|

Death, while an incredibly difficult subject to confront, is one of life's unavoidable realities. Yet many investors fail to prepare for this eventuality and put their loved ones' financial futures at risk. According to The Fiduciary Institute of Southern Africa, more than 75% of South Africans pass away without a valid will drawn up.

In the spirit of National Wills Week this month, we want to empower you to prepare adequately and help you leave a lasting legacy by posing these questions: • Is your will up to date? Make sure you keep me abreast of any material and life-changing events, such as marriage, the birth of a child, or a death in the family. • Are your retirement fund nominees' details up to date? • Are the beneficiaries of your various policies up to date? If your investments are structured as a life policy, you will need to make sure your service provider has the correct beneficiary appointments on file to ensure speedy payment to your intended beneficiaries. • Have you planned for immediate needs? Make sure you have made provisions for any immediate expenses, such as funeral costs, that may need to be covered before your investments can be accessed. • Have you spoken to your beneficiaries, dependents, and nominees about the contents of your will? Contact us on service@daberistic.com if you want a financial planner to review your financial affairs.

0 Comments

In 2024, South Africa will finally see another major change to our retirement system. Although known as the “Two Pot system”, in reality, and for most, it will be a new three pot system. All retirement savings invested before 1 September 2024 will vest in a vested pot (pot 1), while all new contributions after 1 September 2024 will be allocated between a savings pot (pot 2) and a retirement pot (pot 3). Investors aged 55 and older as of 1 September 2024 will only have one pot - if you so choose.  “South Africans are not saving enough for retirement!” screech the headlines at least once a year, followed by industry pundits such as myself citing shocking statistics such as “90% of retirees are unable to maintain their standard of living after retirement”.

