Benefits can become complicated. For your own good, here’s what you should know.

Medical schemes undertake liability in return for a premium or contribution. They are required to help their members in obtaining healthcare services and defraying expenditure for such services. The benefits that a scheme may grant must be registered in its rules. Schemes typically cover the following healthcare services:

Common tariff structures

Private health insurance allows people to protect themselves from the potentially extreme costs of medical care if they become ill. It also gives people access to healthcare when they need it. The exclusion list of scheme options (Annexure C of scheme rules) deals with limitations of entitlements. Schemes must ensure that there is good reason for these exclusions and limitations, and that they are not too broadly worded. Otherwise, they may lead to arbitrary or unreasonable denial of care. But why exclusions and limitations? Entitlements in any option are discretionary (optional) or non-discretionary (compulsory). The latter are covered by the prescribed minimum benefits (PMBs). The Regulations in the Medical Schemes Act 131 of 1998 deal with the entitlement to PMBs: they must be paid in full under certain circumstances, such as when the member obtained the service from a designated service provider. The standard of care (and entitlement to it) is determined by protocols based on the principles of evidence-based medicine or, where these do not exist, the protocols of the public sector. Non-PMB conditions and entitlements are dealt with in scheme rules, and limitations and exclusions are applicable to them. Exclusions The following principles should be considered when deciding whether an exclusion is justified or not: best practice, evidence-based healthcare, clinical protocol, cost-effectiveness (affordability), and the laws of the country.Conditions or circumstances that should definitely not be excluded are those that are medically necessary, with little discretion from the member and/or service provider. Put differently, consider whether urgent treatment is needed to prevent death or permanent disability, and whether the attending doctor has some discretion as to the timing of treatment, and whether the treatment should be given at all. It would, for example, be entirely inappropriate to include an exclusion for the treatment of acute appendicitis, whereas an exclusion for cosmetic surgery in the absence of clinical indications would be appropriate. Not forgetting affordability, clinical protocols based on evidence-based medicine should be the bottom line when deciding whether funding is justified or not. Fair exclusion? You decide. Limitations on cover are appropriate where they permit a degree of financial risk management. But they are inappropriate where their application allows for the selective targeting of specific people or vulnerable risk groups. Thus, reasonable financial management should be permitted, but not to the extent that it allows risk selection and unfair discrimination. Limitations should be permitted where they achieve the following:

Limitations are inappropriate where they achieve the following:

Source: Medicalaide.co.za

0 Comments

Avoid close contact. Don’t go to your doctor’s rooms. So what are your options? Globally, people have been slow to take up consulting doctor using digital and social platforms. But, with COVID-19 now in 100s of countries, the number of people spending time with doctors through screens is increasing just as fast.

