|

In partnership with Morningstar: In 2020, the South African Reserve Bank (SARB) dramatically cut the country’s interest rate by 3%, lowering the repo rate to a historic low of 3.5%. The SARB initially started to cut interest rates in response to declining inflation, which was sitting towards the bottom- end of the inflation target band (of between 3% and 6%). In mid-2020, the SARB cut the repo rate even further, in response to the COVID-19 crisis, to provide relief to consumers and businesses and promote economic growth. By cutting the interest rate, the SARB intends to provide a helping hand to the economy, by freeing up more capital for lending (by financial institutions) to households and businesses.

0 Comments

Dear client,

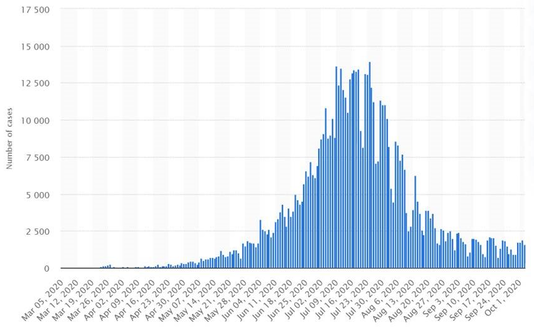

I thought it would be useful to explain the way we think about inflation and your investments as I’m not sure I’ve fully elaborated on this before. So, to start, let’s talk about inflation. Inflation is a relatively simple concept, used to describe the gradual rise in the cost of goods and services. For example, a loaf of bread or the cost of petrol. Inflation is generally healthy if it’s in the 2-3% per year range, but it is considered to be unhealthy if it falls too low or rises too high (the idea is that we make steady progress over time). For this reason, the central bank will adjust interest rates to control it. Inflation is important today because it is currently rising from a very low base, but it’s perhaps rising too quickly. This is understandable, given the reopening of the economy, yet is garnering headlines and has caused some volatility among certain assets. We should also keep in mind that the job of your total portfolio is to increase your purchasing power over time. Some assets we hold will do better in a period of higher inflation and some will do better in a period of lower inflation. The key is to strike the right balance for your long-term goals and risk tolerance, which is a core part of your financial plan. On this, the return on cash (interest) typically fails to keep pace with the rising prices of goods (inflation). Therefore, as a long-term pursuit, cash is actually a very bad investment. Hence, unless we have absolute certainty that the markets are nearing the peak, which is extremely difficult, putting everything in cash is rarely a good idea. We therefore use cash selectively as an investment tool. This is already done within your portfolio, where cash is treated as any other asset class available for allocation. This means that as the attractiveness of other available assets rises relative to cash, cash allocations should fall and vice versa. Therefore, cash plays both offense and defense, by being used as ‘dry powder’ for adding undervalued assets to the portfolio and by buffering against rich valuations. This brings us to a crucial aspect of wealth creation and preservation – we need to be a step ahead of our own emotions as well as other participants emotions. So yes, cash may feel like the best place in the darkest moments (so-called “cash is king”), but it is a poor choice when considered as a long-term pursuit and only tends to work if we increase it before the market decline occurs. At heart, we remain confident that your portfolio is well positioned to navigate different inflation environments. We can’t rule out the odd setback (whether due to inflation, covid, or otherwise), but wealth creation is often about avoiding the biggest mistakes, which is why we’re diversified across different assets. We want to “be greedy when others are fearful and fearful when others are greedy”, but we also want to manage risks along the way. Bringing this together, we want to reiterate that we are aware of the current inflation discussions and your portfolio has been thoughtfully considered in this light. If you would like me to elaborate further on this, or any other matter, I’d be delighted to chat. Regards Kevin Yeh, CFP® South African Market Update South African equities tracked global markets lower during the month, weighed down by poor performance from some large industrial and resource shares, despite strong performance from the local banking sector. Local bonds ended the month largely flat, as appetite for emerging market debt remained subdued, despite the attractive yields on offer. Local listed property continued to face headwinds from uncertainty regarding earnings and distributions, which has deterred investment in the asset class due to the historical reliance on income as a source of return. The rand was stronger against most major developed market currencies for the month, which detracted from the contribution of the performance of global asset classes. South African Economic Update South Africa moved to a level 1 lockdown on 21 September, as daily local Covid-19 infections continued to decline during the month and the recovery rate improved to a figure of around 90%. SA’s Q2 2020 GDP data was released during the month, indicating that GDP fell 17.1% year-on-year for the second quarter, as the hard lockdown took its toll on the local economy. South African Reserve Bank Governor Lesetja Kganyago announced that the Monetary Policy Committee has decided to leave the repo rate unchanged at 3.5%. The decision by the MPC was split, with 2 of the 5 members favouring an interest rate cut. SA headline CPI fell to a year-on-year figure of 3.1% to the end of August (from 3.2% in July), close to the bottom end of the target range of between 3% and 6%. Chart of the month: Daily confirmed Covid-19 cases continued to fall in South Africa during the month as the country moved to a level 1 lockdown. (Source: Statista)  See below for a summary of the key market movements for the month of September:

Please click on the links below to download the Market Summary PDF and the Market Commentary PDF, intended to be ‘end investor friendly’ Morningstar Market Commentary SA September 2020.pdf 2020_09_Morningstar Market Summary.pdf *All data is sourced from Morningstar Direct as at 30/09/2020. The performance of South African asset classes is quoted in rands and the performance of global asset classes is quoted in US dollars.  Global equity markets ended September lower, as concerns over a second wave of Covid-19 infections across Europe and the possibility of a recurrence of infections in the US winter weighed on sentiment.

US politics took centre stage during the month, ahead of what is likely to be hotly contested US Presidential Election in November. The first presidential debate between US President Donald Trump and Democratic nominee Joe Biden, was marred by President Trump refusing to declare that he will accept the election result if he loses. The US Federal Reserve left interest rates unchanged at its meeting midway through the month, indicating that they expect interest rates to remain close to zero through 2023, further reinforcing an increased tolerance for inflation in the medium term. Source: Morningstar  By Global investment strategist at Ninety One, Michael Power

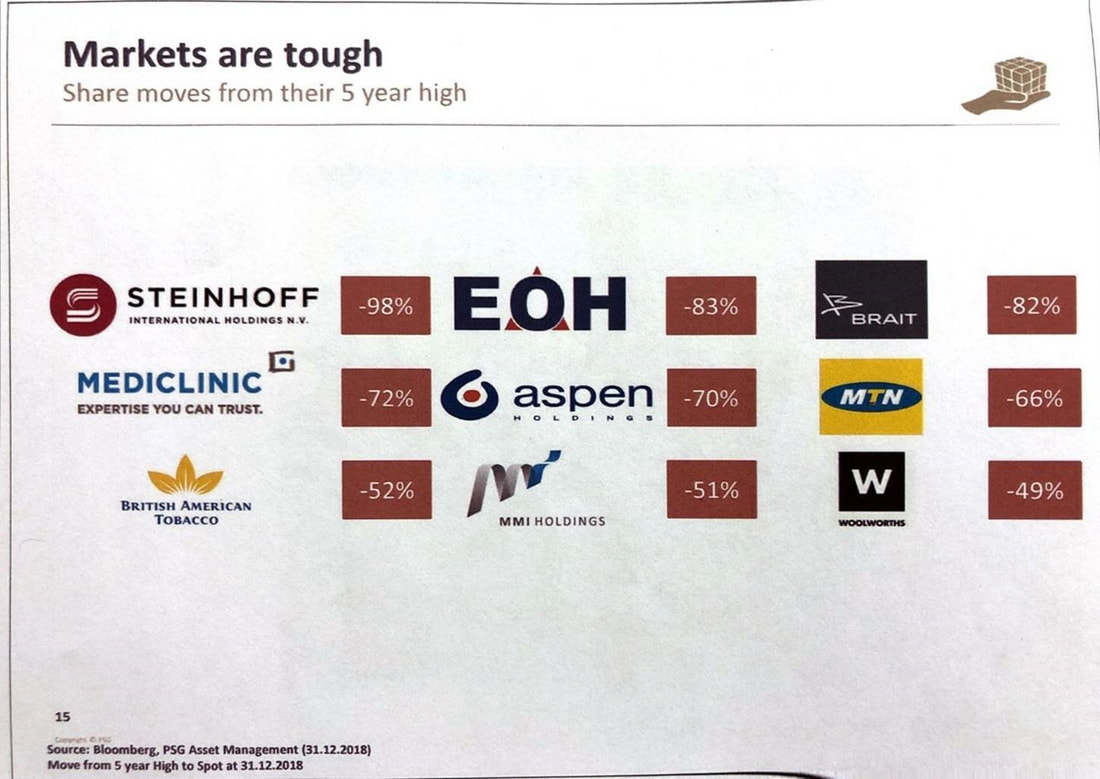

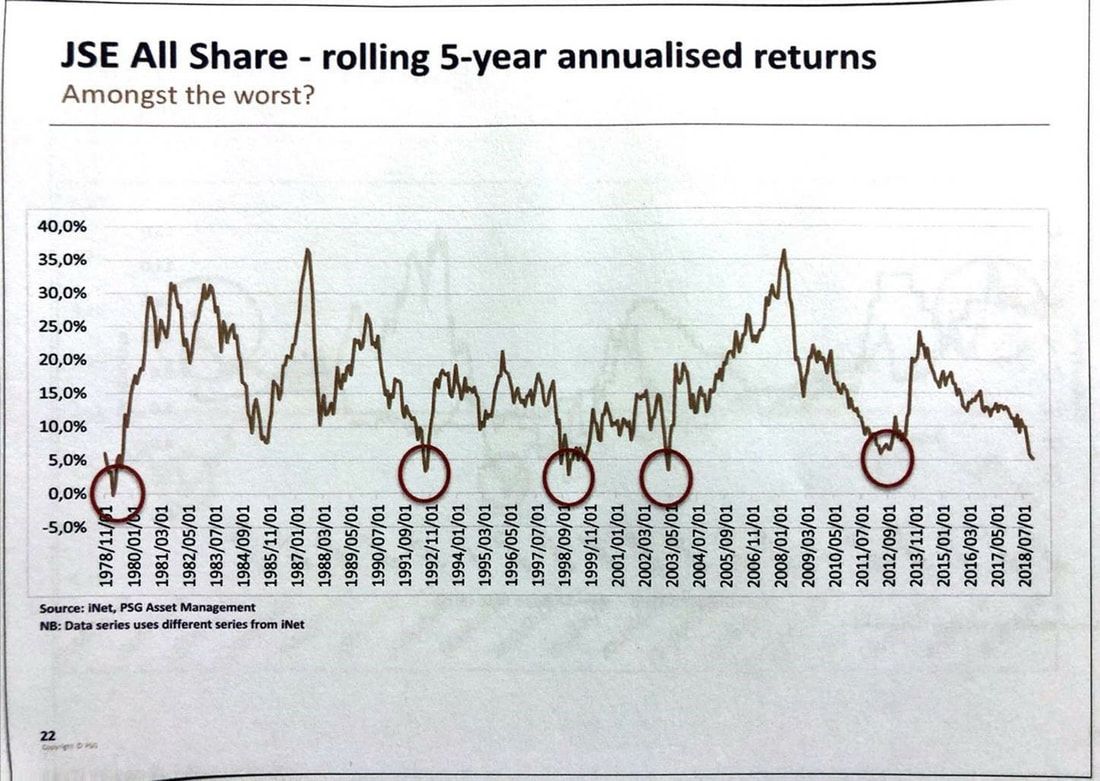

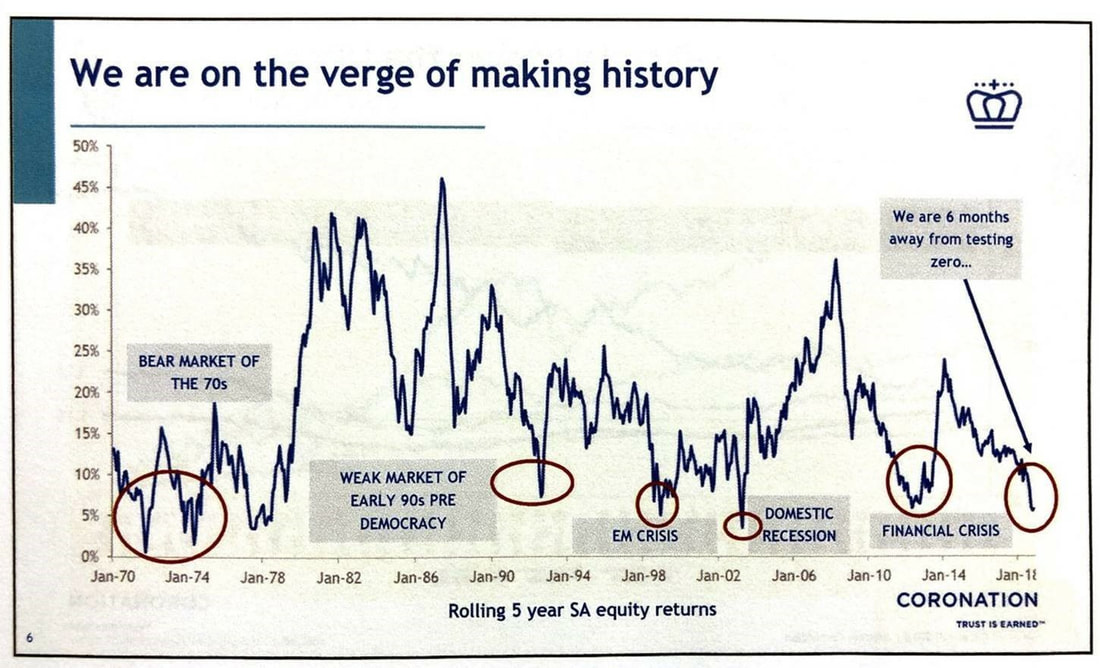

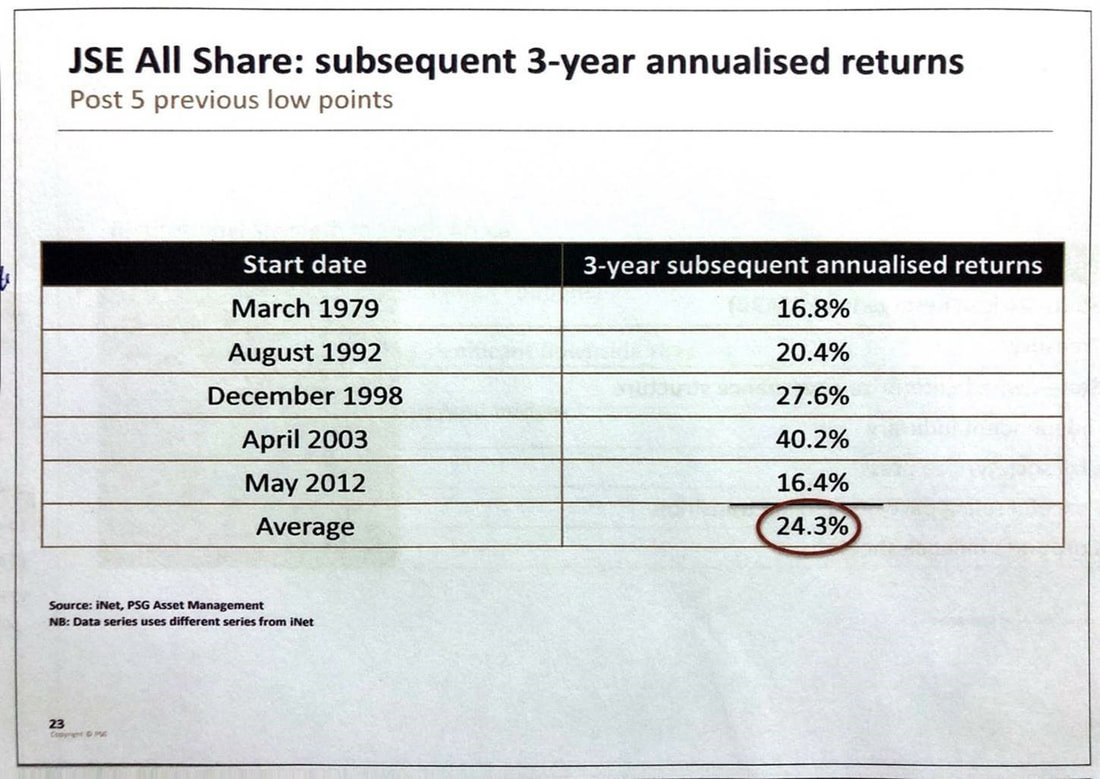

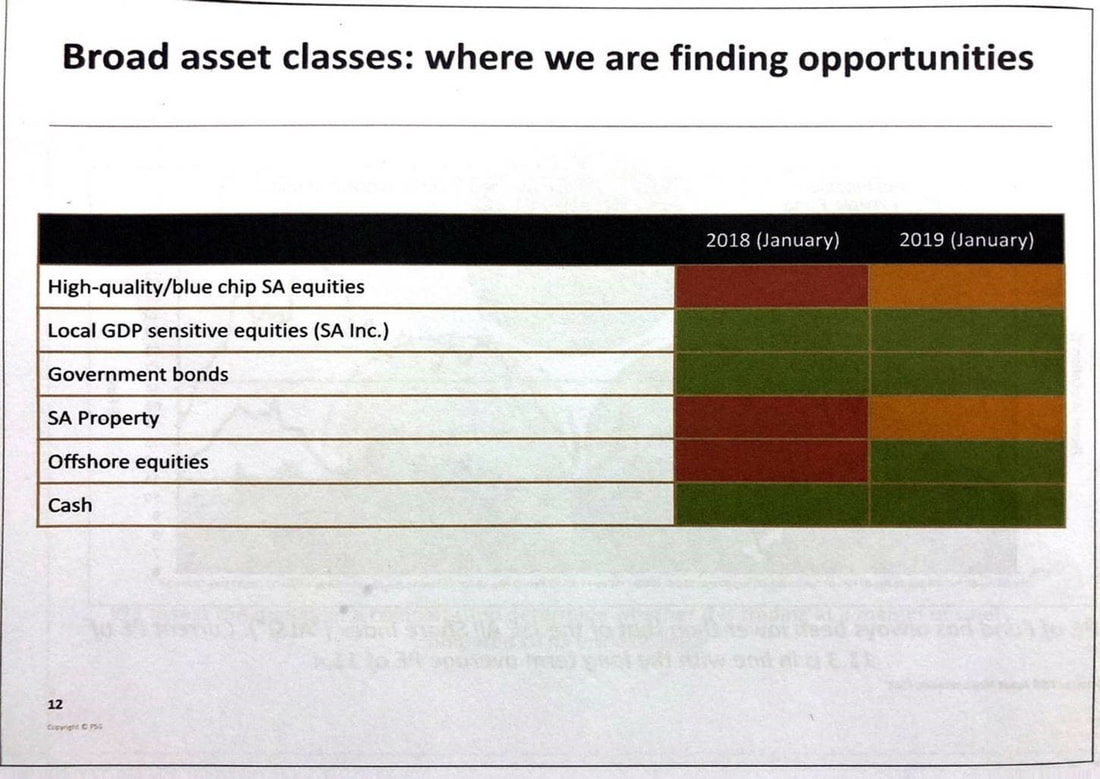

In a recent column in the Financial Times, historian Yuval Harari made the observation that emergencies ‘fast-forward historical processes’. The Covid-19 pandemic, he said, is doing exactly this. Rapid changes are taking place across all aspects of society. Countries, economies and people have been so disrupted that nothing is constant. ‘I think there is no normal any longer,’ said Michael Power, global investment strategist at Ninety One. ‘We are in such a fluid environment that there is nothing very much we can take for granted any more.’ Perhaps what is most profound about this, is how time frames are being condensed. ‘I’m not sure what long term is any longer,’ said Power. ‘Things that I thought were going to happen for instance by 2030 I think in many instances are going to happen by 2025, and even before. There is a concertinaing of many things at the moment, and the reality is that “long term” is something that is affecting portfolios now. ‘There are huge changes taking place across vast areas of business, politics and geography, and we have to get to grips with that.’ This is an acute challenge for asset allocators. They need to be extremely cognisant of their future allocations, because the future may be closer than they realise. Power emphasised two major trends that should be shaping decision-making. The first is that the shift of economic power to the east may now happen more quickly than previously thought; and the second is that the eurozone, and potentially the European Union itself, are increasingly fragile. Chinese wealth ‘We are fast-forwarding this process by which the west is going to see the centre of gravity move to the east,’ said Power. ‘I think that is going to happen in the next five years rather than the next 10. My prediction is that by 2023 China will be a larger economy in absolute terms than the US.’ This shift has been sped up by the massive economic impacts of the coronavirus. While every country has been affected, China is likely to revive itself more quickly for a significant reason. ‘What’s driving the admittedly muted recovery in China is the Chinese consumer,’ said Power. Consumers in the west will struggle to support the recovery of their own economies to the same extent. And this disparity is going to grow more pronounced. ‘What is going to happen in the next five years is that China is going to discover its 1.4 billion consumers, and they are going to become the drivers of the Chinese economy,’ said Power. This will happen at the same time that China is starting to match, and in many cases lead, the development of global technologies. ‘We’ve seen it start to happen with Huawei in cell phones, and it’s probably going to happen in things like aircraft,’ said Power. ‘The Chinese are going to start to move up the technology chain.’ Asset allocators need to consider what this means for their portfolios, particularly because this transition won’t be smooth. ‘In this process of change, there will be capital that will start to leave the west and move to the east, but it will do so quite hesitantly,’ said Power. ‘Some of it will go to a stepping stone between these two worlds, and that stepping stone looks like gold. ‘I think we have to watch this trend,’ he said. ‘Start understanding the opportunities to invest your capital beyond the old world, because the new world is going to come into focus much more quickly.’ European cracks The second major disruption that may be accelerated by the Covid-19 crisis is a serious challenge to the sustainability of the eurozone. ‘In the next five years I think the euro is in danger and possible the European Union itself,’ said Power. ‘That threat is going to come from the south.’ The southern European states are falling further behind their northern peers in economic terms and are increasingly reliant on financial support to sustain their viability within the European Union. Their vulnerability may become even more starkly apparent in just the next few months of summer. ‘Southern Europe earns well over 50% of its GDP from the tourism season,’ said Power. ‘It’s like having a single crop, and their crop is going to fail this year. They are going to get no income from tourism. ‘That is going to cause huge problems, not only for Italy, but Spain, and Greece and Portugal. Many of the issues that are facing the European Union are going to become very front-and-centre in the next four months.’ This may well lead to another country deciding to split away from the Union. ‘In the next five years its distinctly possible that we will see a second exit from the European Union, and that is probably going to be Italy,’ said Power. ‘Even before this, there were cracks evident, but those cracks are now gaping chasms.’ Source: Ninety One Summary The US-China trade war that began more than a year ago has been hurting the economy and trade of the two largest economies of the world, while also disrupting and re-shuffling the global supply chain. In addition, the United States hiked interest rates four times last year, increasing the rate to 2.25%, attracting funds back to the United States, first hitting emerging markets, and then hitting the US stock market. The US stock market had the second worst rate of return in December in the past 100 years (-7.8%). The South African asset management companies that I rate highly agree that the South African stock market and global