As many South Africans are taking note of their spending habits and looking for the best ways to save money. We understand you may want to cut back on a few things, but one thing you should never cut back on is quality insurance. Cheaper insurance options could save you some cash in the short-term, but will usually end up costing more in the long run, especially if you aren’t properly covered. You can still get affordable cover without compromising on quality. Here are some savings tips to ensure you enjoy affordable car insurance, house insurance and building insurance. Get the best car insurance premiums

More affordable home insurance

Budget building insurance cover

Check in regularly on your insurance cover It’s very important to do a regular run-through of your lifestyle, profile and assets as these are the factors that determine how much you are charged every month. Things change all the time – for example, you may have installed extra security measures around your home and not told us, changed jobs, gotten married or had a child move to university. Simply by updating your profile, you may find that your premium decreases or that your risk profile has changed. Remember that a car depreciates in value every year. Ensure that the insured amount reflects the reasonable market value of your vehicle as you will only be paid the insured amount or reasonable market value (whichever is the lesser of the two). To review your current policy or get a comparative quote contact Marizka from our Short-term department, Tel: 011 658-1333, email service@daberistic.com Source: Santam

0 Comments

The economic downturn over the past year, coupled with the need to reduce expenses, has seen a rise in vacant properties across South Africa and an increase in co-habiting. Taking the decision to move in with a housemate or your partner is a big step. It’s wise to consider the emotional, financial and insurance implications and have critical conversations upfront.

Marius Steyn, Personal Lines Underwriting Manager at Santam, and Marius Neethling, Manager Personal Lines Underwriting (Systems and Administration) at Santam, caution that there are a few considerations people need to think about when merging households. “In the scenario where you move in with your partner, an insurer usually considers you the equivalent of a common-law husband and wife, depending on the seriousness of your relationship. That means you can take out a policy together. If you are moving in with a housemate, both parties will need their own separate insurance policies. In this case, you will have to insure your own belongings and communal living underwriting rules will apply. In both cases there are lots of logistics to tick off – like making sure the household contents are covered.” Here, Steyn and Neethling chat through the checklist to tick off before co-habiting: Make sure you’ve adequately covered the combined contents of your home: Moving in together often results in a staggering amount of ‘stuff.’ Which means you and your partner or housemate will probably need to update the household contents insured amount. If your relationship is seen as serious (insurers look for things like how long you’ve been together, if you’ve co-purchased furniture, etc.), then an insurer will treat you the same as they would a married couple. This means you can take out a policy between you, with one person being the main policyholder and the other, the additional insured. Some considerations:

If you happen to have a fight and temporarily move out… It’s not commonly known, but, if you happen to argue and temporarily move out and take some of your household contents with you, these items will still be covered in your temporary abode, providing this is a private building – not a tent or caravan, for example. This only applies to a temporary situation though – if it’s a permanent split, then you’ll need your own new policy. Vehicle insurance is also important: Remember to add your partner as a regular driver on your policy if he or she uses your vehicle more frequently than you do. If it really doesn’t work out: If, sadly, the relationship comes to an end, then you should get your own policy as soon as possible, especially if you have one policy between you, but you’re not the main policyholder. Remember, if you’re the additional insured, it’s up to the policyholder to pay you in the event of a claim, which could get difficult if you’re not together anymore. If you would like to get a free quote comparison please contact Marizka in our Short-term department email: service@daberistic.com, tel: (011)658-1333 Source: Personal Finance  Discovery Insure is celebrating 10 years of bringing clients the very best in innovative and rewarding car and home insurance. Now Discovery Insure is bringing more rich enhancements to clients, while continuing to reward clients for driving less and driving well. These enhancements include benefits to protect the whole family, such as updates to our car seat benefit, a unique safety feature, new tools for driving safely, and more. 1. Keeping our children safe on the road with enhanced car seat discounts. Having the correct car seat can significantly reduce your child's risk of injury or fatality if you are involved in a vehicle accident. Discovery has DOUBLED the discounts on car seats from partners: Toys R Us and Born Fabulous. Vitality Drive clients can get up to 50% off car seats, based on their Vitality Drive status. In addition, you will also have access to a wider range of car seats, making child safety on the roads much more accessible. There is also an extension on the benefit to give clients the opportunity to replace a damaged car seat in the event of a motor vehicle accident at no additional cost The increased discount is available from June 2021 onwards. The car seat replacement benefit will be available in 2021, quarter 3. Read more about the car seat benefit and how to redeem your voucher. 2. The Discovery Insure Driving Academy Being at the forefront of innovation and technology, the Discovery Driving Academy places the driver in an artificial environment which is designed to mimic an actual driving experience. The simulator itself mimics a real car and includes an accelerator, brake, clutch, gearbox, indicators and windscreen wipers. The Discovery Driving Academy allows drivers to have:

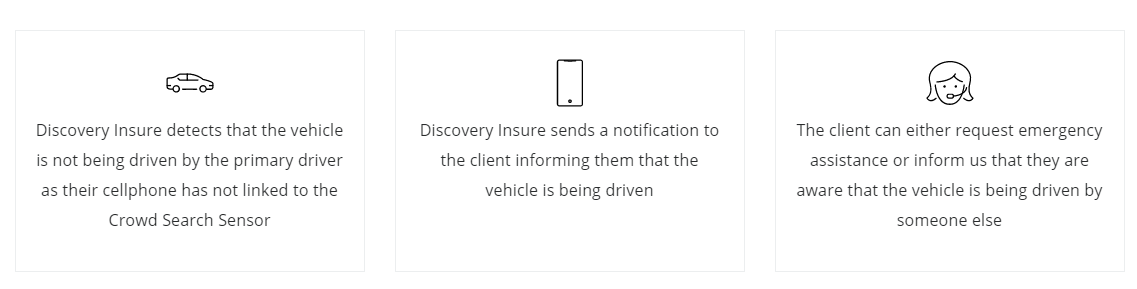

Courses available The Discovery Driving Academy is available to all members of the public. Discovery clients get 25% off the course fees but as a Discovery Insure client, you get a 50% discount. Other courses for other levels of experience will soon be added. The Driving Academy can be found at 1 Discovery Place, and will be available from April 2021. Bookings we will be available on the Discovery website. 3. Additional protection with Motion Alert for the Crowd Search Sensor Vitality Drive clients automatically have access to state-of-the-art safety features. The Crowd Search Sensor now offers an additional layer of protection using new telematics technology. How it works Motion Alert uses the latest telematics technology to identify when your phone is not in the vehicle at the time that the vehicle is moving, thus alerting you to possible theft of your vehicle.  4. New services with Vitality Drive Vitality Drive is Discovery Insure's unique driver behaviour programme that rewards you for driving well. In order to help you manage your driving behaviour even better, Discovery has upgraded the monthly Vitality Drive performance dashboard effective from May 2021. What's new on your Dashboard? You will be able to view:

At the Drive Centres, you can:

Keep an eye out for your new personalised Dashboardand visit www.discovery.co.za to find the location of the Discovery Drive Centre closest to you. 5. Upgrade to the latest Apple or Samsung cellphone every year With our Purple Plan, you can upgrade to the latest Apple or Samsung cellphone every year! We are excited to announce that we have a brand new partnership with Cellucity in addition to our partnership with iStore. To qualify for the cellphone upgrade, you must have:

If you qualify, email the Discovery Insure Partners team at dipartners@discovery.co.za and Discovery Insure will provide you with a voucher of R10 000 which you can use at any iStore or Cellucity. You will need to pay any amounts that are more than the R10 000. If you choose to trade in your existing cellphone, it will contribute towards the cost of the new cellphone. We are excited to give you this update and we are sure that you will get great value from it. Get more information about Discovery Insure's Purple Plan cellphone upgrade benefit. 6. Keeping your personal information safe As a valued client we would like to make sure you experience the best service, stay informed and have access to all the information pertaining to your insurance plan. This is why we are gradually changing the way we communicate with you in accordance with the POPI Act. Going forward, all communication that contains personal information will be accessed via a secure log in on the website or on the app. Follow this guide on your personal information to make sure you have updated your contact details and security settings on the website and mobile app. Source: Discovery Insure

