National Treasury announced an increase in Value Added Tax (VAT) from 14% to 15% effective 1 April 2018. Your short-term insurance premium is subject to VAT and will be adjusted. The new premium will be communicated to before your April debit order collection and below is some of FAQ:

General

Premium collection

Policy Amendments

For any queries regarding changes to your insurance, please contact Jan or Po-Lin in our Short Term department shortterm@daberistic.com tel no: (011) 658 – 1333 Source: Momentum

0 Comments

Daberistic hosted a Vitality Wellness day at the office where clients were able to do their Fitness,Health and Nutrition checks in order to earn their Vitality points. Our Daberistic staff were able to assist clients with completing their online assessments,complete forms as well as link their movie cards, food cards in between the checks. We look forward to the next one.       The 2017-18 budget provided limited relief for fiscal drag and introduced a personal income tax of 45% for individuals earning R1.5m or more. The previous top bracket of 41% was set at an income of R701,301. Tax collections have fallen sharply in light of poor econo-mic growth and the Treasury has had its worst performance in collections since the 2009 recession. So the trend of increasing taxes seems likely to continue as the Treasury sets about on what it calls a "measured, prudent course of fiscal consolidation". In the light of this, it is now more important to plan your financial affairs effectively from a tax point of view. There are several structures you can employ legally, without much cost, that can be quite effective in reducing the amount of tax you pay on your investments. One such structure is an endowment, which has potential tax advantages for investors in higher tax brackets and can also be used for estate planning. There are typically two types of endowments: "traditional" and new-generation unit trust-based endowments. Traditional endowments tend to have an insurance element linked to the structure, usually in the form of life insurance. They are less flexible in that you don’t have control over the underlying investment and may be charged fees or penalties when changing the contribution amount or withdrawing early.  New-generation endowments tend to be more flexible and give you choice over the underlying investment portfolio.