The number of COVID-19 infections have exceeded 100 000 and are increasing daily. So are the number of people using telemedicine technology. With good reason. Using your computer or smartphone to see a medical professional is not new. Virtual consultations and treatment have been available in most healthcare systems and through medical schemes, including Discovery Health Medical Scheme, for some years. But, given the traditional preference for face-to-face consultations between doctor and patient, virtual consultations and remote care were mainly for the future, for tech-savvy generations. This view is changing fast as the world responds to COVID-19. Dr Peter Antall, the chief medical officer for AmWell, was quoted saying “telehealth is being rediscovered” as health systems are racing to adapt and even develop virtual services that can serve as their front line for patients. (Doctors and patients turn to telemedicine in the coronavirus outbreak). Virtual care is the first line of defence Technology-based consultations and remote contact with patients through virtual platforms are fast becoming the norm. As people connect virtually, healthcare professionals manage overcrowding of consultation rooms, ensure appropriate referral for care, and help prevent the highly infectious COVID-19 virus from spreading. More importantly, virtual care keeps the worried calm, and those who need immediate care are prioritised. “In South Africa, we’re raising awareness and taking appropriate precautions to help to minimise the spread of COVID-19. We must continue to do everything possible to minimise the chance of uncontrolled spread. Applying learnings from around the world in managing COVID-19, show access to and using telemedicine and virtual consultations are of critical importance. It has been an effective healthcare tool to ensure appropriate care while making sure infection rates are controlled by avoiding direct contact with others,” says Dr Noluthando Nematswerani, Discovery Health’s Head of the Centre for Clinical Excellence. The power of social distancing, part of which is offering virtual healthcare, has been invaluable in the success of China (fewer than 50 infections a day) and South Korea (from 900 infections a day to fewer than 200) in containing COVID-19. Promoting virtual consultations prevents medical facilities from becoming overcrowded with people, possibly spreading infection to others. Doctors from around the world agree with this approach and are praising telemedicine technology for helping to successfully manage COVID-19. Virtual consultations through DrConnect: reaching more people virtually Since 2017 Discovery Health Medical Scheme has had a virtual consultation platform called DrConnect. This digital platform, supported by artificial intelligence (AI) machine learning, gives members of the Scheme access to virtual consultations with healthcare providers they have visited in the past 12 months. Through the Discovery app, this platform also offers free trusted medical information from a worldwide network of doctors. “It’s natural that people may be concerned and would want to see a medical professional. Your first choice when any signs or symptoms of COVID-19 are present, should be to stay away from others. Contact your doctor, either telephonically or through virtual consultation channel, like DrConnect (that’s available through Discovery Health Medical Scheme). Accessing virtual consultations, especially now as a measure to contain COVID-19, ensures that people receive the correct care and that we protect the health of others,” says Dr Nematswerani. In response to COVID-19 infections in South Africa, Discovery Health Medical Scheme has a benefit to support the diagnosis and treatment of the illness. Going forward, Discovery Health is looking at opening a basic version of DrConnect to a broader segment of healthcare professionals and people. Commenting on this, Dr Nematswerani says, “With more people having access to and using virtual consultations, we can employ this as another method to contain the spread as well as minimise the accompanying health and other environmental effects of COVID-19.” Telehealth platforms are helping experts and medical professionals around the world to map cases and to distribute messages of prevention and appropriate care. Through effective prevention and encouraging virtual care, we can contain COVID-19. Source: Discovery Health  Much debate has taken place around the proposed National Health Insurance Bill (NHI). Discovery’s overall position on NHI is unequivocal. We would like to provide some additional information to answer any questions you may have.

Discovery Health is supportive of structural change that assists in strengthening and improving the healthcare system for all South Africans, and we are committed to assisting where we can in building it, and making it workable and sustainable, seeking to ultimately strengthen both the public and private healthcare systems for all South Africans. While the NHI is a huge, complex and multi-decade initiative and a considerable amount of debate and effort will be required to make it workable, in this brief note, we review some of the key issues arising from the NHI Bill and then look at the NHI policy process going forward. The role of medical schemes once the NHI is implemented A central issue is the future role of private healthcare and medical schemes once the NHI is implemented. The NHI Bill states that when the NHI is ‘fully implemented”, medical schemes will not be able to provide cover for services that are paid for by the NHI. Discovery's strong view is that limiting the role of medical schemes would be counterproductive to the NHI because there are simply insufficient resources to meet the needs of all South Africans. Limiting people from purchasing the medical scheme coverage they seek will seriously curtail the healthcare they expect and demand. It poses the risks of eroding sentiment, and of denuding the country of critically needed skills, and is impacting negatively on local and international investor sentiment and business confidence. Crucially, by preventing those who can afford it from using their medical scheme cover, and forcing them into the NHI system, this approach will also have the effect of increasing the burden on the NHI and will drain the very resources that must be used for people in most need. Discovery also believe that limiting the rights of citizens to purchase additional health insurance, after they have contributed to the NHI, would be globally unprecedented and inappropriate. In virtually every other country with some form of NHI, citizens are free to purchase additional private health insurance cover, including cover that overlaps with services covered by the national system. A restriction on choice of medical scheme cover is not dissimilar to limiting the rights of citizens to purchase private education for their children or private security, on the basis that the public system already provides state schooling and security services. Given the substantial harms that this approach of limiting the role of medical schemes will cause, it must surely be strongly justified for good policy reasons. However, we are not aware of any sound policy reason or justification that has been put forward for this approach. Discovery believe that medical schemes will continue to cover all of the healthcare services which they currently cover for the foreseeable future for a number of reasons:

Discovery is already actively engaging with the Department of Health on this critical set of issues, alongside the broader business community, and we will continue to do so in order to ensure that medical schemes and private healthcare remains a critical part of the healthcare system, together with the NHI. The financing of the NHI system The Bill makes no reference to the likely costs of the NHI once fully implemented. Any fundamental change that improves quality and access and seeks to contract with private providers will require substantial additional funding. We understand that National Treasury will soon be publishing a costing document, and that this is likely to be based on an incremental approach to providing NHI benefits. The Bill specifies that payroll taxes and a surcharge on personal income tax could be considered as sources. Such taxes would need to be determined by National Treasury. At the presentation of the Bill, the Minister of Health indicated that no tax changes are envisaged over the 3 year period of the current Medium Term Expenditure Framework. In our view, there are material challenges to raising new revenues to supplement the current government budget for healthcare, and this is unlikely to change in the foreseeable future. This suggests that the rollout of the NHI will be slow unless there is a substantial improvement in the country’s economic prospects. The role of private hospitals and health professionals The Bill envisages that the NHI Fund will contract on a voluntary basis with private hospitals and health professionals to supplement the current public sector delivery system. For the foreseeable future, we expect that the NHI will contract with some GPs to supplement primary care services, and also that it will contract for certain high priority services to address specific gaps in public sector provision. If this is achieved, it will already be a significant step forward. Beyond that, we expect that the vast majority of NHI services will continue to be delivered by public sector clinics and hospitals, and that private hospitals, specialists and other providers will continue to be funded by medical schemes. South Africa is blessed with a committed, highly skilled and world-class healthcare professional community. These professionals work hard, provide excellent care and are committed to our country. We will work hard to defend their rights to fair remuneration, to an optimal working environment that promotes sustainability and ideal patient care, and to retaining and supporting them within our broader healthcare system. The NHI Bill Process The NHI Bill has been tabled in Parliament and is now in the hands of the Portfolio Committee on Health, which will hold formal hearings in early 2020. Discovery is actively participating in a direct engagement process between Business Unity South Africa and the Department of Health to discuss a number of issues of common interest, including the NHI. There is also a parallel process within NEDLAC, offers further opportunities for business, labour and government to engage on the final content of the Bill. We expect the Bill to be finalized sometime during 2020 at the earliest. Concluding remarks While the NHI Bill certainly raises some serious concerns, we recognize the need for structural change to improve healthcare for all in SA. We believe this should leverage the strengths of the key elements of the current public and private healthcare systems, and we remain confident that the final outcome will be rational and workable. Discovery is committed to playing its role in building a positive future - for our members, South Africa’s healthcare professionals, and for all South Africans. Frequently asked questions  1.Claiming from Medical Aid

Daily Claims The day to day claims, like your Gp, Specialist, buying medication will be covered from your MSA Benefit, however if you are using a hospital plan, day to day is not submitted. Hospital claims. This is any claim that has been authorized for hospital stay, this can be a day or more than, so this will be paid from the hospital benefit Documents required to submit claim Valid invoice, not older than 3 months which must include, - Dr Details, Practice number, service date, ICD10 Code and Procedure code - Details of the patient i.e Name, surname and date of birth, Medical aid number Where to submit Medical Aid claim

2.Claiming From Sirago Any claims that needs to be submitted to Sirago has to submitted to your medical aid before claiming from the Gap Cover. Gap cover will only pay if it’s a valid claim which is based on one of the following:

Documents required to submit claim -Complete claim form -Invoices -Hospital statement -Medical aid statement, reflecting all the invoice or providers that has shortfall Where to submit