Hair-raising stats like this, taken from a January 2022 study by Genesis Analytics and the Financial Sector Conduct Authority (FSCA), are published year after year but have done little to scare under-saving South Africans to change their ways. This is evidenced by the same study’s finding that two-thirds of retirement fund members have less than R50,000 saved. If the definition of insanity, according to the wisdom of Albert Einstein, is doing the same thing over and over and expecting different results, we need to try something new to incentivise 90% of South Africans to save adequately for retirement. This is why I welcome the government’s new “two-pot” retirement system, which is now set to be introduced on March 1 2024 as opposed to the initial and somewhat unrealistic date of March 1 2023. It is a long-overdue revamp of a system that is clearly not effective, a fact that was reiterated in November when SA slipped even further down in the Mercer CFA Institute Global Pension Index. SA dropped three places this year: down to 34 out of the 44 pensions systems the index benchmarks. There are still many details that need to be finalised before the new two-pot system is promulgated along with the annual budget in March 2023, but the broad aims already agreed on will put structures in place to entice South Africans not only to save for retirement, but preserve these savings until retirement age. And it will provide South Africans with another accessible tax-free savings vehicle once they’ve maxed out their annual or lifetime tax-free savings allowance. Enforced preservation with more flexibility The two-pot system will apply to all members of pension and provident funds, umbrella funds and retirement annuity funds who were under the age of 55 as of March 1 2021. It is designed to address the achilles heel of the current retirement system: members are able to cash in their entire savings if they change or lose jobs. This all-or-nothing preretirement withdrawal rule radically reduces members’ chances of achieving their retirement goals. And since early withdrawals count towards each member’s one-off R500,000 tax-free lump sum withdrawal allowance, large preretirement withdrawals sabotage a member’s retirement outcome. The two-pot system will change this by splitting retirement savings: two-thirds of contributions will go into a retirement pot and one-third into a savings pot. The retirement pot cannot be touched until retirement, even if you lose or change your job, and must be annuitised at retirement. “The new 'two-pot' retirement system is designed to address the Achilles' heel of the current retirement system, which allows large preretirement withdrawals that sabotage a member’s retirement outcome.” Kyle Hulett, head of investments at Sygnia Asset Management If you would like to set up an appointment with our Financial Advisor contact Sandra, email: service@daberistic.com tel (011)658-1333 Written by: Kyle Hulett Source: Timeslive The 2021 edition of the 10X Retirement Reality Report points to a deteriorating pension outlook for South Africans. In the wake of the Covid-19 pandemic, even fewer now look forward to a comfortable retirement, says Chris Eddy, head of investments at 10X Investments. This is evident across all age groups, demographics and income levels. The 10X report is based on the annual Brand Atlas Survey, which tracks the lifestyles of the 15 million economically active South Africans in households earning more than R8,000 per month. Alarmingly, this modest cut-off already excludes two-thirds of households in the country. In total, 71% of respondents indicated they had no retirement savings plan at all, or just a vague idea of one. That is a lot of people who could be forced to rely on the kindness of family and friends, or to live off South Africa’s meagre older person’s grant (state pension) of R1,890 per month (R1,910 for those older than 75), said Eddy. Within the ‘fortunate’ minority, half the respondents still don’t save because they have nothing left at the end of the month. And even among those who are saving, just 7% anticipate a comfortable retirement; 79% fear they won’t have enough or feel unsure. Most survey respondents (74%) believe they will have to generate some income after they retire. Another 19% are not very sure, leaving just 7% of respondents feeling confident that they are on course for what is increasingly becoming an outdated notion of retirement, based on full financial independence. Breaking this down into different income groups: a mere 6% of those with a household income of R50,000 and above feel sure they will not have to keep earning after they retire. For both other income groups, it was just 7%. This highlights once more that achieving a financially secure retirement is less about how much we earn, and more about how much we engage in the process, inform ourselves and save.  But how much is enough, and how do we start a savings plan to get there? Several leading financial services firms weigh-in: The 80% rule Schalk Louw, portfolio manager at PSG Wealth, notes that many experts recommend using the 80% rule as a benchmark for what you will need to cover your monthly expenses once retired. “I won’t personally guarantee the accuracy of this figure, but it does give us a basis to start from,” said Louw. If you currently earn R15,000 per month, and apply the 80% rule, you will need at least R12,000 per month after retirement to maintain your current living standard. Unlike food products, human beings don’t have a “use by” date, so we have to rely on a safe withdrawal rate to ensure that we do not outlive our savings, said Louw. According to this rate, you should be able to withdraw 5% of your portfolio yearly without having to use any of your remaining capital, he said. “This approach is based on the fact that the historical return on the South African stock market (since 1964) was about 8% higher than the local inflation rate and that you would expect to earn slightly less than that in a typical balanced fund portfolio. “By limiting your withdrawals to 5% of your portfolio, you should still have an additional 5% to 6% growth to cover inflation in the long run.” Based on a 5% annual withdrawal rate after retirement, Louw said that the amount you will need to save in rand terms would look something like this: R12,000 x 12 months = R144,000 (annual income) ÷ 0.05 (5% safe withdrawal rate) = R2,880,000. If you don’t properly compensate for inflation in your portfolio, you may fall short of your required total after retirement, said Louw. “Let’s assume that you are 40 years old and you plan to retire at age 65 (25 years). By using the top of the South African Reserve Bank’s target range, the best-calculated guess we can offer on annual inflation is around 6%. The 4% rule Traditionally, financial advisers, savers and retirees have relied on the 4% rule when working out how much to save for retirement and what kind of annual income retirement savings would provide, noted financial services group Discovery. Simply put, the rule says that if retirees withdraw 4% of their savings annually (adjusting this amount for inflation every year thereafter), their nest egg will last at least 30 years. The rule also requires retirement savings to be split equally between shares and bonds. This method, Discovery said, is also used to determine the lump sum investors need to provide an acceptable annual income when they retire. For example, if you retire with a final salary of R480,000 a year, you need a replacement ratio of 90% of your final salary, which amounts to R432,000. To ensure you do not use all your saved retirement capital in 30 years, R432,000 should be 4% of your total savings, Discovery said. This means you would need R10.8 million saved to draw 4% or R432,000 annually. Put another way:

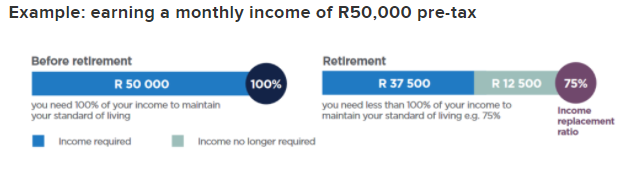

For example, Bengen’s rule is based on the average long-term annual returns (since 1926) of shares and bonds being 10% and 5.3%, respectively.  75% rule Plan to have 75% of your current pre-tax income, says financial services firm, Sanlam. “You will most likely need less than 100% of your current income to live comfortably when you retire as some expenses fall away once you retire.” Ask yourself these questions:

Allan Gray offers a similar guideline around saving. Aim for an income of 75% of your final salary.

It is widely held that a retirement income equal to 75% of your final salary will allow you to live comfortably during retirement, it said. “This figure accounts for the adjustments many people make as they age, for example, no further retirement savings contributions but higher medical costs.” To assess how much you will potentially need, consider the following factors:

Aim to put away at least 17% of your salary from age 25 “Assuming that you will be comfortable living off 75% of your pre-retirement salary, our research indicates that saving 17% of your salary is a reasonable starting point for the 25-year old saver. “This amount increases dramatically the later you start. You need to save 22% if you start saving at 30, up to 42% if you start at 40, and up to 59% if you start at 45,” Allan Gray said. It is important to note that these numbers are simply averages and assume a consistent, inflationary salary increase each year, that you retire at 65 and that you earn an average return of consumer price inflation (CPI) plus 5%, it said. The 15% rule The general rule of thumb for a comfortable retirement is 15%, noted Gus Van Der Spek, a developer of upmarket retirement village Wytham Estate. “15% of your salary should be put aside for your entire working career of around 40 years. For those wanting to retire in luxury, 20%-plus is advised. Also, bear in mind that what R1 is worth now will differ by the time that you retire,” he said. Van Der Spek shared the advice given to him by financial planners saying, “multiply your needs by 300. Simply put, if you currently live on R50,000 per month, multiply this by 300 to determine what you will need to maintain a luxury lifestyle post the age of 60.” Van Der Spek’s comments dovetail retirement expert Andre Tuck, a senior Investment consultant at 10X Investments. Tuck pointed to three old school ways to ‘guesstimate’ your retirement goal:

He added, however, that if you are hoping to do things you didn’t do during your working years, for example, travel, you should rather multiply your final salary by 17, or even 20.

“The more money you have available to invest once you retire, the better your lifestyle will be and the more likely you will be to withstand the impact of unexpected events, such as the current pandemic,” he said. If you would like to speak to a Financial advisor about planning for your retirement contact Kevin tel(011)658-1333 email: service@daberistic.com Source: Businesstech In partnership with Morningstar, Let’s kick off the comparison with a quote by Ryan Holmes – “You can run a sprint or you can run a marathon but you can’t sprint a marathon.” The same principle can be applied to saving for retirement. Training to run a marathon is very similar to saving for retirement.  During 2017 the Minister of Finance issued the final retirement fund default regulations (commonly referred to as “Default Regulations”) made in terms of section 36 of the Pension Funds Act, 1956.