Author: Marizka Esterhuizen, Insurance Broker The main function of insurance is to put the insured into the same position as they were before a loss or accident. Santam states on their website that: “The retail value of a car (which is usually the higher value of the two) is the average price a car dealer would sell it for. In insurance terms, this means that if your car is covered for its retail value and it is written off in an accident or stolen without being recovered, the settlement amount will be based on the car’s retail value. If your car is insured for its retail value, it will be much easier to replace a damaged or stolen car with a similar make and model. The market value of a car is almost always lower than the retail value and takes into account a number of variables, including mileage, vehicle condition, service history and accident reports. If you were to sell your car privately, the market value would be the price that you could likely sell it for. Because this figure can vary from car to car, short-term insurers need to find a way to standardise the market value. The reasonable market value uses the retail value as the base and takes into account the amount of kilometres on your car’s odometer, the condition of the car as well as any extra items added to the car.” Therefore, if you insure your vehicle at market value you will not be able to replace the vehicle with a similar vehicle, leaving you in a worse position than before the loss or accident. You can use the calculator on Santam’s website to calculate the retail value of your vehicle by using the Auto Dealer Code, or your vehicles exact specifications, e.g. year, make, module etc. The Auto Dealer code was developed by TransUnion to specify vehicles. TransUnion has been gathering data over five decades and updates their data monthly to ensure that they provide accurate information in their guides. These guides are used by insurance, financing, and motor trader companies. “Can you please also explain why the Honda Jazz is insured for a less value, but the monthly insurance is higher than the Jeep Compass?”Insurance companies uses various factor that impact the rate at which the insurance premiums are calculated. These factors include, but are not limited to, the regular driver, vehicle specifications and the claims history.

Insurance premium rates are calculated by actuaries every year using data collected over the previous years. With today’s technologies and the vast well of data available, insurance companies have moved over to a client specific risk-based approach. Meaning that insurance rates are calculated per individual with vehicle insurance, insurance companies look at the regular driver, taking into account the following factors: • Age • Marital status • Gender • Occupation The vehicles specifications also play a role in calculation the rate. For example, older vehicles have been on the road longer and are therefore more prone to breakdowns, the parts are harder to find and therefore more expensive even if their retail value is lower than other vehicles. Hijacking statistics are also used, as a result vehicle like VW Polo’s that are more likely to be hijacked, have higher insurance rates. Insurance companies look at the following factors: • Year the vehicle was manufactured • Vehicle module • Vehicle make • The colour of the vehicle • Extras on the vehicle • Vehicle security • Where the vehicle is parked in the day and at night The claims history of the driver is used in calculating the rate for the premium, a higher loss ratio will result in a higher premium. • Your loss ratio, which is the losses an insurer incurs due to paid claims as a percentage of premiums earned. • Your loss ratio is calculated by dividing the claim amount by the annual premium. In conclusion, there are various factors that can result in the premium for the Honda Jazz being higher than the Jeep. To get help and advice on your car insurance, please contact 011-658-1333, Option 3, email service@daberistic.com to speak to one of our insurance brokers.  Discovery announced a number of key product enhancements that respond specifically to insurance needs around COVID-19, as well as the results of two critical research papers on COVID-19 in South Africa.

