All Medical aid Options would include: Accidental or emergency medical hospitalisation, maternity benefits, chronic illness benefits, oncology benefits, mammogram screening (once every 2 years), pap smear screening (once every 3 years), and prostate cancer screening (once a year). Below we detail each cover and how it works.

Hospitalisation Whether your medical aid option is a hospital plan or a savers plan, as long as you are hospitalized in South Africa and obtain the hospitalization pre-authorization, you are covered. In case of emergency hospitalization, the hospital will contact the Medical aid company directly and obtain authorization When hospitalized, the hospital bill and the doctors’ bills are separate. In the case of elective hospitalization (planned procedure), the Medical Aid company will pay the hospital bill in full (in most of the cases). In terms of doctor's fees, medical aid company will pay according to the scheme rate. For example, if the scheme rate for a certain operation is R5,000, but the doctor can decide how much to charge. If the doctor charges R15,000, the Medical Aid company will only pay R5,000, and the remaining R10,000 is your liability. If you have Gap Cover, the the co-payment can be claimed back. If the patient is hospitalized due to an accident, an emergency or critical illness (such as cerebral hemorrhage), the doctor does not charge more than scheme rate, and the Medical Aid company will pay for the medical cost, and this is unlimited. In addition to applying for pre-authorization for hospitalization, you can also apply for pre-authorization with the Medical Aid company if you need to do endoscopy (as out-of-hospital) so that the Medical Aid company will settle the medical expenses. It should be noted that if your endoscopy is done in a hospital or a day hospital, you will need to pay a co-payment; If it is done in the doctor's room, there won’t be a co-payment. What should you do if the doctor asks you to request for pre-authorization? You need to ask the doctor for the following information and provide it to the Medical Aid company: • Medical aid membership number • Name the patient • Reasons for hospitalization or surgical items • Date and time of admission • Name and practice number of doctor • Hospital name and practice number • ICD10 codes and procedure codes Maternity Benefit If you have confirmed your pregnancy with your doctor, you can activate the maternity benefits with the Medical Aid company. After that, your medical aid would compensate 8 maternity check-ups up to scheme rate (about R480). Each obstetrician and gynecologists' charges different fees, you will then need to pay the amount exceeding the scheme rate. If your Gap Cover is with Sirago Ultimate option, 4 out of the 8 times, you may claim back the difference paid. Chronic Benefit If you are diagnosed with chronic illness, you can ask your medical aid broker for a chronic illness benefit application form, and ask your doctor to fill it out and send it to the Medical Aid company (or send it to the broker, who will send it to the Medical Aid company). In this way, you can go to the pharmacy for medicine every month, and the Medical Aid company will pay for the medicine. Cancer If you are diagnosed with cancer, you need your oncologist to provide a treatment plan and histology report to the Medical Aid company. Once the oncology benefit is activated, the first R200k of each cycle (12 months) will be paid in full, up to scheme rate. After that, Medical Aid company will pay 80%, and the remaining 20% will be your own expense. (if you have Gap Cover, the 20% co-payment amount can be claimed back) If your Gap Cover is Sirago's Ultimate option, the Gap cover will also compensate you R25k. Day-to-day Medical Expenses - Medical Savings If you are on a Savers option (or higher), you can enjoy day-to-day benefits. Every January, Discovery gives you your full-year savings which you may use throughout the year, if the savings are not used up by the end of the year, it gets rolled over to the next year and you can accumulate it and earn interest. If you are on a Priority, Comprehensive, or Executive plan, you also enjoy the Above Threshold Benefits, given that you have paid up the Self Payment Gap. What can you use Medical Savings for? You can use your Medical Savings for any out-of-hospital medical-related expenses, including but not limited to doctors' consultations, over-the-counter medication, dentists, glasses, certain co-payments (scopes, out-of-hospital CT/MRI scans), etc. Once the savings are used up, you will then need to pay for the medical expenses from your own pocket, until January the following year. Written by: Tammy Hua If you would like to review your Medical Aid option contact Tammy email: service@daberistic.com (tel)11)658-1333 Ext 106  The flu season is here again and with this year’s flu season expected to be more severe, South Africans should seriously consider getting their influenza (flu) vaccine, a local disease expert warns. We are here to remind our Medical Aid Members that use this time to get the flu vaccine, to strengthen immunity, and let you enjoy this winter in the healthiest way possible.

