As a most loved local business, your clients rely on you to keep your doors open - even when disaster strikes. Business interruption insurance is designed to protect your business against lost profits should your property be damaged or destroyed by fire or natural disasters like flooding, earthquakes or tornadoes. Here are five must-know facts about this type of cover to safeguard your profits.

1. It’s cover added on to existing business insurance cover In order to have this type of cover, you need to have fire or property business insurance in place. While property insurance covers physical damages, business interruption insurance covers the profits you would have earned if it was business as usual. 2. Must-have for most types of businesses as part of their survival plan Can you imagine keeping up with orders if your most important piece of machinery burns down? Can you fathom having to close your doors for months – while still paying all your staff and bills? After working so hard to build up a fan base, can you imagine them going to your competitors? Most businesses should see business interruption insurance as a must-have survival plan. Work with your broker to plot out your worst-case-scenario and how you would deal with a disaster, especially for:

3. What business interruption insurance covers...and what it doesn’t A business interruption insurance policy will be tailormade to your business operations and turnover, but typically covers the following: Profit: You will receive funds to cover the profits you would have earned during the time you had to close your doors. This sum is based on the income of previous months and the forecast of trends in the future. Temporary relocation: While your premises are being repaired, it will cover costs for you to move to and operate from a temporary location. Fixed operational expenses: Based on historical costs, the policy would cover any expenses and costs that you continue to incur even though you’re not operating. E.g. wages, water, lights. Fines and penalties: Covering costs to service providers including any fines or penalties for being in breach of contract.

4. Accurately calculate your gross profit One of the common pitfalls of business interruption insurance One of the common pitfalls of business interruption insurance - where businesses find themselves underinsured - is when they don’t properly work out their gross profit. Your broker will help you ensure that this amount includes VAT and reflects either a 12-month period (if your maximum indemnity period is 12 months or less) or multiples of the annual turnover (where the maximum indemnity period is more than 12 months). There is a difference between what you know as a Financial Gross Profit, and an Insurance Gross Profit. The latter excludes costs/expenses that vary in direct proportion to a change in turnover. Examples are purchases, bad debts, discounts allowed and direct commission. If, for example, turnover or sales dropped by 10%, so would each of these costs. 5. Work out a sufficient indemnity period Your broker can help you set the right indemnity period for your business. This should allow you enough time to remove damaged property, replan your business (including getting building plan approval), reorder stock and machinery, rebuild your property (including any installations), recover lost markets and restore your turnover to what it would have been had the disaster not happened. Remember, there is no one-size-fits-all approach to getting a business back on its feet. With Santam’s small business insurance solutions, we can help you protect the business you’ve worked so hard for. Speak to your broker to find out more about the essential insurance cover for your unique business needs. If you would like to get a quote for your Business Interruption , please contact Edmond in our Short-Term department, email shortterm@daberistic.com , tel (011)658-1333 Source: Santam

0 Comments

As we enter the holiday season, many South Africans will be heading off for a well-deserved break. But, it’s also that time of the year where we need to take extra safety precautions. Here are some holiday safety tips to help ensure your clients are doing all they can to minimise risk.

Safety at home Burglaries and damages are on the rise during the holidays. That’s why it’s important that your clients are properly covered if something goes wrong. Here are some steps they can take before they lock up and go:

We offer SOS services including roadside assistance, route assistance and home drive assistance, as part of our vehicle cover should anything happen on the road. Help your clients prepare properly by sharing these road safety tips:

Safety for small businesses Smaller businesses are often cash-intensive which makes them especially vulnerable to crime during peak holiday season. If your client is a business owner, there are some precautions they can take to ensure they are protected and prepared for any potential criminal attacks:

Source: Santam  In this article, we focus on Excess – the amount which you have to pay when you claim from your insurer (whether you are at fault or not) unless if you have elected to pay an additional premium for an excess-free policy. So, what exactly is an excess and why do insurers apply these charges to insurance claims?