Hylton Kallner, Discovery South Africa CEO says, “Our response to the COVID-19 pandemic has been guided by our core purpose of making people healthier. In the context of this pandemic, it is more critical than ever that we work hard every day to support clients with access to healthcare cover and comprehensive financial protection, and that we provide them with the necessary tools to promote behaviour that encourages healthy lifestyle choices.” The Group earlier introduced healthcare cover specific to COVID-19 through the WHO Global Outbreak benefit and tailored Vitality to help encourage people to stay healthy and active at home. In partnership with Vodacom, the Group made online doctor consultations available to South Africans through a virtual healthcare platform that gives free access to reliable information, risk screening and the ability to effectively ‘dial a doctor’ from the safety of their home. Kallner explains, “Discovery has access to one of the largest population data sets on a variety of factors relevant to the COVID-19 experience. Ranging from clinical, to financial and behavioural data, we are in a unique position to understand the long-term impact of COVID-19 in South Africa, and to design the necessary product structures to better support clients.” Together with emerging experience from other parts of the world, Discovery data highlights the importance of regular screening, appropriate testing and understanding and managing an individual’s health risk. This has informed the expansion of new benefits in response to changes brought about by COVID-19. These provide clients with proactive risk monitoring and assistance; providing cover for different severe illness outcomes due to COVID-19; adequate health protection over a longer term; and rewards that adapt to new lifestyles. A new COVID-19 risk assessment tool to be made available to all South Africans “We have undertaken the analysis to create an accessible COVID-19 risk assessment tool, that will be released on the Discovery app and the website helping people to understand their risk for COVID-19, to know their health risks that increase the likelihood of hospitalisation, and access funding for testing and health monitoring for those at a high risk for compilations,” says Kallner. The assessment will look at a member’s risks compared with that of the membership base in an area. “Members will be able to complete the assessment over time and keep track of their history. When testing is recommended, the assessment tool guides them to an online doctor consultation in a network. More than 6 500 members of Discovery Health Medical Scheme (DHMS) have consulted with their doctors online over the past couple of months, helping to contain the spread of the virus,” he says. “What we know now is that high blood pressure, cholesterol, blood glucose and body mass index are leading risk indicators of developing complications. We want to help members on all health plans to understand and manage these factors to mitigate the risk of complications from COVID-19. From June, any result from a Vitality Health Check that places someone at a high risk for complications will trigger a referral for advice through one online doctor or nurse consultation in the network, which the Scheme will fund in full,” says Kallner. In addition to the forthcoming COVID-19 risk assessment tool, other key enhancements announced by the Group include: Discovery Health expands access to fully funded COVID-19 testing and high-risk monitoring The WHO Outbreak benefit, first announced in early March, has been enhanced further to provide comprehensive cover for COVID-19 over the longer term. It now provides cover for two PCR tests for each beneficiary in a year, following screening by a healthcare professional and will be funded from the risk benefit regardless of the result. Healthcare professionals who are members of DHMS, will have cover for four PCR tests in a year. Discovery Health will assist members at higher risk of COVID-19 complications with funded telephonic consultations with a wellness specialist to monitor their current physical and mental wellbeing and make referrals to virtual healthcare services. DHMS will fund a pulse oximeter– used to monitor oxygen saturation from an early stage – for members at high risk of COVID-19 complications. This will be funded in full if obtained from a network provider. Members will also have access to three consultations with a wellness consultant to monitor oxygen and make a referral to a GP when necessary. Employer groups also have access to a variety of benefits that can help to manage COVID19 in the workplace. A comprehensive information hub, management of high-risk employees, contact tracing and access to screening and online doctor consultations are all available to employers through Discovery Healthy Company. Discovery Insure rewards clients for driving less Premium cash back even when driving shorter distances through the Dynamic Distance cash back that rewards low kilometres. Clients can earn up to 25% motor premium cash back every month when they drive between 0km and 249km in a month and they can still earn up to 50% fuel cash back when they drive more. Vitality Drive Active Rewards has been enhanced so that a client’s drive goal each week is based on their driving behaviour and not on the number of kilometres driven. Discovery Vitality tailored for seniors Vitality Health Check tailored for people aged 65 years and older, recommending specific and age-appropriate health screenings, preventive tests and vaccinations, including a risk assessment score for COVID-19. Three clinically validated screening tests help with early detection of age-related risks of hearing loss, visual perception, and balance and leg strength to prevent injuries from falling. The standard set of preventive tests follow, which include blood pressure, blood glucose, cholesterol, weight and smoking status. The acceptable ranges for weight and blood pressure are altered to consider the changes at an older age. Preventive steps include recommended vaccines such as the flu vaccine and the pneumococcal vaccine to prevent pneumonia. Results are summarised in reports and provide targeted health tracking, clinical risk projections and healthcare referrals based on the health assessment. It can be accompanied by a Vitality Functional Assessment which is an eight-part physical assessment to identify the risk of early frailty or disability and offers tailored workout routines to support healthy ageing. Discovery Life enhances Severe Illness Benefit to automatically cover multi-organ complications associated with COVID-19 Clients have full cover for COVID-19 related claims under their Discovery Life cover. A new multi-organ benefit has been included as a category under the Severe Illness Benefit to provide relevant cover for the complications associated with COVID-19. COVID-19 presents varying respiratory, cardiac, renal and liver complications. The multi-organ benefit is a category within the Severe Illness Benefit and complements existing severe illness body systems to provide payments by the level of acute multi-organ failure, resulting in payments of 50% to 100% of the severe illness benefit. Discovery Life is also taking a proactive approach to providing cover and is currently tracking 203 clients who haveCOVID-19 to manage claims from any of their available Life, Severe Illness and Income Continuation Benefits. If you would like more information on any of the products please contact Koketso email: info@daberistic.com tel:(011)658-1333 Source: Discovery  Everyone’s worried about their finances right now, but it’s vital that you don’t cancel your insurance or default on your insurance premiums.