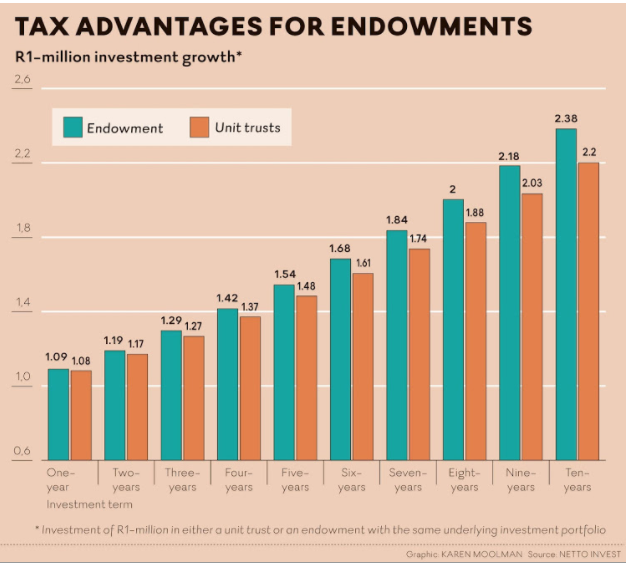

There are no asset class restrictions on endowments (unlike retirement funds investments). This means that you are free to invest in any allocation of equities, bonds, property and cash (including the offshore version of each). Endowments present valuable tax arbitrage opportunities. Tax on income is levied at a flat rate of 30% within the endowment. This is attractive when you compare it to the 45% applicable to investors in the highest tax bracket. Capital gains tax is levied within endowments and varies according to the legal nature of the owner. Within an endowment, investors in the top tax bracket will pay capital gains tax at an effective rate of 12% (40% inclusion rate multiplied by 30% tax within the endowment). In a unit trust, the same investor could pay an effective rate of 18% on capital gains (40% inclusion rate multiplied by 45% marginal tax rate). If you are an individual with a tax rate of less than 30%, investing in endowments for tax reasons alone, probably does not make sense. Endowments can also be a useful estate planning tool as they allow you to nominate beneficiaries The tax arbitrage opportunities within an endowment can be explained by comparing the after-tax return to that of a unit trust. Assume Steve is in the top tax bracket and under the age of 65. He has already used the interest exemptions (R23,800) and capital gains tax exemptions (R40,000). Steve has the choice to invest R1m in either a unit trust or an endowment with the same underlying investment portfolio. The investment is in a typical balanced fund with a blend of asset classes returning 10.8% over the period. At the end of the 10-year term the endowment will be worth R2,383,048 and the unit trust will be worth R2,788,673. However, in the unit trust, the tax on the interest (payable annually) and capital gains tax on withdrawal at the end of the term amount to R587,806 and reduces the proceeds to R2,200,867. The after-tax return of the endowment beats the after-tax return of the unit trust by 0.86% over the period. Steve would be better off opting for the endowment. Endowments can also be a useful estate planning tool as they allow you to nominate beneficiaries. That is, a nominated person can receive direct ownership of, or payment from, your endowment in the event of your death. This means that the beneficiary receives the value of the endowment without having to wait for the estate to be wound up first. What’s more, no executor fees (which can be as high as 3.99%) are charged on the value of endowments received by beneficiaries. There are some other subtle-ties to bear in mind. An endowment is a long-term investment vehicle by nature, with the minimum investment term being five years. It is possible to access some funds before the five-year period in the event of an emergency, but there are limits imposed as to how much you can withdraw. If you are unsure whether an endowment is appropriate for your circumstances contact our Financial advisor, please contact Kevin or Ray, email: invest@daberistic.com tel no: (011 658-1333) Source: Businesslive  After three years of low equity returns, investors drawing an income from their investments may be considering shifting some of their portfolio exposure away from multi-asset funds with equity exposure towards cash. However, the appropriate time for switching - if there ever was any - has passed, and retirees are in danger of eroding the longer-term value of their retirement capital should they switch now. This trend towards cash has been evident in South Africa over the past year in the wake of the higher returns (of around 7.0% p.a.) offered by bank deposits and money market funds compared to riskier equity holdings. Poor equity performance has dragged down the returns of well-diversified multi-asset funds in which many retirees are invested: the average ASISA low-equity multi-asset fund delivered only 6.3% p.a. over the three years to 31 July 2017, and the average ASISA high-equity multi-asset fund (the typical “balanced” fund) returned only 5.5% p.a. over the same period, according to Morningstar. Compare these returns with those of the past 15 years, where high-equity fund returns averaged 12.5% p.a., and low-equity funds averaged 10.0% p.a. The longer-term performances are in line with the funds’ generally accepted return targets of inflation + 4% for the less aggressive low-equity category, and inflation + 6% for the more aggressive high-equity category, with long-term inflation at approximately 6%.  Given their recent under performance, retirees dependent on income from multi-asset funds may think that they will benefit by moving to cash now. However, they would be getting their timing wrong by being too late. Current valuations show that prospective returns from multi-asset funds are higher than those from cash assets. So by moving to cash now, retirees will be exposed to falling cash returns in future (the SARB has already started cutting short-term interest rates), and will miss out on any improvement in returns from multi-asset funds.

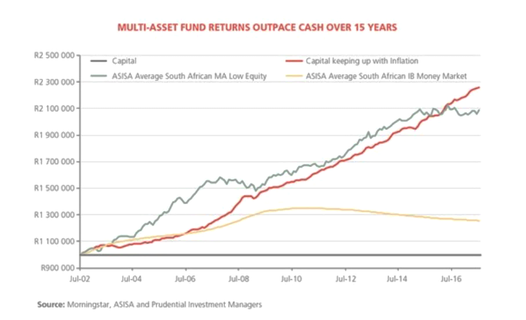

The accompanying graph shows how a R1.0 million retirement investment has performed over the past 15 years (July 2002-July 2017), starting with a 5% annual drawdown and escalating the drawdown by inflation, when invested in different funds. The initial capital investment is represented by the fixed black line. In order to have maintained its real value over time, it would have needed to grow at a rate equal to inflation, to R2.26 million (as shown by the red line). Would a money market investment have given the retiree an adequate return over the 15 years? Clearly not: the yellow line in the graph depicts how the R1.0 million would have performed invested in the average South African money market fund (the ASISA IB Money Market category) while drawing the income over the period. Due to its low return, the capital would have grown to only R1.25 million. Although it would have successfully given the retiree their income (totalling R1.1 million), the real value of the retiree’s capital would have been significantly eroded (shown by the gap between the red and gold lines). By contrast, an investment in the average low-equity multi-asset fund is shown by the green line. Although the fund return varies over time, it manages to outperform or remain in line with the inflation requirement (red line) for much of the period. Its more recent underperformance is partly compensated by the earlier excess performance. The retiree ends up with R2.09 million, while also having drawn down R1.1 million in income payments over the 15 years. From this evidence, it is clear that multi-asset funds have been delivering the returns they are expected to over longer periods, and investors, especially retirees, need to think twice before moving away from them. Anyone switching to cash now is likely getting the timing wrong – they will receive lower returns over the longer term (as the graph demonstrates), or if they plan to switch back to multi-asset funds later, they will also likely mistime their move. To set up an appointment with our Financial Planners, please contact Kevin, email: invest@daberistic.com tel no: (011 658-1333) Written: Pieter Hugo Source: Prudential  Take advantage of the positive market sentiment with Discovery Invest investment opportunities

