|

Naji Haddad is a life insurance agent, successful businessman, a proud MDRT member in Beirut, Lebanon. François du Toit interviewed him, he shared his life story of being positive, overcoming adversity and helping people. As people of Beirut deal with the aftermath of a powerful chemical explosion on 4 August 2020, his story touches many hearts.

0 Comments

Discovery Health has launched a new Covid-19 Benefit across its plans. It is called World Health Organization Global Outbreak Benefit. Discovery Health Medical Scheme (DHMS) is taking proactive steps to make sure its members who need it have the necessary cover for COVID-19.

Overview From time to time, there are viruses or diseases that affect world health. These outbreaks are closely monitored by the World Health Organization (WHO) and are, depending on the severity and spread, declared as epidemics that place the global population's health at risk. We recognise the importance of being prepared for these public health emergencies. Through careful benefit design and in support of public health initiatives aimed at containing and mitigating the spread of such outbreak diseases, our members now have access to supportive benefits during the outbreak period. The outbreak is actively monitored by a dedicated team within Discovery Health that closely assesses the evolution and progression of such outbreaks. Having a timely and effective response to global epidemics help to improve the health outcomes for our members. This document explains the cover and support we provide to you when faced with a WHO-recognised epidemic. WHO Global Outbreak Benefit The WHO Global Outbreak Benefit is available to all members of Discovery Health Medical Scheme during a declared outbreak period. This benefit ensures members with a confirmed diagnosis have access to the out-of-hospital management and appropriate supportive treatment as long as they meet the Scheme's Benefit entry criteria. The WHO Global Outbreak Benefit provides cover for a defined basket of healthcare services related to any outbreak disease. How you are covered from the WHO Global Outbreak Benefit When you are covered? The WHO Global Outbreak Benefit is available for the WHO-recognised outbreak period. All healthcare services covered by this benefit are available for confirmed outbreak diseases, as confirmed by a test and subject to the Scheme's benefit entry criteria. This benefit, available on all plans, is covered by the Scheme for confirmed cases of outbreak diseases and does not affect your day-to-day benefits, where applicable. What you are covered for? Cover includes access to a defined basket of care that includes: • The diagnostic tests • Consultations (which can also include video call consultations) • Defined supportive medicine list. Use of the relevant networks as per chosen health plan will apply for healthcare services paid from the WHO Global Outbreak Benefit. More information is available in the following two documents: Guide to Global Emergency Benefit Frequently Asked Questions  outh Africa has a relatively small equities market with a handful of dominant shares, spread across a few sectors, which are available to invest in. This presents a significant risk for investors: a highly concentrated portfolio.

When compared to global markets, the Johannesburg Stock Exchange (JSE) is relatively small, comprising less than 1% of the total global investing universe. It is also highly concentrated, with the top 10 shares on the FTSE/JSE All Share Index (ALSI) making up between 50% and 60% of the index. In contrast, the top 10 shares in one of the world’s major indices, the S&P 500, make up just over 20% of the index. Most of the ALSI’s concentration comes from one share: technology giant Naspers, which makes up 20% of the index. Naspers’ dominance in recent years has increased concentration risk for investors, making portfolios overly sensitive to the factors that drive its value. In general, most investors are happy to contend with the exposure, as long as they are still generating positive returns. But what happens when the proverbial goose stops laying the golden eggs; when the dominant share(s) in your portfolio begins to perform poorly? How you can mitigate your concentration risk As famously stated by American economist Harry Markowitz, who received a Nobel Memorial Prize in Economic Sciences: “Diversification is the only free lunch in finance.” The best way to reduce your concentration risk, without losing out on the potential to earn good returns, is to make sure that you are invested in a combination of assets that have little correlation to one another – essentially, having a diversified portfolio where you generate returns from a wider spread of assets, industries and markets with an acceptable level of risk. To construct a diversified portfolio, one has to consider correlation and volatility. Correlation measures the strength of the relationship between the returns of two assets. A positive correlation indicates a strong positive relationship, i.e. the two assets tend to have higher and lower returns at the same time – this is indicative of an undiversified portfolio. A negative correlation implies the opposite, i.e. returns of the two assets move in opposite directions at any given time. A correlation of zero implies that no relationship (positive or negative) exists between the returns of the two assets. By adding assets with zero, or negative correlation, a portfolio becomes more diversified. You should also look at the overall volatility of your investment to gauge how well your portfolio is diversified. Intuitively, a portfolio consisting of correlated assets should show a larger deviation in its overall returns (i.e. high volatility), while a portfolio that has uncorrelated or negatively correlated assets should show smaller deviations in its overall returns (i.e. low volatility). In essence, if you have a well-diversified portfolio, then your investment should generate returns at lower levels of volatility over the long term. Diversify your portfolio If all this sounds very complicated, you could consider investing in a balanced fund. These are available both locally and internationally and offer a good solution to those investors who want to create a diversified portfolio without the hassle. Your chosen investment manager will carefully select a basket of uncorrelated assets from different markets, companies and industries to ensure that you generate good returns with minimal concentration risk. Local balanced funds offer South African investors some offshore diversification, but remember that Regulation 28 of the Pension Funds Act limits their foreign asset allocation to a maximum of 30% of the fund, with an additional 10% for investments in Africa outside of South Africa. This may not be enough offshore exposure for your needs – in which case you can also invest directly with offshore fund managers of your choice or through an offshore platform, such as the one Allan Gray offers. Every South African resident can use up to R11 million offshore for all foreign expenditure including travel, foreign exchange and for investing purposes. The first R1 million, called the single discretionary allowance, can be used without having to obtain permission from the South African Revenue Services (SARS) and the Reserve Bank. If you want to spend above this allowance, up to R10 million, you would need to get a tax clearance certificate from SARS. To further diversify, many investors choose to invest in more than one of the same type of fund from different managers. If you go this route, it is important to check that the underlying investments are different; otherwise, the combined weighting of the duplicate shares may increase your portfolio’s concentration. Building a diversified portfolio can be complicated and requires a solid understanding of markets and companies. But the good news is that you don’t have to go at it alone. An independent financial adviser (IFA) can help you assess the concentration risk in your portfolio and advise accordingly. It can be tempting to ignore concentration risk when the going is good, and returns are attractive. However, an undiversified portfolio can quickly become a problem if your most concentrated shares begin to perform poorly. Source: Vuyo Nogantshi , Allan Gray  In this article, we focus on Excess – the amount which you have to pay when you claim from your insurer (whether you are at fault or not) unless if you have elected to pay an additional premium for an excess-free policy. So, what exactly is an excess and why do insurers apply these charges to insurance claims?