Since Covid 19 came into our lives, its very hard distinguish the difference between the two. It is rather important to note that Flu and COVID-19 are very different diseases. Although Flu and COVID-19 may present similar symptoms, the viruses that cause them are not the same. COVID-19 is caused by infection with SARS-CoV-2, and flu is caused by infection with influenza viruses. To gain protection against each, you need to have the vaccine developed against each disease. You don't have to wait between COVID-19 and flu vaccinations. You can have them at the same time and, if you've had COVID-19 and recovered, it's safe to have the flu vaccine. Remember to give the healthcare provider your Medical aid company name and your Medical Aid number. Below we indicate with the different medical aid Providers , you can go about getting the vaccine through your Medical Aid Provider. Discovery Flu shot is paid from savings, or if you are on the Smart Plan, it is paid from your OTC benefit; if you are on the Core Plan, you then will need to pay from your pocket. You may go to: Medirite + Pharmacy (No dispensing and admin fees), ICPA (independent community pharmacy association), Clicks or Dis-chem. Momentum Flu vaccine is paid from Health Platform Benefit, you can either contact Momentum via WhatsApp (+27860117859), Momentum App, access your Momentum profile or call 0860117959 to notify Momentum. Bonitas Bonitas offers all members a free flu vaccine once a year. Simply go to Dis-chem, Clicks, or Pick n Pay Pharmacies. FedHealth FedHealth offers all members a free flu vaccine once a year, you need to pay R36 for admin fee. Fedhealth covers both flu vaccines, namely quadrivalent (QIV) and trivalent (TIV) vaccines. Profmed One flu vaccine per person per year is covered by Profmed Scheme. You must use a Designated Service Provider (DSP). If you want to know more about preventative benefits, please contact Namhla in our Health Department, email service@daberistic.com , Tel (011)658-1333  Every Medical Scheme includes maternity benefits.If you are not already pregnant before applying for your medical aid, you can enjoy maternity benefits when you fall pregnant. This article will focus on Discovery Medical aid company. If your medical insurance is Momentum, Bonitas, Fedhealth or Profmed, please contact us for your maternity benefits. Benefits will be activated when your pregnancy or baby profile is created on the My Pregnancy or My Baby programme on the Discovery app, or on website www.discovery.co.za or when you register your baby onto the Scheme. You can also activate the programmes by calling 0860 99 88 77 and following the voice prompts. These benefits are available per pregnancy per child up to two years after birth. Once these limits are depleted, you will have to pay for out-of-hospital healthcare expenses related to your pregnancy. Benefits Overview During Your Pregnancy  For Two Years After Birth  Benefits Details