There has been a wave of positive sentiment in South Africa following Cyril Ramaphosa’s election as president, with positive reactions to the budget speech and a strengthening of the rand. Investors’ sentiments are on the rise again. With this positive investor sentiment in mind, Discovery investment opportunities provide clients with:

To get a quote on different Discovery Investment options, please contact Kevin or Ray, email: invest@daberistic.com tel no: (011 658-1333) Source: Discovery invest  What is the fund’s objective? Strategic Income aims to achieve a higher return than a traditional money market or pure income fund.

What does the fund invest in? Strategic Income can invest in a wide variety of assets, such as cash, government and corporate bonds, inflation-linked bonds and listed property, both in South Africa and internationally. As great care is taken to protect the fund against loss, Strategic Income does not invest in ordinary shares and its combined exposure to listed property (typically max. 10%), preference shares (typically max. 10%), international assets (typically max. 10%) and hybrid instruments (typically max. 5%) would generally not exceed 25% of the fund. The fund has a flexible mandate with no prescribed maturity or duration limits for its investments. The fund is mandated to use derivative instruments for efficient portfolio management purposes. Important portfolio characteristics and risks: Strategic Income is tactically managed to secure an attractive return, while protecting capital. Its investments are carefully researched by a large and experienced investment team and subjected to a strict risk management process. The fund is actively positioned to balance long-term strategic positions with shorter-term tactical opportunities to achieve the best possible income. While the fund is managed in a conservative and defensive manner, there are no guarantees it will always outperform cash over short periods of time. Capital losses are possible, especially in the case of negative credit events affecting underlying holdings. How long should investors remain invested? The recommended investment term is 12-months and longer. The fund’s exposure to growth assets like listed property and preference shares will cause price fluctuations from day to day, making it unsuitable as an alternative to a money market fund over very short investment horizons (12- months and shorter). Note that the fund is also less likely to outperform money market funds in a rising interest rate environment. Given its limited exposure to growth assets, the fund is not suited for investment terms of longer than five years. Who should consider investing in the fund? Investors who are:

To invest in Coronation Fund, please contact Kevin or Ray, email: invest@daberistic.com tel no: (011 658-1333) Source: Coronation  Yesterday (Happy International Women's Day!) I was fortunate to visit Dodge & Cox in San Francisco, US. Kevin Johnson, an experienced portfolio manager at Dodge & Cox, was kind in spending over an hour with me, for me to understand more about the firm, its operations and investment outlook. Dodge & Cox is situated in the Financial District of San Francisco, occupying 4 floors in this very impressive skyscraper on 555 California Street.

