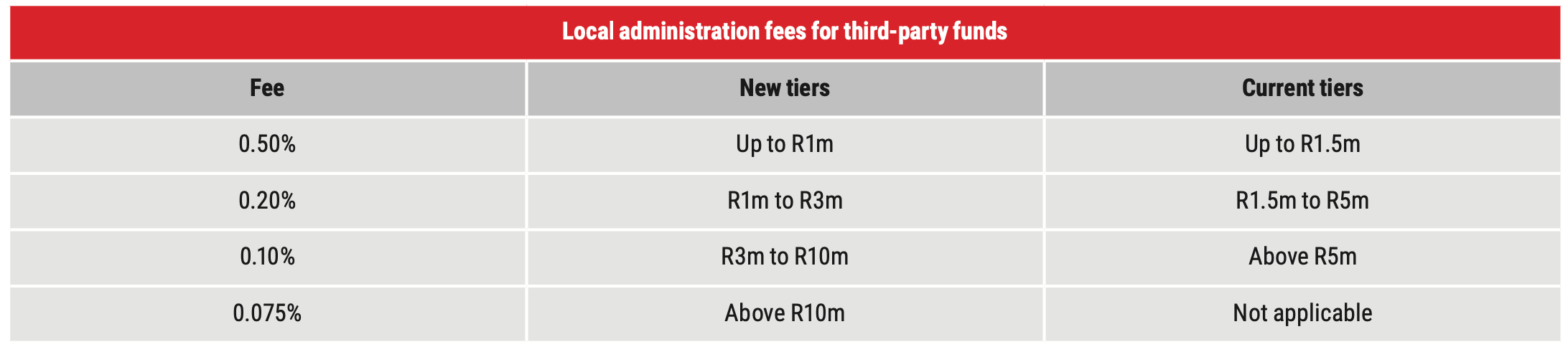

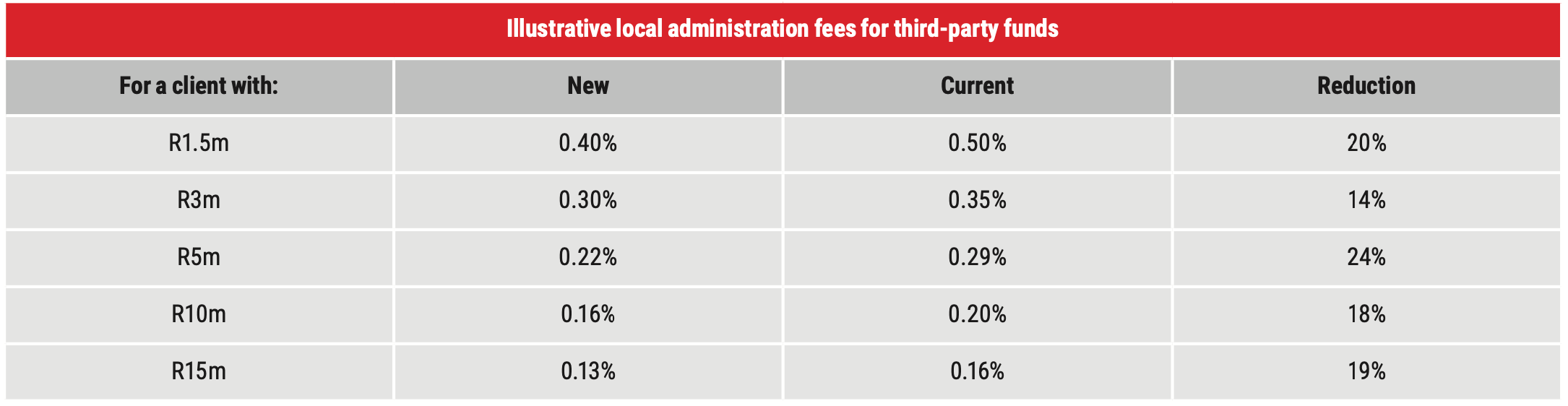

We are pleased to share that Allan Gray, one of the largest linked investment service providers (LISPs) in South Africa, has reduced its adminsitration fees. Allan Gray have reduced their local administration fees for third-party funds, effective 1 October 2022. In early 2023, they will combine a client’s local and offshore platform assets for the purposes of calculating their applicable administration fees on each platform, enabling clients to benefit from lower fees. In early 2023, they will introduce a step fee for new clients investing below their lump sum minimum of R50,000. Allan Gray reducing local administration fees for third-party funds Allan Gray's new fees, which are effective 1 October 2022, are outlined below.  The administration fee charged for local Allan Gray funds will remain unchanged at 0.20% per annum (excl. VAT).  Combining local and offshore platform assets to calculate administration fees (from 2023)

Allan Gray will combine your local and offshore platform assets when calculating your administration fees which will result in more of your assets being subject to the lower fee tiers. Currently, your local administration fees are based on the market value of all local platform assets linked to your investor number and applied to the local administration fee tiers. Your offshore administration fees are calculated separately based on the market value of all offshore platform assets linked to your investor number and applied to the offshore administration fee tiers. The effective date of this change will be communicated ahead of implementation in early 2023. What does this all mean for you as an investor? For clients with assets more than R1 million with Allan Gray, they will enjoy reduced administration fees, so they will keep more of the investment returns. We applaud Allan Gray for reducing costs of investing for clients. For clients with assets less than R1 million with Allan Gray, the 0.5% administration fee stays the same. For new clients with less than R50,000 invested, they will have to pay a step administration fee of 1.0% per annum (excl. VAT), until their investment value has reached R50,000. So Allan Gray is not so cost effective towards smaller investors. This cost is understandable, as there is a base cost of opening and maintaining an investor account. If you have any questions or feedback, email us at service@daberistic.com

0 Comments

In partnership with Morningstar: This document has been created to highlight the most important issues facing investors, share insights from our current research, and help you make better investment decisions as we enter 2022. It has been compiled by our investment leaders and draws on the work of our global team.  