Budget 2017 was unusual due to the tough economic environment in 2016 and SA narrowly having avoided going into recession, according to independent economist Sandra Gordon.

She was the guest speaker at the monthly networking forum of the Western Cape Business Opportunities Forum (WECBOF) on Wednesday evening. "The slow SA economy has led to little revenue, which put a squeeze on Treasury. Ratings agencies are concerned that SA is building up debt so quickly and the country sits right on the line between being investment grade or junk," said Gordon. "If SA is downgraded to junk status it will raise the cost of borrowing. It can take up to seven years to get out of junk status. Budget 2017 was, therefore, so tight and constrained that the consensus is that SA won't be downgraded in the first half of 2017." Treasury has indicated that the path SA is on at the moment is not sustainable. That leaves the question of how economic transformation could be achieved. "Budget 2017 was more of a political vision. Resources are so limited that there is not much government can do for SMEs until the economy gets better," said Gordon. "That is why I think it is not worth waiting for government to do something for SMEs." At the same time, she said there is an improved economic outlook for 2017. This could mean that interest rates are cut later this year or early next year. "Entrepreneurs should be aware of how things are changing," concluded Gordon. Written by : Carin Smith Source: Fin24

0 Comments

“In these tough times we draw strength from the resilience and diverse capabilities of our people, our business sector, our unions and our social formations.”Pravin Gordhan, Budget Speech 22 February 2017

Personal tax

Business and trusts

Employers

Retirement reform

Other tax proposals

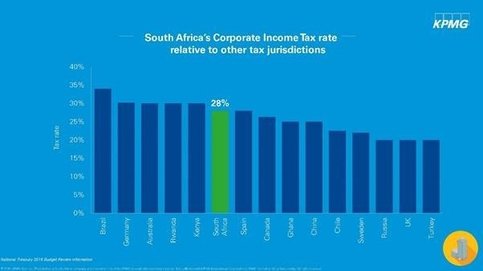

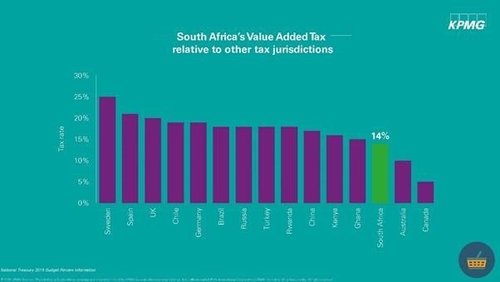

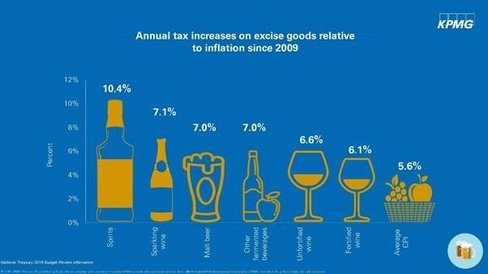

In the march newsletter we will be focusing on on the 2017 Budget speech. This month we look predictions made by experts. Below is an article on views by Analyst before the budget speech. In the mini budget last year, Finance Minister Pravin Gordhan explained that additional revenue would be sourced through various tax increases. This is in the face of slowing economic growth and falling tax revenue collection. Analysts, senior economist at KPMG South Africa, Muziwethu Mathema and Grant Thornton’s director and leader tax Eugene du Plessis share their expectations of where they think Gordhan will find the “additional” revenue. Personal Income Tax (PIT) KPMG: PIT accounts for 35% of tax revenue. In SA, higher income individuals pay a higher proportion of tax, which means Gordhan would increase taxes for these high income earners to generate significantly higher revenue. This can be through the introduction of a 45% marginal tax rate for individuals earning above R1.5m per annum. Treasury could raise between R75bn and R10bn through this approach.  Grant Thornton: To avoid a VAT hike, increasing the tax rate for higher income earners is likely. Treasury may add a percentage to the top tier bracket. Or government may reduce the bracket creep adjustment, but this may result in a higher effective tax rate. If the bracket creep adjustment is chosen, to compensate for higher inflation pushing up income into higher brackets, it could offset or avoid a VAT increase. Corporate Income Tax (CIT) KPMG: Treasury is unlikely to raise CIT given the weak macro-economic environment. Increasing the CIT rate will be uncompetitive. SA’s current statutory tax rate is already higher than most tax jurisdictions, Treasury could lower the tax rate to attract investment.  Value-added Tax (VAT) KPMG: SA’s VAT rate is low compared to other tax jurisdictions. A one percentage point increase in VAT could generate R15bn in additional revenue. However raising VAT could have a negative impact on inequality, real GDP growth and inflation, according to the Davies Tax Commission First Interim report.  Grant Thornton: Treasury may be considering a VAT increase. If this happens government would have to take measures to minimise the impact of a VAT increase on poor households, for example through increasing social grants. An alternative option would be to introduce a dual or multiple-rate VAT system, where VAT is increased on luxury items and be lower on other items, and maintain a zero rate on basic items. But the costs related to the administration of this approach outweighs the benefits. There may also be a political fallout following the increase in VAT. Specific Excise Tax KPMG: Treasury is likely to introduce higher-than-inflation increases in sin taxes, which could generate between R5bn and R7bn. But increasing this tax may result in an increase in black market consumption. The sugar-sweetened beverages tax could generate between R2.5bn and R4bn. However the job losses incurred in this second may negatively impact PIT and CIT tax bases.  Grant Thornton: The proposed sugar tax is supposed to come into effect on 1 April 2017, but the process is still underway. The tax may be deferred and is unlikely to contribute to the fiscus any time soon.

Fuel levy KPMG: Treasury is not likely to increase the fuel levy. The higher crude oil prices also limit Gordhan from increasing the levy. The fuel levy could raise between R5bn and R7bn. Grant Thornton: An increase in the fuel levy could be another source of revenue. Although this may negatively impact poor households, it would be much “easier to sell” than a VAT increase. Other adjustments KPMG: Gordhan could provide reduced tax relief to short-term revenue. In Budget 2016, Treasury raised R7.6bn through this option. Failure to give tax relief over a sustained period is regressive. Gordhan may introduce adjustments to wealth-related taxes, similar to last year’s property taxes. Grant Thornton: The Special Voluntary Disclosure Programme, which involves exchange control and tax relief, may raise funds. The Davis Tax Committee is also looking at interest-free or low interest loans made to a trust will. Under certain circumstances where this results in donations, tax must be paid. But this is unlikely to make an impact on tax revenue collection this year. The committee is also considering the viability of wealth taxes. There may also be new measures related to transfer pricing and common reporting standards to avoid illicit transfer of funds to ensure tax revenue collection. Written by: Lameez Omarjee Source: Fin24 |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|