that you were not covered by a medical scheme. Please contact Namhla or Tammy in our Health Department, email health@daberistic.com, to find out about different Medical aid options Source: Medicalaid.co.za  Let us use a case study to illustrate how financial planning can help a young family. Gavin lives in Joburg, 29 years old, is married to Ntombi with a 1-year old son Siya, named after the Sprinbok captain Siya Kolisi. Gavin works in a family business with a monthly salary of R30,000. In addition, he gets extra income of about 2,000 US dollars per year from YouTubing. The monthly expenditure of Gavin's family is R18,000. He can save about R10,000 a month. Looking at Gavin's personal balance sheet: He has no house, no car under his name, and no loans. He has R200,000 in bank deposit. He has a 10% stake in the family business. He has a life insurance policy with the following benefits: Life insurance R2, 361,000. Lump Sum Disability R2, 361,000 Severe Illness Benefit R944,400 Income disability benefit R7,300 per month He contributes R1,277 per month to a retirement annuity, retirement age 55, and current value R61,500. Gavin's family is on Discovery Essential Saver option, plus a gap cover policy to cover for medical expense shortfalls. The marriage between him and his wife is in the community of property. His wife is a housewife. His financial dependants are his wife and son. Gavin would like to buy a house of his own and invest overseas. Asked about his retirement planning, he says that he would like to retire at the age of 55 (although he knows it might be an unreachable dream), with a monthly income of R15,000 in today's money, plus travel abroad every year. The house and car loans will be paid off and there is an emergency reserve. For his children, he wants to provide for their education, until they complete their university degrees. I use a professional financial planning program to do financial needs analysis for Gavin and produce a financial need analysis report. Then I draft a proposed financial plan, with some preliminary recommendations to Gavin and Ntombi: 1. Risk planning Since Gavin has a single-income family, his child is still young, his life insurance is insufficient. He needs an additional R4,700,000 cover to provide protection for his family, especially his child's future education and living expenses. According to the financial analysis, he has enough severe illness insurance coverage and lump sum disability cover. His income disability benefit needs to be raised to R13,700 per month. The objective of income disability benefit is that when the insured is temporarily or permanently unable to work, the insurance company pays a monthly income as compensation until he goes back to work or until his retirement age. The cost of additional insurance benefits is R412 per month. I recommend that Gavin buys Discovery Global Education Protector, private school option. If he dies, is disabled or has a major illness, Discovery will cover the cost of tuition and extracurricular activities until the age of 24. It also includes a University Funder Benefit, which helps to pay part of his child's tertiary education fees . Monthly premium R358.07. 2. Investment planning I use the three-bucket approach to financial planning, which is easy for clients to understand.  The first bucket of money is the money needed in the next two years. It needs to be capital secure and highly liquid. It can be withdrawn at any time. It can be an emergency fund. I suggest that Gavin has R200,000 in the bank, in a high-interest account such as money market account or call account, which can withdrawn at any time.

The second bucket of money is the money needed for years 3 to 10. It can partially invest in growth assets, but seek stability. A suitable investment vehicle is a conservative fund. Part of the child’s education fund belongs to this bucket. The third bucket is the money that is needed only after ten years, usually for retirement funding, child’s education fund and long-term capital growth. I suggest that Gavin invest in equity funds, which have shown to have the highest long-term returns over the long term, but have short-term fluctuations (volatilities). It can be done on a debit order basis, to benefit from a disciplined investment approach and Rand cost averaging. In addition, I suggest that he invest overseas, in US Dollars, to benefit from investment opportunities internationally, diversify risks, and hedge against long-term depreciation of the South African Rand. He can open an account with a minimum investment of 1,500 US dollars. 3. Education fund The analysis points out that Gavin needs to invest R6, 898 every month for the next 18 years, for his son's education. I suggest that he can start a tax-free investment account in his son's name and debit R2,750 from the bank each month to invest in a long-term growth portfolio. The investment value is expected to be R1,121,886 after 15 years. 4. Retirement planning In calculating the capital required for retirement, I used the following assumptions: Retirement age 65 (not client's wish of 55) Monthly income, today's value of R22,100. This is not the R15,000 Gavin indicates to me in the initial discussions, as after taking into account the medical expenses in the old age and the desire to travel abroad, this is the more realistic figure. Inflation rate 6% Investment return 8% The retirement capital required is R31, 415, 100. Gavins existing Retirement Annuity is expected to reach R6,077,840 on retirement. In order to achieve the retirement income target, Gavin needs to invest an additional R5,390 per month, increasing by 6% per year. 5. Estate planning I recommend that the Gavin and his wife make a joint will to distribute the estate in South Africa as he wishes. From this case study, you can get a glimpse of the process, details and the wide areas covered in personal financial planning, tailored to the needs of a person or a family. The more assets and the more complex a person's financial situations, the more complicated is the financial, tax and estate planning required. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|