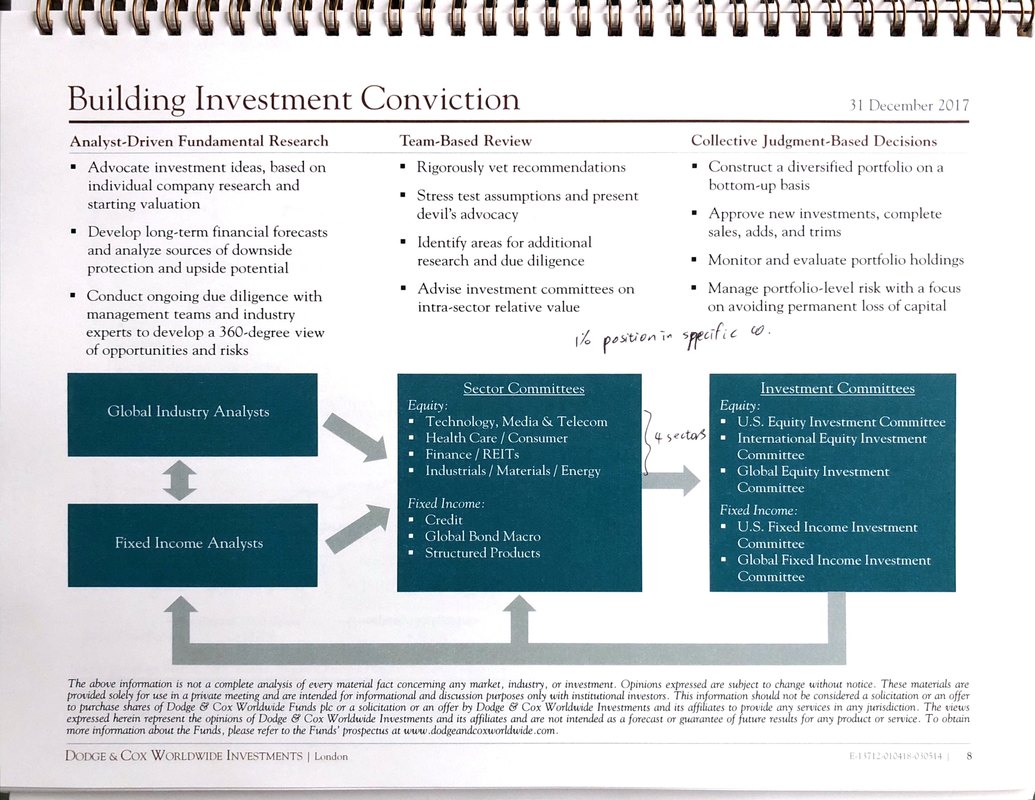

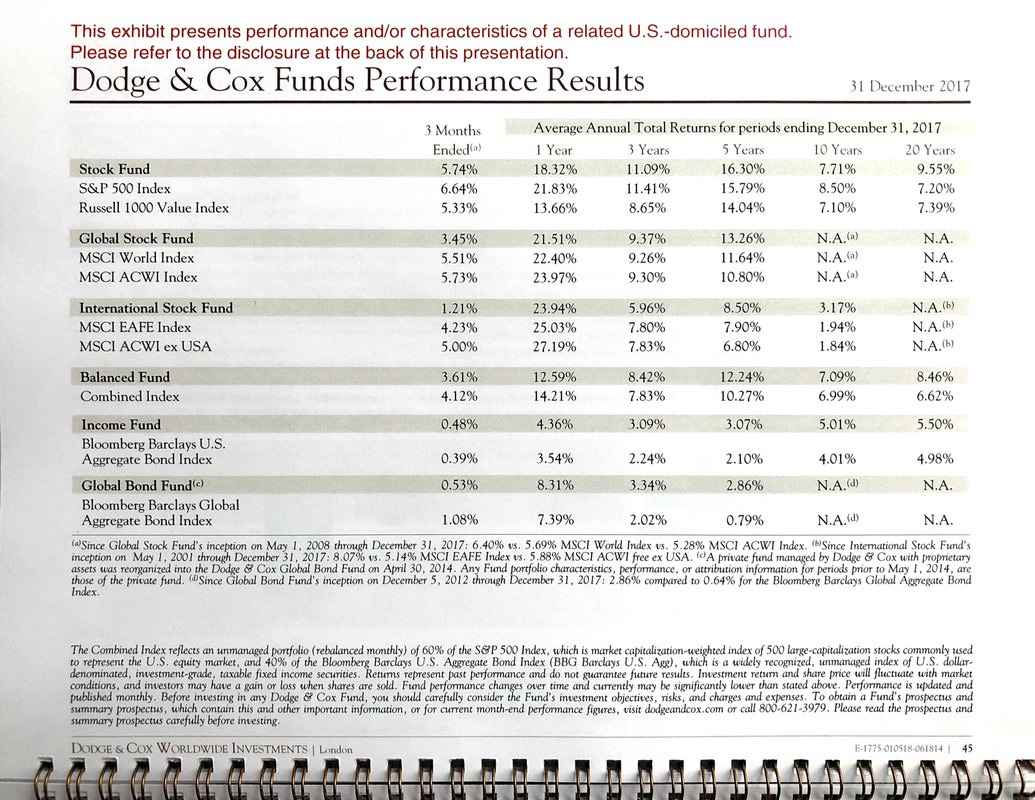

After the guest registration process at the lobby, I was told to take a lift to the 40th floor. When the elevator door opened, I walked onto think carpet, with the gold plated Dodge & Cox signage in front of me. I knew I was at the right place. The office has stunning views of the San Francisco Bay area. The tall building in the second picture is Transamerica Pyramid, 260m high.   Kevin Johnson came and welcomed me, took me to the boardroom with stunning views of San Francisco. I decided to sit with my back facing the view/window, so I could better focus on my discussions with Kevin. Kevin Johnson is well versed in the investment markets, with 28 years of experience at the firm. I gave him a background of what Daberistic does, our wealth management services to our clients, and how Dodge & Cox funds fit into our solutions to our clients. Kevin then gave me a presentation booklet on Dodge & Cox UCITS. I am not familiar with the term UCITS, so afterwards I googled it. UCITS stands for “Undertakings for Collective Investment in Transferable Securities". In essence mutual funds, or unit trusts as known in South Africa. Dodge & Cox was founded in 1930 in San Francisco. It prides itself in having a stable and well-qualified team of investment professionals, most of whom have spent their entire careers at Dodge & Cox. Ownership of Dodge & Cox is limited to active employees of the firm. Currently there are 75 shareholders and 271 total employees. It is a mature fund management business. Kevin emphasised the point that Dodge & Cox is independent, no absentee ownership, no parent company to report to, so not forced to do anything. This is a great contrast to Merrill Lynch, which is owned by Bank of America. Dodge & Cox is solely in the business of investing clients' assets. Apart from the San Francisco office, it only has one small client service office in London. So all its staff are based in the single office in San Francisco. It offers a focused range of strategies (I tend to like fund managers with a small, focused range): US equities Non-US equities Global equities: combination of the above two US Fixed Income Global Fixed Income US Balanced (combining equities and fixed income) Active vs Passive This debate continues to rage on. Kevin and Dodge & Cox are undoubtedly in the Active Managers camp. His comments? Active managers have been overly criticised for high fees, the focus on (comparing to) average active managers return is a mistake. Dodge & Cox wrote an article on the characteristics of good active managers. These include: 1. Low turnover 2. Experienced 3. High active share. Passive is really a Momentum strategy, buying more on the way up. He used the dotcom bubble as an example: in 1998 the tech sector accounted for 45% of S&P, and index trackers would continue buying more of tech companies as their weightings in the index rose. Only to see the dotcom bubble burst until 2002. What is important is to focus on performance after fees, he comments. I 100% agree with this point. Dodge & Cox is a value-driven fund manager. Value as a style has fallen out of favour with investors over last few years, as the bull market continues to rise. Dodge & Cox continues to stick to what it has done over last 88 years, without wavering. Value