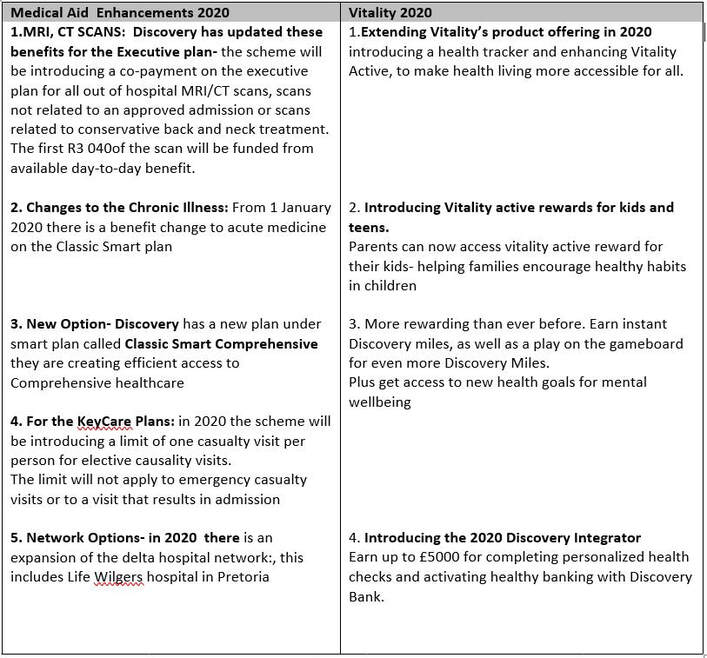

Click here to read more on Medical Aid enhancements

Please contact Namhla or Tammy in our Health and Wellness Department, email health@daberistic.com, if you have any queries about Discovery Health Source: Discovery  Medical aid is a necessary yet expensive purchase in South Africa. Due to the public healthcare system unable to cope with the public demand, people who can afford it or who work for larger employers will choose private healthcare. They buy medical scheme products to cover such healthcare expenses.