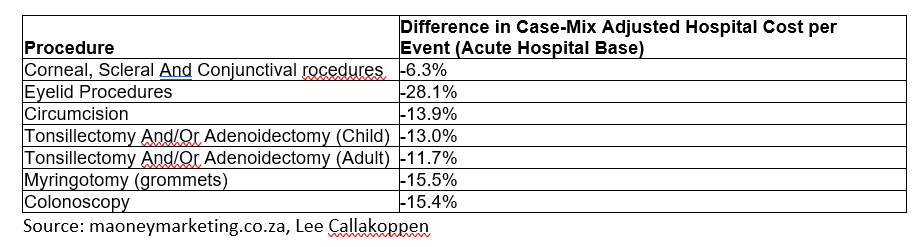

Antenatal consultations You are covered for up to 8 consultations at your gynaecologist, GP or midwife covered from the Maternity Benefit at the Discovery Health Rate. Pre- and postnatal care You have cover for up to five pre- or postnatal classes (including online classes) or post-birth consultations with a registered nurse, up until two years after birth. Once these have been used, we pay antenatal classes from the available funds allocated to your Medical Savings Account. Prenatal screening You are covered for one non-invasive prenatal testing (NIPT) or one T21 chromosome test subject to clinical entry criteria and/or amniocentesis or chorionic villis sampling (CVS) from the Maternity Benefit at the Discovery Health Rate. Blood tests Cover for a defined basket of blood tests per pregnancy from the Maternity Benefit at the Discovery Health Rate. Ultrasound scans You are covered for up to two 2D ultrasound scans including one nuchal translucency test from the Maternity Benefit at the Discovery Health Rate. 3D and 4D scans are paid up to the rate we pay for 2D scans. Medicines for morning sickness, iron supplements and folic acid (Medical Savings required) Discovery pays for medicines and supplements that are taken during your pregnancy from the available funds allocated to your Medical Savings Account. If these accounts are more than the money you have available in your Medical Savings Account, you will have to pay these costs. GP and specialist care after birth Your baby under the age of two years is covered for two visits to a GP, paediatrician or an ear, nose and throat specialist from the Maternity Benefit at the Discovery Health Rate. Other healthcare services You are covered for one flu vaccination during your pregnancy. You also have access to postnatal care which includes a postnatal consultation within six-weeks post-birth for complications postdelivery, a nutritional assessment with a dietitian and two mental healthcare consultations with a counsellor or psychologist. You are also covered for one breastfeeding consultation with a registered nurse or breastfeeding specialist from the Maternity Benefit at the Discovery Health Rate (DHR). Point-of-care devices (Medical Savings required) If you are registered on the My Pregnancy or My Baby Programmes, you also have access to the latest remote monitoring medical examination device called TytoHome until your youngest child turns six. Discovery pays up to 75% of the Discovery Health Rate for one device per family every five years. You will need to pay 25% of the cost of the device. For more information, refer to the Connected Care for healthcare at home guide available on www.discovery.co.za under Medical Aid > Manage your health plan > Find important documents and certificates. Discovery covers normal deliveries or home births or birthing home delivery with a registered midwife If you choose to have a water birth or normal delivery at home or birthing home, Discovery will pay for care from a midwife for your approved delivery from your Hospital Benefit. The midwife must be registered with a valid practice number. For a water birth at home, Discovery will pay for the cost of the hire of a birthing pool from your Hospital Benefit at the Discovery Health Rate. This must be hired from a registered provider who has a valid practice number. If you use a midwife within our network, the birthing pool is included in the amount we pay. Hospitalisation for your delivery You have cover for hospitalisation for your delivery from the Hospital Benefit, if approved. We pay the hospital account from your Hospital Benefit up to the Discovery Health Rate. You have cover for a water birth in hospital. The midwife must be registered with a valid practice number. Treatment for neonatal jaundice If your baby needs phototherapy due to neonatal jaundice, Discovery will pay for the phototherapy lights from the Hospital Benefit as long as you call for authorization. Please consult the treating doctor for the treatment codes so that we can provide you with the authorization number of the treatment. Is Baby Immunization Covered? Baby immunization is paid from your available Medical Aid Savings, if you are on a hospital plan (Core Plan) then you need to pay for it from your own pocket. The suggestion we would provide, whether you have Medical Aid Savings, is that you should call the Dischem near you, ask them if they have stock for government/public immunization shots, this would not only save your time from queuing at a Public Clinic, but also save you money, as the price difference between the private and public immunization shots can be huge. If you would like to know more about your Maternity Benefits, please contact Jo or Namhla in our Health Department email: service@daberistic.com Tel: (011)658-1333  The concept of day hospitals is gaining popularity – particularly because of high hospital stay costs. Day Hospital are there to drive down the cost of procedures affordable. They are also known as Outpatient Surgery Centres which is option of having short stay/day surgical. A day hospital satisfies the patient’s need for a convenient, efficient and lean-cost facility, without compromising on quality clinical care. Advantages of day hospitals 1. No overnight stay – patients are admitted, operated on, and discharged on the same day 2. Child-friendly wards and facilities – day hospitals are the ideal alternative for children requiring same day surgery as the trauma of overnight stays are eliminated. 3. Lower risk of infection – since patients return home on the same day, the risks of cross infection are reduced, which results in a shorter recovery 4. Improved surgery scheduling – decrease in waiting lists 5. More efficient Doctors - Surgeons and anaesthetists are able to plan operating times, thereby increasing their productivity. Internationally there is a trend in increased day surgery for multiple reasons including: • Improved anaesthesia (with quicker recovery period) • Improved pain control (anaesthetic blocks and improved medication) • Instrumentation and procedures (keyhole surgery). Examples of price differences There remains a difference in costs between day and acute hospitals,’ says Callakoppen. The table below represents savings across some of the most prevalent surgeries. Examples of price differences There remains a difference in costs between day and acute hospitals,’ says Callakoppen. The table below represents savings across some of the most prevalent surgeries.  This is probably why the percentage of day cases, split between acute hospitals and day hospitals, is still biased toward acute hospitals. Currently the split of day cases being done in acute hospitals is 74% and 26% in day hospitals. This implies that 74% of all procedures which could be performed in a day hospital are currently performed in acute facilities.