emerging markets are at or near historical lows, and many good investment opportunities are found at this stage. We recommended long-term investors to continue to have exposure to growth (stock) assets, which could provide a 60% return over the next three years. *** Global The US-China trade war has been more than a year since the US declared it last year. President Trump of the United States believes that China was competing unfairly. The US trade deficit with China is huge and continues to expand. China infringes on intellectual property rights, as well as providing subsidies to public and private companies. Sanctions include imposing 10% tariffs on imported products from China, lawsuits and measures against ZTE, Huawei and other Chinese telecommunications companies, and containing Chinese companies in the 5G sector. From the recent statistics on Chinese economic growth and import and export volume, China’s exports in February fell by 20.7% from the previous year to US$135 billion, the largest decline since February 2016, indicating that the US-China trade war is having a significant negative impact on China. China's stock market fell 25% in 2018, but since the start of 2019, China's stock market has risen by 25% due to the recovery of global investor confidence and the Chinese government's monetary easing. In 2018, the US stock market was steadily rising, until it experienced a sharp 7.8% drop in December and a 6.1% decline over the year, the first annual negative rate of return since the 2008 global financial crisis. However, it has risen 11.48% since the beginning of this year. South Africa After Cyril Ramaphosa was sworn in as new president at the beginning of last year, there were high expectations from all sectors, which was termed Ramaphoria. However, the US-China trade war, the emerging market currency crisis, the ANC party’s two-faction fighting have caused the high spirits to evaporate quickly. The successive commissions of inquiry have opened up the lid on the rampant corruption and briberies during the Zuma era, so now we know that the National Treasury was hollowed out, and the infrastructure is crumbling. Eskom frequently broadcasts news of mismanagement, energy crisis and implements load shedding, which darkens investor confidence. South Africa’s