Since medical aid is expensive, it is important for a member to understand its benefits, in order to make the best use of it when needed. As each new year begins medical aid members start with a clean slate, with new benefits and replenished savings available. If you manage your medical expenses correctly you can avoid out-of-pocket expenses and limit the possibility of running out of benefits. 1. Read up on your medical aid plan Take the responsibility of understanding your medical aid plan. Visit the medical scheme's website, find your specific medical aid plan information and read through it. Check out the FAQs. If your medical scheme creates YouTube videos on your specific plan and benefits, watch these videos. The more you understand your medical aid plan, the better you are in a position of making use of benefits provided for by the plan. 2. Speak to your Healthcare Advisor Medical aid plans are complex. A medical aid plan has many details, terms and conditions. Many members will struggle to make sense of it. A Healthcare Advisor with suitable qualification, training and years of experience can simplify matters for you and answer your specific questions. 3. Find a GP on your medical aid's network Using network doctors is an invaluable tool to make your medical aid last longer as it means you won’t be charged more than a specific amount. 4. Always use partner networks Medical schemes negotiate preferential rates with providers who have partnered with them. This means if you use a network hospital, doctor or pharmacy you will not be charged more than the rate agreed with the scheme. This will also help you to avoid co-payments, deductibles and additional out-of-pocket expenses. 5. Ask your pharmacist Buy over-the-counter medicine to treat less serious ailments and consider using generic medicine which is cheaper but effective. Pharmacists are able to provide sound medical advice on problems such as rashes, colds or illnesses that are not severe, simply ask! 6. Going to hospital - get the facts Talk to your doctor or specialist before being admitted to hospital. Check what they are going to be charging and what your scheme will cover. If there is a large difference, don’t be afraid to approach your doctor to see if they are prepared to adjust their fee. Alternatively, you can also check if there are other healthcare providers who are on your scheme’s network that will charge you a better rate. 7. Remember to pre-authorise Pre-authorisation is required for all hospital admissions to ensure your stay will be covered. Always ask if there are any co-payments or sub-limits that will apply and what you can do to avoid these. For planned procedures, it’s also worth checking with your scheme if you will obtain better cover by using contracted providers or having the procedure performed in the doctor’s rooms or a day clinic. 8. ICD-10 codes If you need to undergo an operation, ask your surgeon for the codes that will be charged. This will include the procedure codes and those for any other products that will be needed, this all helps with pre-authorisation and ensuring the costs will be covered. 9. Chronic health conditions Some schemes offer programmes to help you manage severe chronic conditions such as cancer, diabetes and HIV/AIDS. These programmes are usually covered from the risk portion of your medical contribution and are not funded from your savings account. They help you use your benefits to maximum advantage while ensuring you receive quality care by using specific providers. With thanks to: www.w24.co.za  People often believe that if you gather significant assets during your lifetime and put enough into your retirement or pension fund during your career, you don't have to worry about living comfortably in your later years. But in an environment where medical costs are rising and markets are constantly fluctuating, is that really true? Here's a figure that might be surprising if you are planning to retire soon and haven't considered your health care costs. If you are 65 and retiring this year, you will need about R990 000 during retirement to keep up the same cover you currently enjoy. For a couple, that total is about R1 990 000. (assuming you are on the Discovery Health Medical Scheme, on the Classic Delta Comprehensive Plan, a contribution of R4059 to your plan, and that your retirement grows in line with medical inflation- currently CPI +4%). These numbers are based on the assumption that a man will live to be 85 and a woman 87, however with publications like the scientific research journal Nature reporting that children born in 2000 will live to be 100 years or older we may need even more retirement and medical savings in the future. With our longer life spans, financial planning for retirement has never been more important if we want to maintain your lifestyle over the long term. So how much is enough? It’s easy to miscalculate how much you’ll need in retirement. Underestimate what you will need and retire too soon and you could run out of money in your retirement years. Overestimate and you might keep working longer than is necessary or deprive yourself of trips, restaurant meals and other luxuries unnecessarily. Bottom Line Personal asked retirement-planning professor, Michael Finke, what he sees as the top 3 most common mistakes made by people when planning for retirement. Number one, he says is that people often overestimate the amount medical aid and insurance will cover, number two, that they underestimate health-care inflation and the third mistake that they do not consider or factor in the possibility that they could need long-term care in retirement. On how to more accurately estimate medical expenses in retirement Finke suggested that you start with what you currently spend on health care annually, or if that figure has fluctuated greatly, take the average you have spent over the past five years. Then also factor in that the Consumer Price Inflation (CPI) in South Africa has increased by 6.3% a year on average since 2008, and medical scheme contributions are increasing by at least CPI 3-5% annually. What can we do to plan better for the future? It is important to engage in a healthy lifestyle. 60% of diseases afflicting people worldwide are lifestyle diseases. To help aid in a happy, active retirement, protect your health by embarking on regular exercise, a balanced diet and maintaining a weight that is correct for your body type. The healthier you keep your body; the better the chances are that you would not need to spend as much money on healthcare bills as you age. Of course, there are will always be unforeseen illnesses which will catch you off guard but it is important to make provisions where you can, so that medical bills will be one less thing that you would need to worry about as you enter into retirement. Invest in yourself and pick the right plan Government care may be sufficient for many pensioners; however, many may require immediate or specialised levels of care that are not readily available at state facilities. Some medical schemes may also impose substantial late joiner penalties, waiting periods and exclusion if a pensioner joins for the first time. Having adequate retirement funds to cover medical cost will ensure you get the care and treatment you need when you need it. Covering your medical expenses in retirement requires planning and Discovery Invest has created funds that help you fund your healthcare expenses in retirement. They also give you up to 15% more money for your retirement savings. To get us to review so as to ensure sufficient retirement savings, please contact Kevin or Thato, email: invest@daberistic.com tel no: (011 658-1333) Source: Finance24 |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|