If you would like to know if your option covers for a Day procedure, please contact Jo or Namhla in our Health Department email: service@daberistic.com tel(011)658-1333  Due to pandemic, rising costs and high taxes are eroding pensions and retirement savings in South Africa. Many are forced to use the state-funded healthcare services which is already under pressure, causing long queues and even longer waiting lists.

There is no doubt that we want the best medical attention for our elderly parents when they fall ill therefore private health care is our solution. It is important to understand what options is best suited for your aging parent’s needs. Where do you start? You would need to sit down and discuss with your parents and obtain the following information:

Once you have answers to the above, the next set of questions you need to discuss is to do a realistic budget to finance the plan.

What if your parents cannot contribute? If your aging parents are financially dependent on you and you happen to be main member of a medical aid policy, you may consider adding them as your dependent as this means they can pay a reduced rate. However, they will be on the same option plan as you, should your option not be sufficient to cover their needs, your option is to upgrade your plan. If you’re on an option that includes savings, they become eligible for using your savings. You will need to be prepared for savings being exhausted due to extensive care required. What happens when parents don’t qualify as your dependent? If you decide to not add parents as Dependants or due to parents not qualifying to be your dependent, they can always choose a medical option according to budget and below are things to consider for when choosing your option. Full medical cover (with savings): On a comprehensive option, most elements are covered for. Such as hospital admission, chronic medication and day to day expenses, medical equipment, and possibly dentistry and optometry. These plans vary widely therefore, read through entire plan before signing up to make sure it qualifies all your parent’s needs. Basic hospital plan: These covers around 90% of hospital procedures, basic prescribed minimum benefit (PMB) condition and cancer benefit. It excludes expenses such as none PMB approved medication, equipment, doctor’s visits, optometry, or dentistry. This may not be a full coverage but highly affordable option. Gap cover is always recommended by Daberistic as this boosts your unforeseen gap payment by 500%. To read more about gap cover click here. What else to keep in mind?

If you would like cover for your parents, please contact Namhla or Tammy in our health department, email Service@daberistic.com, Tel 011-658 1333, option 2 for Medical Aid.  Festive season is finally approaching and that means it’s time for holidays. After many countries being on lockdown for the past 18 months and more people getting the vaccine, we can see that more and more countries are opening up for tourists. In the time of such a pandemic it also reminds us how important it is to have medical cover abroad. This cover is known as, The International Travel Benefit covers costs associated with a relevant health service obtained outside of South Africa for a condition or health event that occurs as a result of an accident or emergency.