What is an excess? An excess is the uninsured portion of your loss or that portion of the claim you must pay for. When the amount that is claimed is less than the excess, no payment will be made by your insurer. Why do you pay an excess? Insurers use excesses as a way to make sure that you do not claim for every small loss. They do so not only for their own benefit but for all policyholders to ensure that insurance does not become unaffordable, because eliminating these claims and their associated costs helps keep premiums lower for you. An excess also acts as an incentive to ensure that you take responsibility for the safety and security of your possessions. Are there different types of excesses? There are many different types of excesses used by insurers. As a general rule of thumb – the lower the premium relative to the market standard the higher the excesses. Examples as follows:

The insurer needs to bring to your attention, when the contract of insurance is entered into, the standard excess and all other excesses that may be applicable when you claim. You can always enquire from your insurer if an excess can be completely done away with. This is referred to as an excess waiver. The important thing is that you understand why and when you pay an excess so that you can make an informed decision when taking out the insurance. Does an insurer have to recover the excess you paid? If someone else has caused your loss, the insurer may be able to recover the cost of the claim, including the excess you paid, from them or their insurer. The success of a full recovery however depends on several factors, including whether you identified the other party, whether they admitted fault, whether there are any witnesses, whether they have insurance and, if not, whether they have the ability to pay. What if your insurer does not recover the excess you paid? If the insurer decides that it is not going to attempt a recovery of the claim cost or it does not succeed in making a recovery, the insurer should advise you so that you can decide whether to attempt a recovery of your excess yourself. With the consent of the insurer, you may then proceed to recover your excess directly from the third party. We at Daberistic believe that by providing the right advice and solution to clients, we can create win-win relationships which will ultimately benefit everyone. If you are looking for advice on your short-term insurance needs, you can contact us on the following channels:

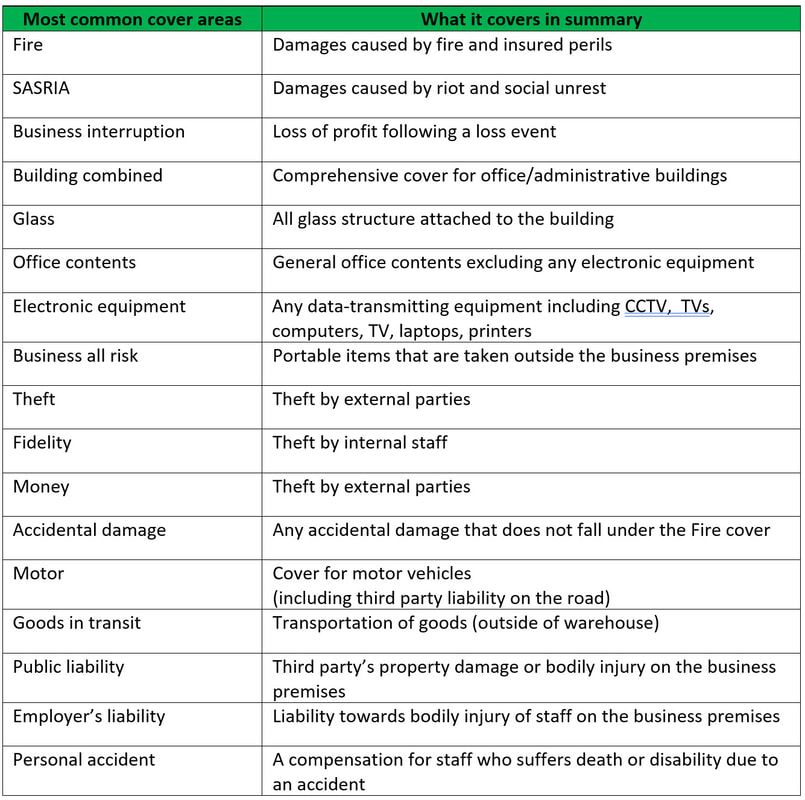

Author: Edmond Lee Commercial insurance is a necessity for business owners, but at the same time it is a rather complicated area to understand. We at Daberistic believe in simplifying insurance for our clients, so this article will shed some lights on the basic structure of commercial insurance in South Africa. In the early eighties there were many short-term insurers, flooding a variety of commercial insurance policy wordings onto the market. A sensible comparison of benefit between these policies was virtually impossible, which was to the detriment of the small business insurance consumer. Hence the regulator responded by introducing a standard business policy - known as "Multimark" - in 1987. Over time, Multimark was revised, and today we have the Multimark 3 wording available to us. Even though insurers have since introduced various endorsements to differentiate their products, the basic structure remain largely the same, as the Multimark’s risk-based approach is a solid foundation which ensures that various sections in the policy cover various risks and premium are calculated accordingly. As an example, Fire has a low probability of occurrence but high severity (i.e. all stocks can be affected) if it occurs, as opposed to Theft which has a higher probability but lower severity (because robbers or burglars cannot possible steal all your stock), which explains why covers are broken down into various section. Below is a table summarising the various key sections and their cover areas.  The scope of commercial insurance is broader than the above and continues to evolve as the risk landscape changes, resulting in other covers such as Products liability, Directors’ and Officers’ liability, Cyber crime, Commercial crime, Credit insurance – just to name a few. It is therefore crucial that you make use of an insurance advisor who can advise you on your risks and propose covers that meet your needs.