This will not only put you in a difficult financial situation if something valuable is damaged or stolen, it’ll also affect your ability to get insurance, or any form of credit, in the future, as your credit score will be impaired. “It’s hugely risky to cancel your insurance, as a time of crisis is when you actually need insurance the most. And don’t just stop paying: Bad credit decisions can come back to haunt you later. But there are several things you can do to make sure you pay the lowest premium possible, especially during lockdown. Talk to your insurer now and make a plan in the short term, rather than suffering long term consequences,” says Wynand van Vuuren, partner of customer experience at King Price. Defaulting on your insurance premiums will see you being reported to the credit bureaux for non-payment, which will negatively affect your credit score. A credit score is a 3-digit number that helps lenders evaluate how safe or risky you are as a customer. It’s based on the information contained in your credit report, which is a history of all the loans and credit you’ve ever taken, and how you’ve paid them back, as well as how reliable you are with your other monthly payments. So why does your credit score affect your insurance premium? Insurance companies use a range of factors to assess your risk and determine the premium you will pay. For a car, these include the security measures where you park your car; the age, make and model of the car; your age and driving history; your accident and claims history – and your credit score. “You may not realise it, but your credit score is a powerful predictor of your financial behaviour. It shows lenders and financial institutions how likely you are to pay your bills and default on debts. As such, when it’s combined with other factors, it tells an insurer how risky you would be to take on as a client, and this risk will be reflected in your premium,” says Van Vuuren. According to insights and data company TransUnion, the biggest influence on your credit score is your account payment history – that is, how you manage your accounts and whether you make the monthly payments on time. To improve your credit score, focus on paying the full instalment of every bill on time, so you’re offsetting past negatives with more recent positives. It also helps to maintain a healthy mix of credit – store accounts, credit cards, a home loan, and service contracts such as cell phone accounts – to establish a good credit history. The bad news is that a negative credit score can take 2 years to fix. The good news is that it’s easy to obtain your credit report. You can download your credit report once a year, for free, from TransUnion. Source: FA News  Below are the different premium relief options announced by short-term insurance companies on car insurance, due to Covid-19 lockdown. It stands to reason that insurance companies should cut the premiums during this period, as people stay at home and do not drive, hence much fewer motor vehicle accidents and claims. This is good news for consumers under financial distress:

Discovery Insure Discovery Insure is offering a Motor Premium Relief Benefit to all Discovery Insure personal and business insurance clients during this time. The Motor Premium Relief Benefit will apply to May Discovery Insure motor vehicle premium and will be based on how much you drive during the month of April, as follows - If the client drives less than 500 km in April, they will receive a 25% discount on their May Discovery Insure premium for that vehicle - If the client drives more than 500 km in April, they will receive a 15% discount on their May Discovery Insure premium for that vehicle Santam There is a premium-relief support for a maximum of two months. Please see below the qualifying criteria for premium-relief due to unpaid premium as a result of the lockdown (Covid-19): - On risk with Santam for minimum 3 years. (Clients under 3 years to be referred) - No unpaid premiums in the last 12 months (up to and including March 2020) - Loss ratio below 70% over 3 years for Personal lines - Loss ratio below 65% over 3 years for Commercial Lines - Three claims or less in the 3 years excluding CAT claims Momentum A premium pause option will be available during, and continue after, the lockdown period. Upon reinstatement of the premium at any point, following the pause, MSTI will not deem the period as a break in cover with MSTI, which otherwise might impact the clients’ risk profile. Pro rata premiums will be charged from that day onwards and cover will be reinstated. Here is a list of discounts on premium offered by other insurers Standard Bank 25% Outsurance 15% Miway 10% Old Mutual iwyze 7.5% This compares favourably with international peers in the US, UK and Australia. If you would like us to do a comparitive quote please contact Edmond or Rethabile email: shortterm@daberistic.com tel: (011)658-1333 |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|