Most medical schemes include International Travel Benefit for members. With some medical schemes you need to ensure that you need to activate your International Travel Benefit before you travel. With Discovery Health you do not need are to phone ahead to “activate” this benefit, all you need is your departure and re-entry stamps in your passport as proof! Depending on your chosen medical aid option, your cover limit will either be R5 Million or $1 Million and that will alleviate the burden off your shoulders knowing that you will be able to receive the best medical attention whilst on your travel adventures. Principal members and beneficiaries are covered for up to 90 days from the date of departure. Benefits apply to medical emergencies, and are limited to between R5 million and R10 million per trip. Cover can extend to an emergency medical evacuation or repatriation. It's important to note that International Travel Benefit is often excluded from low cost entry level plans. Members of the Discovery Health KeyCare Series and the BonCap option by Bonitas, for instance, are not covered, and will have to make alternative arrangements. What's excluded from cover? There are certain instances when medical aids will not pay for emergency treatment overseas. Common exclusions are:

The medical emergencies claims process If a medical emergency requires surgery, expensive procedures and/or an extended stay in hospital, you need to get authorisation and a payment guarantee from your medical aid's travel partner. In less expensive scenarios, you'll usually be expected to pay the costs from your own pocket, and claim the money back from your medical aid on your return to South Africa. A nominal co-payment may apply for treatment conducted out of hospital. Travel insurance Whether your medical aid option offers international travel benefits or not, it's a good idea to optimise your cover. In some cases – like when you pay for your air ticket with your credit card – you'll automatically get free travel insurance. If you'll be travelling for more than 90 days, or are planning to go dividing, skiing, summit a mountain peak or visit potentially dangerous areas, it's best to purchase comprehensive travel insurance as a separate product. This also means you'll enjoy benefits such as cover for lost baggage, stolen goods and cancelled flights. Important when travelling during Pandemic You may require a vaccine certificate, you may download on website https://vaccine.certificate.health.gov.za/ or contact EVDS tel: 0800 029 999 to request a vaccine certificate. They will need the below information:

If you would like to activate your International Travel Benefit, please contact Namhla or Jo in our Health department, email service@daberistic.com, Tel 011-6581333, Option 2 for Medical Aid. Source: IFC  Women’s medical expenses are usually very different compared to males. It is then vital to choose the medical option that will cover risks specific to women.

Most times women think of pregnancy when wanting medical cover, but it is important to also remember that women are more susceptible to different chronic conditions. Reproductive health Women have many expenses related to their reproductive system. Woman may claim for pap smears, gynaecological check-ups, birth control and mammograms for detecting breast cancer are recommended for all women over the age of 40. The most common is claims during pregnancy, which may include antenatal scans, blood tests and gynaecological consultations, as well as child delivery. Pregnancy can also take a toll on long-term health after childbirth. For example, incontinence, a prolapsed bladder and lower back pain are often directly associated with carrying a child to term. As woman get older, they may also experience Hormonal changes which may make them vulnerable to various diseases, from cervical cancer and osteoporosis to hyperthyroidism and depression. Conditions that affect women more than men It is found that diseases like lupus, rheumatoid arthritis, multiple sclerosis, and type 1 diabetes are far more common in women than men. The other diseases that are common in woman then men are heart disease, chronic fatigue syndrome, irritable bowel syndrome and chronic obstructive pulmonary. Women usually live longer than men. So, it is important to follow preventative or early detection measures, these diseases are:

When shopping or reviewing your medical aid, it is important to choose cover that covers your needs as a woman. Most medical aids cover chronic illnesses, and it’s covered under PMBs (Prescribed Minimum Benefits). This will cover costs for diagnosis, treatment, and care. Some medical aid schemes offer screening and prevention benefits. Discovery Health, for example, covers the cost of one mammogram every two years and one pap smear every three years. It also covers a group of preventative tests, which Discovery refers to as the “Vitality Check.” Consultations are covered from day-to-day benefits. If you would like us to help you with comparison to fit, your medical needs contact Tammy in our Health Department email:service@daberistic.com tel:(011)658-1333 |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|