Last month I talked about Step 5 - Invest 15% of your earnings. Let's continue with Step 6 - Set up an emergency fund. You should prepare for a rainy day. Things can happen and will happen. A death in the family, sickness, accident, a punctured tyre, someone in the family comes to borrow money, the phone is stolen ... unforeseen expenses, the list goes on. Or you lose your job. Or your business is negatively impacted by COVID. Having an emergency fund can help deal with these instances, cushion the blow. You should use a bank savings account, separate from your daily transactional account, to set up an emergency fund. You should have a minimum of 6 months' pay in that emergency fund, to be safe. For example, your monthly take-home pay is R40,000. Then you should have R40,000 x 6 = R240,000 in your emergency fund. If you ever lose your job or your income, then you can sustain yourself and your family for six months, while you look for another job or find the next source of income. If your business has a monthly expenses of R200,000, then you should have R200,000 x 6 = R1,2 million in the company's emergency fund. If you have not reached the ideal emergency fund amount, create a plan to top up the emergency fund every month. Maybe you have more income or receive a bonus in a month, use part of that money to top up your emergency fund. Continue with this process until you have reached the target of having 6 months' worth of income in your emergency fund. From time to time, you may have to access the emergency fund as emergencies come up. That's exactly what it's for. After you have taken money out of the emergency fund, top it up again, until you reach the ideal emergency fund amount. So what vehicle should you use to keep your emergency fund? I would recommend the following three options: 1. Bank savings account: This is an ideal vehicle for keeping your emergency fund. It is safe and liquid. You can withdraw money at any time. A savings account, call account or money market account will work. What is not recommended is fixed deposit account and notice accounts. These type of bank savings accounts tie you up for a period of time, maybe 7 days, one month or even longer. The emergency fund is there when you need it. You don't want to put the emergency fund in an account where you cannot access immediately, or with penalties if you want to access it. 2. Home loan with access bond facility. If you have a home loan, make sure you have the access bond facility. I always make sure my home loans have access bond facility. It is an excellent financial management tool for personal finance. This allows me to pay more into the home loan when I have extra money, to reduce the capital amount and interest payment. I can take out the extra money I put in at any time. Watch this to know the 7 things you should know about home loan. The segment on Access Bond starts at 20:10. The beauty of this solution is it reduces the interest and capital amount outstanding as you pay the extra money into the home loan account, but when you need it, you can take it out.