What is an excess? An excess is the uninsured portion of your loss or that portion of the claim you must pay for. When the amount that is claimed is less than the excess, no payment will be made by your insurer. Why do you pay an excess? Insurers use excesses as a way to make sure that you do not claim for every small loss. They do so not only for their own benefit but for all policyholders to ensure that insurance does not become unaffordable, because eliminating these claims and their associated costs helps keep premiums lower for you. An excess also acts as an incentive to ensure that you take responsibility for the safety and security of your possessions. Are there different types of excesses? There are many different types of excesses used by insurers. As a general rule of thumb – the lower the premium relative to the market standard the higher the excesses. Examples as follows:

The insurer needs to bring to your attention, when the contract of insurance is entered into, the standard excess and all other excesses that may be applicable when you claim. You can always enquire from your insurer if an excess can be completely done away with. This is referred to as an excess waiver. The important thing is that you understand why and when you pay an excess so that you can make an informed decision when taking out the insurance. Does an insurer have to recover the excess you paid? If someone else has caused your loss, the insurer may be able to recover the cost of the claim, including the excess you paid, from them or their insurer. The success of a full recovery however depends on several factors, including whether you identified the other party, whether they admitted fault, whether there are any witnesses, whether they have insurance and, if not, whether they have the ability to pay. What if your insurer does not recover the excess you paid? If the insurer decides that it is not going to attempt a recovery of the claim cost or it does not succeed in making a recovery, the insurer should advise you so that you can decide whether to attempt a recovery of your excess yourself. With the consent of the insurer, you may then proceed to recover your excess directly from the third party. We at Daberistic believe that by providing the right advice and solution to clients, we can create win-win relationships which will ultimately benefit everyone. If you are looking for advice on your short-term insurance needs, you can contact us on the following channels:

Medical aid is a form of insurance where you pay a monthly amount, called contribution or premium, in return for financial cover for medical treatment you may need, as well as any related medical expenses.