These Default Regulations, published in Notice 863 of Government Gazette No. 41064, were the outcome of an extensive consultative process between Treasury and the FSCA (the first draft was published back in July 2015) and intend to improve the outcomes for members of retirement funds by ensuring that they get good value for their savings and retire comfortably. Default Regulations The final default regulations amended existing regulations published back in 1962 and, in essence, introduce three sets of requirements: 1. They require the board of trustees of retirement funds to offer a default investment portfolio to contributing members who do not exercise any choice regarding how their savings should be invested (Regulation 37); 2. They also require the fund to offer a default in-fund preservation arrangement to members who leave the services of the participating employer before retirement (Regulation 38); and 3. for retiring members, a fund must have an annuity strategy with annuity options, either in-fund or out-of-fund, and can only “default” retiring members into a particular annuity product after a member has made a choice. The above listed defaults must be relatively simple, cost-effective and transparent and require the board of trustees to assist members during the accumulationand retirement phases. 1. Default Regulations Regulation 37: Default investment portfolios All retirement funds with a defined contribution category are required to have a default investment portfolio(s). The investment portfolio(s) that members are defaulted into should be appropriate, reasonably priced, well communicated to members, and offer good value for money. Trustees are required to monitor investment portfolios regularly to ensure continued compliance with these principles and rules. Performance fees will be allowed but subject to a standard to be issued by the FSCA and a regulatory or policy review. Loyalty bonuses are not permitted. For now, Regulation 37 does not apply to retirement annuity and preservation funds. 2. Regulation 38: Default Preservation and Portability Funds that have members enrolled into them as a condition of employment (i.e. pension and provident funds), will have to change their rules to allow for default preservation, as some of them currently do not allow resigning workers to leave their accumulated retirement savings in the fund. The employee, however, will have the right and option to withdraw, upon request, the accumulated savings or to transfer them to any other fund, thereby achieving portability. Employees will also be required to first seek retirement benefits counselling before they make a decision. Regulation 38 does not apply to retirement annuity and preservation funds. 3. Regulation 39: Annuity Strategy The boards of all pension, pension preservation and retirement annuity funds must establish an “annuity strategy”. Provident funds and provident preservation funds must only establish an annuity strategy if the fund enables the member to elect an annuity. The regulations define an “annuity strategy” as follows: “annuity strategy” means a strategy, as determined by a board, setting out the manner in which a member’s retirement savings may be applied, with the member’s consent, to provide an annuity or annuities by the fund or to purchase an annuity on behalf of the member from an external provider, which annuity or annuities may either be in the name of the member or in the name of the fund and which complies with the requirements of regulation 39 and any conditions that may be prescribed from time to time”; (my emphasis) In determining the fund’s annuity strategy, the board must consider (as far as it can reasonably ascertain): · the level of income that will be payable to retiring members; · the investment, inflation and other risks inherent in the income received by retiring members; and · the level of income protection granted to beneficiaries in the event of death of a member enrolled into the proposed annuity. The proposed annuity or annuities – which can be a life annuity or a living annuity (and can be either member owned or in-fund) - must be appropriate and suitable for the specific class of members who will be enrolled into them, must be well communicated and offer good value for money. Members will be entitled to opt into this annuity strategy by selecting the annuity product in which they wish to enrol (i.e. the member must indicate which annuity product he/she would prefer by opting in instead of opting-out). Members should also be given access to retirement benefit counselling to assist them in understanding and giving effect to the annuity strategy. With respect to a living annuity, the fund must communicate to members (on a regular basis) the asset class composition of investments, their performance and changes in the income in respect of the annuity. In addition, funds will need to ensure that all fees charged in respect of the proposed annuity are reasonable and competitive considering the benefits provided to members. The fund must review its annuity strategy at least annually to ensure that the proposed annuity continues to comply with the regulations and is appropriate for members. The new concept of “retirement benefits counselling”: what does it entail? The concept of “retirement benefits counselling” is defined in the regulations as “the disclosure and explanation, in a clear and understandable language, including risks, costs and charges…”. Regulation 39 states that members must be given access to retirement benefit counselling not less than three months prior to their normal retirement age as determined in the rules of the fund (and as may be prescribed). It however offers little guidance as to what exactly this service must entail. The FSCA subsequently published a guidance note providing more clarity on (inter alia) the concept of retirement benefit counselling. PFA Guidance Note No.8 of 2018 states that retirement benefit counselling may be provided either in person or in writing. In either event, the fund must retain a record thereof. The person providing counselling (as appointed by the fund) does not need to be a registered FSP or financial advisor in terms of FAIS, but the board must be satisfied that the person who provides the retirement benefit counselling is suitably qualified and experienced and able to properly manage any conflicts of interest. Retirement benefit counselling does not include advice, even on tax matters, and members should be expressly informed of this fact. If advice is also provided, then the person providing the advice must be a registered financial adviser or tax practitioner, as the case may be. It is recommended that retirement benefits counselling should be provided no longer than 6 months prior to a member’s retirement from the fund and the board should make every effort to ensure that the information provided is still relevant and appropriate at retirement age. When members are given access to retirement benefit counselling, a disclosure and explanation must be provided in clear and understandable language, including fees, risks, costs and charges of the available investment portfolios, the fund’s annuity strategy and any other options made available to members. As of 01 March 2019 all default arrangements in respect of a fund must be fully compliant. Funds must therefore ensure that their rules and investment policy statements are properly aligned to ensure compliance with the new default regulations. Source: Personal Finance, Lize de la Harpe a legal adviser at Glacier by Sanlam.  Delaying saving for retirement is not uncommon. Other life costs seem more important – there’s a wedding to pay for, a deposit for a new house to put down, a baby, school fees and that holiday you absolutely must take. And, even for those of us who have been forced to save (thanks to a compulsory pension fund or retirement annuity deductions at work), it might not be enough.