So imagine you put in extra money every month, over some time you have put in extra R240,000 in total. So you have R240,000 you can access in your Access Bond facility. There is your emergency fund! 3. Income funds. These are unit trusts, or collective investment schemes, that invest in a wide variety of assets, such as cash, credit, government and corporate bonds, inflation-linked bonds and listed property, both in South Africa and internationally. These funds focus on investing in income generating assets. In the current low-interest rate environment, they offer an attractive yield of 6% to 7%. In the short term an investor may experience temporary capital value fluctuation, but you can expect positive return over any 12 month period. Examples of good income funds are: Coronation Strategic Income Fund, Ninety One Diversified Income Fund, Nedgroup Flexible Income Fund. Any questions on emergency fund for Uncle Kevin? Email to service@daberistic.com. Ninety One (formerly known as Investec Asset Management) Global Franchise Feeder Fund has a long track record (25 years), managed by veteran portfolio manager Clyde Rossouw, focused on investing in global quality companies. The fund seeks to invest in world leading companies with strong competitive advantages, superior margins and focuses on capital re-investment, with a high-conviction portfolio of 25–40 stocks of primarily investment grade companies, with high customer loyalty, strong brands and no debt. It is an equity-only fund adjusting exposure to maximise downside protection and participate meaningfully in rising market. This fund is also part of the managed portfolios developed by Morningstar for our clients. Through us you access the institutional fee class with lower fees.  Hi everyone, this is Uncle Kevin. Today I would like to encourage you to start investing today.

Have you developed a savings habit? Are you saving money every month? Do you know that by consistently investing money every month, you are going to reap the rewards in the long term? Investing is not a short-term game like a 100 metre sprint, but rather a long-term game like a 42km marathon. I would like to use two real-life client examples to demonstrate how you will reap rewards in the long run. Zane is now 43 years old. 10 years ago when he was 33, he had a financial planning meeting with me. He wanted to invest for his child's education. At that time I advised him to take up a Discovery Invest Endowment Plan, R1,000 per month, with the contribution increasing at CPI inflation rate every year. He started the investment on the 1st of April 2011. He has continued with the investment plan without fail. In year 10, his monthly contribution was R1,639. Now 10 years later, at the beginning of April 2021, the investment plan value, after deducting income tax, is R 223,691. The internal rate of return, IRR is 8.39%. Now internal rate of return is the net return received by the investor, net of fees, charges and taxes. So over the 10-year period, Zane has received on average 8.39% return per annum. Which is a good return. The second client, Ken is now 49 years ago. 10 years ago when he was 39, he also had a financial planning meeting with me about the same time, and he wanted to invest for long-term. At that time I advised him to take up a Discovery Invest Endowment Plan, R1,000 per month, with the contribution increasing at CPI inflation rate every year. In year 10, his monthly contribution was R1,639. Now 10 years later, at the beginning of April 2021, the investment plan value, after deducting income tax, is R202,116. The internal rate of return, IRR is 7.13%. There are 3 points I would like to focus on:

Use this link to book a FREE Financial Planning session with Kevin, using Microsoft Teams Online Meeting: https://calendly.com/daberisti... We have partnered with Fedgroup in offering their financial solutions for many years. A recent update shows that Fedgroup Participation Bond continues to attract investors interest in the volatile and uncertain markets. Its fund size has grown from R1.9 billion to R3.9 billion. It is a five-year term investment. The current fixed interest rate is 7.6%. The Growth Option, which compounds interest income, offers a very attractive 9.21% effective rate. This investment is suitable for investors and pensioners looking for steady income and a fixed return. Please contact 083-633-4671 or service@daberistic.com, if you are interested in this investment.  outh Africa has a relatively small equities market with a handful of dominant shares, spread across a few sectors, which are available to invest in. This presents a significant risk for investors: a highly concentrated portfolio.