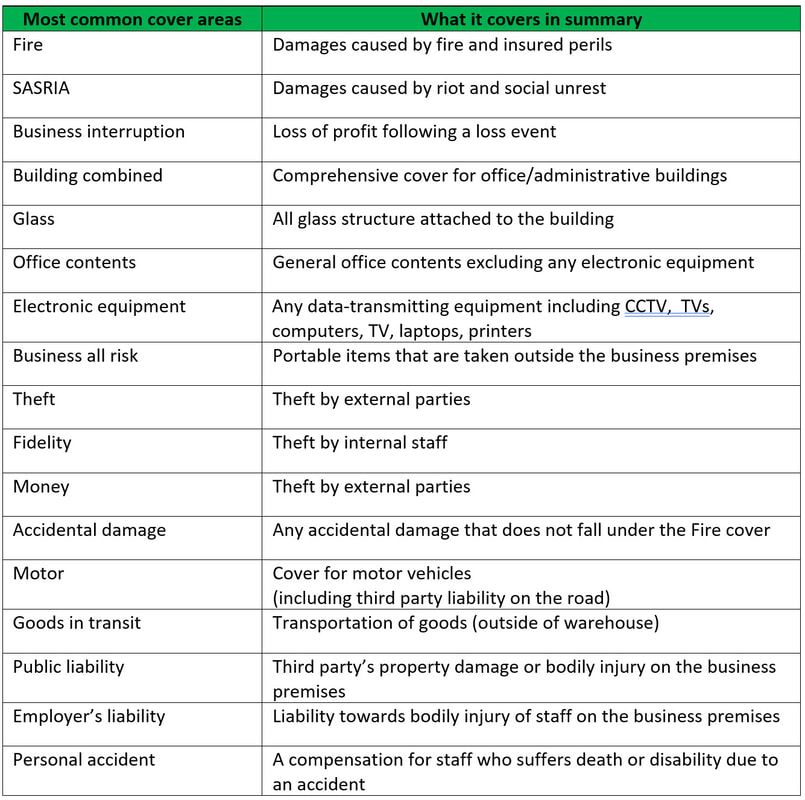

Medical aid and health insurance are two different products. Medical aid, or medical scheme, is regulated by the Medical Schemes Act, provides in-hospital cover and chronic illness benefits, and pays for treatment according to specific medical scheme tariffs. Some medical aids also provide for day-to-day medical expenses. Health insurance, on the other hand, is regulated by the Short-term Insurance Act. It provides a more limited set of health benefits, up to a monetary limit. Health insurance is a cheaper alternative for people who cannot afford medical aid. Why medical aid is important Having a good medical aid plan with a reputable medical scheme can help you protect both your health and your wallet. The reality is that your health, and that of your family holds immeasurable value to you. There are many advantages of belonging to a medical aid. It financially protects you if you suddenly have to pay large, unexpected medical costs. Being a member of a scheme also means you have access to private medical care, instead of having to rely on public health services. If you are looking for advice on healthcare needs for you, your family or your company, you can contact us on the following channels: - WeChat: daberistic - Email: Health@Daberistic.com - Phone: working hours 011 658 1333  Author: Edmond Lee Commercial insurance is a necessity for business owners, but at the same time it is a rather complicated area to understand. We at Daberistic believe in simplifying insurance for our clients, so this article will shed some lights on the basic structure of commercial insurance in South Africa. In the early eighties there were many short-term insurers, flooding a variety of commercial insurance policy wordings onto the market. A sensible comparison of benefit between these policies was virtually impossible, which was to the detriment of the small business insurance consumer. Hence the regulator responded by introducing a standard business policy - known as "Multimark" - in 1987. Over time, Multimark was revised, and today we have the Multimark 3 wording available to us. Even though insurers have since introduced various endorsements to differentiate their products, the basic structure remain largely the same, as the Multimark’s risk-based approach is a solid foundation which ensures that various sections in the policy cover various risks and premium are calculated accordingly. As an example, Fire has a low probability of occurrence but high severity (i.e. all stocks can be affected) if it occurs, as opposed to Theft which has a higher probability but lower severity (because robbers or burglars cannot possible steal all your stock), which explains why covers are broken down into various section. Below is a table summarising the various key sections and their cover areas.  The scope of commercial insurance is broader than the above and continues to evolve as the risk landscape changes, resulting in other covers such as Products liability, Directors’ and Officers’ liability, Cyber crime, Commercial crime, Credit insurance – just to name a few. It is therefore crucial that you make use of an insurance advisor who can advise you on your risks and propose covers that meet your needs.

We at Daberistic believe that by providing the right advice and solution to clients, we can create win-win relationships which will ultimately benefit everyone. If you are looking for advice on your short-term insurance needs, you can contact us on the following channels:

Author: Edmond Lee

So you recently bought short-term insurance, thinking that you are covered fully regardless of the circumstances? Think again. Many insurance buyers forget that insurance is based on certain fundamentals which must be adhered to in order to have continuous cover. The rationale is that although insurance is a risk transfer mechanism, there is still a responsibility for client to manage risk effectively. Below are some key ones which may be useful to you. Did you know?

Below are some key points that relate specifically to motor insurance:

We at Daberistic believe that by providing the right advice and solution to clients, we can create win-win relationships which will ultimately benefit everyone. If you are looking for advice on your short-term insurance needs, you can contact us on the following channels:

|

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|