We at Daberistic believe that by providing the right advice and solution to clients, we can create win-win relationships which will ultimately benefit everyone. If you are looking for advice on your short-term insurance needs, you can contact us on the following channels:

Excess payments are among the most contentious aspects of car insurance. Here are answers to common questions about insurance excesses and tips to check on whether you have the right policy for your risk exposure and your pocket.

What is an insurance excess? The excess is an amount of money that will come out of your pocket when you claim against your car insurance. For example, if you have an approved claim of R100 000 and your excess is R5 000, you will pay R5 000 and the insurer will pay R95 000. If your excess is R5 000 and the cost to repair to damage to your car is less than R5 000, you will need to pay the full amount. Why do insurers charge an excess? The excess is a way for insurers to ensure that the cost of premiums remains affordable. Without an excess, insurers would need to process high volumes of small claims, which in turn would mean it would be necessary for them to charge higher premiums. Excesses lower the insurer’s administrative costs since customers won’t claim for every small scratch or ding to their car. This is important for traditional insurers, who need to run large back-office teams and infrastructure to handle claims. They give customers a financial incentive to take care of their vehicle, since they will also need to pay towards repairs if they’re involved in an accident. They discourage people from making multiple claims that could reflect badly on their claims history. Why should you look out for in the fine print about excess payments? Often, signing up for lower monthly premiums for car insurance will mean that you will need to pay a higher excess in the event you need to claim. Most insurers are transparent about the basic excess, which may be up to 10% of the value of the damage to your car in an accident or of the total value of the car if it is stolen or written off. However, many insurers also impose extra excesses if any of the following are true:

What happens if you were not at fault in an accident? In theory, your insurer should aim to recover your excess from the driver at fault or his/her insurer and refund the money to you. In practice, 70% of cars are uninsured in South Africa, many of the drivers are unable to pay the damages, and the amounts are so small that it’s not worth pursuing legal action to recover the money. That means there’s a good chance you’ll still pay the excess when the accident is not your fault. So how do I find the policy that meets my needs? You should consider the following factors in your decision:

To get assistance with claims please contact Edmond in our Short-Term Department email shortterm@daberistic.com, tel (011)658 -1333 Source: Personal Finance  Most businesses ask themselves if they should have social media liability and the answer is most probably a yes. Fact is, most small and medium size businesses are using social media in one form or another to promote and advertise themselves. This, of course, brings great reward to those who embrace the digital age.

What this age unfortunately also brings with it, is a new type of risk of which most of us are not quite familiar with yet. We are hearing about it on the news and reading it on, yes you guessed it, social media itself. How many of us has first-hand experience of this relatively new type of risk to businesses and business owners? My guess would be not many of us. Businesses and business owners will know very well that if a new type of risk raises its head and pose a threat, the best way to go about it is to take a pro-active type of approach, rather than a reactive approach. Let’s start by looking at the different types of risks associated with having a presence on social networks:

Discovery Business Insurance is launching 1st of June 2018 and they will be offering Social Media Cover as an extension under their Public Liability policy. This extension will offer cover for any liability as a result of social media interactions and it will also include:

If you would like to get a quote for Social Liability quote, please contact Jan in our Short-Term department, email shortterm@daberistic.com , tel (011)658-1333 Source: Jan Prinsloo (Daberistic Short-Term Broker)  National Treasury announced an increase in Value Added Tax (VAT) from 14% to 15% effective 1 April 2018. Your short-term insurance premium is subject to VAT and will be adjusted. The new premium will be communicated to before your April debit order collection and below is some of FAQ:

General

Premium collection

Policy Amendments

For any queries regarding changes to your insurance, please contact Jan or Po-Lin in our Short Term department shortterm@daberistic.com tel no: (011) 658 – 1333 Source: Momentum |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|