When compared to global markets, the Johannesburg Stock Exchange (JSE) is relatively small, comprising less than 1% of the total global investing universe. It is also highly concentrated, with the top 10 shares on the FTSE/JSE All Share Index (ALSI) making up between 50% and 60% of the index. In contrast, the top 10 shares in one of the world’s major indices, the S&P 500, make up just over 20% of the index. Most of the ALSI’s concentration comes from one share: technology giant Naspers, which makes up 20% of the index. Naspers’ dominance in recent years has increased concentration risk for investors, making portfolios overly sensitive to the factors that drive its value. In general, most investors are happy to contend with the exposure, as long as they are still generating positive returns. But what happens when the proverbial goose stops laying the golden eggs; when the dominant share(s) in your portfolio begins to perform poorly? How you can mitigate your concentration risk As famously stated by American economist Harry Markowitz, who received a Nobel Memorial Prize in Economic Sciences: “Diversification is the only free lunch in finance.” The best way to reduce your concentration risk, without losing out on the potential to earn good returns, is to make sure that you are invested in a combination of assets that have little correlation to one another – essentially, having a diversified portfolio where you generate returns from a wider spread of assets, industries and markets with an acceptable level of risk. To construct a diversified portfolio, one has to consider correlation and volatility. Correlation measures the strength of the relationship between the returns of two assets. A positive correlation indicates a strong positive relationship, i.e. the two assets tend to have higher and lower returns at the same time – this is indicative of an undiversified portfolio. A negative correlation implies the opposite, i.e. returns of the two assets move in opposite directions at any given time. A correlation of zero implies that no relationship (positive or negative) exists between the returns of the two assets. By adding assets with zero, or negative correlation, a portfolio becomes more diversified. You should also look at the overall volatility of your investment to gauge how well your portfolio is diversified. Intuitively, a portfolio consisting of correlated assets should show a larger deviation in its overall returns (i.e. high volatility), while a portfolio that has uncorrelated or negatively correlated assets should show smaller deviations in its overall returns (i.e. low volatility). In essence, if you have a well-diversified portfolio, then your investment should generate returns at lower levels of volatility over the long term. Diversify your portfolio If all this sounds very complicated, you could consider investing in a balanced fund. These are available both locally and internationally and offer a good solution to those investors who want to create a diversified portfolio without the hassle. Your chosen investment manager will carefully select a basket of uncorrelated assets from different markets, companies and industries to ensure that you generate good returns with minimal concentration risk. Local balanced funds offer South African investors some offshore diversification, but remember that Regulation 28 of the Pension Funds Act limits their foreign asset allocation to a maximum of 30% of the fund, with an additional 10% for investments in Africa outside of South Africa. This may not be enough offshore exposure for your needs – in which case you can also invest directly with offshore fund managers of your choice or through an offshore platform, such as the one Allan Gray offers. Every South African resident can use up to R11 million offshore for all foreign expenditure including travel, foreign exchange and for investing purposes. The first R1 million, called the single discretionary allowance, can be used without having to obtain permission from the South African Revenue Services (SARS) and the Reserve Bank. If you want to spend above this allowance, up to R10 million, you would need to get a tax clearance certificate from SARS. To further diversify, many investors choose to invest in more than one of the same type of fund from different managers. If you go this route, it is important to check that the underlying investments are different; otherwise, the combined weighting of the duplicate shares may increase your portfolio’s concentration. Building a diversified portfolio can be complicated and requires a solid understanding of markets and companies. But the good news is that you don’t have to go at it alone. An independent financial adviser (IFA) can help you assess the concentration risk in your portfolio and advise accordingly. It can be tempting to ignore concentration risk when the going is good, and returns are attractive. However, an undiversified portfolio can quickly become a problem if your most concentrated shares begin to perform poorly. Source: Vuyo Nogantshi , Allan Gray |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|