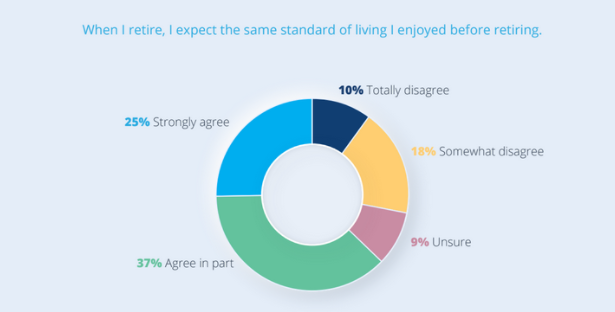

It certainly pays to start saving as early as possible, but if retirement is suddenly closer than you realised and you haven’t saved enough, it’s never too late to start. Make the most of your time It’s not only the amount of money saved that counts, but also when we start saving. The earlier you start, the more affordable the amount of money you need to put away each month will be. More than half of us only start saving at age 28, instead of when we start working. And there are many people who only start in their thirties, or later, when they hit 40. The thing is, it’s not just about “catching up’ savings over the last five/10/15 years that you've missed. That’s a tall order in itself. It's about making up the compounded returns you've completely lost out on! Imagine a saver, Xoliswa, who starts saving for retirement at age 25. (Please note that the following calculations illustrate a point about compounding and time, and do not account for inflation-adjusted increases in contributions.) Saving R5 000 a month, at an average 6% return per year over time, she’ll have more than R7 million by age 60. Mark starts saving at age 35. He will only have R3.46 million at age 60 less than half what Xoliswa saved. To get anywhere close to Xoliswa’s amount, he’ll need to save R10 000 a month to reach R6.9 million in his 25-year investment horizon. Starting even later – at age 45 – and you’re in an even more difficult scenario. Even saving R20 000 a month – four times what Xoliswa started saving at age 25 – won’t even get you to R6 million. That’s why it’s so important to follow Xoliswa’s example and start saving for retirement as early as you can. But even if you’re starting saving late, the most important thing is that you’re starting. How much do you need? Figuring out how much you should have saved is tough. The general rule of thumb in South Africa is that you’ll need to be able to replace 75% of your income to retire comfortably. This assumption relies on the fact that you won’t have a home loan or any other large debt by that age, which means your monthly expenses will be lower. But, increasingly, financial planners are beginning to work on a 90% replacement ratio (especially since medical expenses tend to rise after retirement). Assume you’re retiring today with a final salary of R40 000 a month (R480 000 a year). To replace 90% of your salary, you would need R10.8-million saved to maintain your standard of living (note that this amount also takes account of the 4% rule, which we will discuss in more detail in a later article). Most people will be very lucky if they have three-quarters of that. Boosting your savings So, if you’re nearing retirement and you’ve come to the conclusion that you need more savings to retire comfortably, you need to consider the following points:

To start saving for your retirement, please contact Kevin or Ray, email: invest@daberistic.com tel no: (011 658-1333) Source: Discovery |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|