economic growth rate last year is only 0.8%, and this year is not going to be any better due to the Eskom factor. South Africa's stock market fell 8.5% in 2018, the first annual negative rate of return since the 2008 global financial crisis. If former President Zuma sees the stock market return history, he will brag that, during his presidency, the stock market has risen every year and has never fallen! This is a bit ironic. South Africa's stock market has risen 6.3% since the beginning of this year. The four South African fund managers I rank most highly, based on my long-term observation, analysis and evaluation, agree that 2018 was a tough year for all investors: they lost money no matter where they put their money (except bank deposits and bonds). PSG pointed out that 2018 was a year of trying to avoid landmines:  In 2018, the following well-known listed companies have brought huge losses to investors.  The South African stock market is now near the bottom of the five troughs experienced over the past 40 years.  Coincidentally, Coronation also has the same analysis:  However, they also agreed that 2019 is a year of turnaround. The PSG research report pointed out that the annualized rate of return for the three years after the past five lows was as high as 24.3%, that is, the cumulative rate of return for three years was 92%. Even using the lowest annualized return rate of 16.4%, the investor's 3-year cumulative return would reached nearly 60%. This is the so-called reversion to the mean. Even if the South African economy does not do much, by going from the bottom of a market cycle to the average of a market cycle, with a little boost of investor confidence, the investors could receive this kind of return.  PSG Asset Management is currently positive on the following asset classes (marked by green): South African domestically focused stocks, government bonds, overseas stocks and cash.  Even though 2018 was a disappointing year for investment returns, we recommend investors not to give up on the stock market; continue to hold stock positions in the medium and long term, with exposure to South Africa and offshore markets. Allocate positions in shares, bonds and cash. During this trying time, I chose this pearl of wisdom from Warren Buffett to remind myself and investors:

Now is not the time to give up; it is probably the best investment opportunity since the 2008 global financial crisis.  Kevin Yeh's Corner

I am delighted to write to you in 2019. I trust that you and your family had a restful, festive year-end holiday. With everyone back at work and kids back at school, these holiday memories fade quickly into the background! There are some significant events taking place in 2019: - National elections, around end of April - 30 May to 14 July: Cricket World Cup in England and Wales - 20 Sep to 2 Nov: Rugby World Cup in Japan (Go Ama Bokke!) Not forgetting the SONA (State of the Nation) address early February, followed by the ever-important budget speech late February. Globally, the US-China trade war still hangs over the global economy. The Chinese economy is slowing to a growth rate of 6.6% in 2018 - the slowest pace in 28 years. The Chinese central bank is pumping liquidity into that economy. The US Federal Government shutdown enters 33rd day with no end in sight, as President Trump wants money for his border wall with Mexico. The Emerging Markets had a torrid time last year, reminiscent of the 2014 - 2015 crisis. The IMF projects the global economy to grow at 3.5% in 2019, slower than the 3.7% in 2018. The Zondo commission of inquiry into state capture has lifted the lid on corruption, money laundering and fraud. We now know how the officials in power have colluded and stolen from the state coffers, and why the South African economy has been a shambles. Turning to the financial markets, 2018 was a forgettable year for most investors. The JSE CAPI went down by 7.7%, the balanced fund sector had a negative return of 4.2%. The World Developed Markets returned -10.6%. Emerging Markets even worse -17.5%. China fared the worst at -25%. The only bright spot was bonds (7.7%) and cash 7.2%. Looking ahead, after the doldrums of 2018, 2019 should give investors better returns, as many asset classes are already at depressed levels. Investors should be patient and stay invested. Let us work together to fight corruption, improve our businesses and institutions, do what we can, to make South Africa a better place for all. And let's pray for our beloved country for a peaceful election, that people of ability and good character are in power to do good for the country. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|