Defined It is always good to get under the skin of a manger to understand better what they mean. Kevin defines the firm's Value Investing as "what you thing it's going to be worth in the future. It can be strictly metric based, such as PE ratio. It can also be valuation relative. You would want to avoid something with very high premium built in the price, as it may not be sustainable." So Dodge & Cox sees value in a slightly different way to Warren Buffet. It uses four investment hypotheses: Above Average Growth, Compounders, Cyclical or Asset Play, Deep Value or Turnaround. Warren Buffett's style is probably more the first two hypotheses. Risk Management Over the years I have learnt to appreciate that the best fund managers are also the best risk managers. Dodge & Cox has a systematic way of analysing risks, under the six headings of Operational, Macroeconomic, Commodity, Financial, Technological and Political/Legal Risks. These are used to assess what will cause the future outcomes to disappoint. Investment process Dodge & Cox has a tried and test investment process, run by a very experienced team.  I posted some very specific questions to Kevin, his comments are as follows: Schroders as a value manager We as a manager do not worry about what other fund managers do. My impression is they have an excellent reputation, has value orientation. It may have lots of funds. On the question of the use of the word Recovery in Schroders global Recovery Fund: "There can be an element of marketing. This might define value in a more narrow way." Coca-Cola "it is a good business, not a lot of growth, highly priced. We don't own any Coca-Cola stock. Maybe when its PE is 13 it becomes interesting to us." Amazon "A remarkable company, high valuation makes no sense to us. However what it does influences our thinking on other retailers. Retailers like Sears and JC Penny have been in decline for years. Macy's also struggling, not to the same extent. Walmart and Target have done better in response to the changing business environment, the online/offline mix strategy is a good one." Its AWS (Amazon Web Services) also influences our thinking on other tech companies like Microsoft." "of the FANGs, we only own Google" Dell Dell just came out with its update, showing 9% turnover growth and doubling operational losses, so I posted to Kevin. "Dell went largely private, had a series of corporate actions over last 2 1/2 years. Laptops have low margin, the profitable part is server/other services." Portfolio diversification As a wealth manager I am very sceptical of funds with 20% weighting in one stock (Naspers), as I question their risk management and diversification. "We do not have more than 5% of portfolio in one holding. In our Global Stock Fund, we probably will not exceed 3%." Its original (US) Stock Fund has an enviable track record of annualised 9.55% return over 20 years, outperforming S&P500. Over 10 years a respectable 7.71% after fees. The Global Stock Fund, which South African investors can access via Glacier Global Stock Feeder Fund, has done annualised 13.26% in USD over last 5 years.  The time was just too short, if there is an opportunity I would come back again. At the end of the meeting I asked Kevin to take a photo together. He agreed as a gentleman.  |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|