Here’s what you need to know about your IT3B and IT3C certificates:

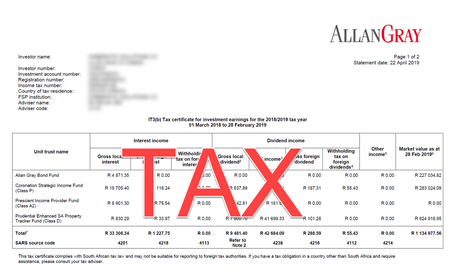

The IT3B certificate is all about the income you’ve generated from your investment. It’s going to reflect: Local dividends: this is the amount which has been paid to you in dividends from JSE listed companies in the last tax year. We automatically pay 20% dividend withholding tax on these for you, so this appears on your certificate to let SARS know that it’s done and dusted. Make sure you disclose this on your tax return and that’s it - finished and klaar. Foreign dividends: this represents any dividends you received from JSE listed companies which earn money overseas. We’ve paid the 15% dividend withholding tax on your behalf, but you still need to disclose this on your tax return. Taxable dividends: This represents REIT (Real Estate Investment Trust) distribution and applies to those of you who hold shares in a company that invests in property. Interest: This amount of interest, which you earn on local and foreign investments, is considered as income and you'll need to declare it to SARS. Bank Accounts Interest: This is the interest you earn on your bank accounts and deposit accounts. Any interest you earn in a year over R23 800 (R34 500 if older than 65) is taxable when you submit your tax return. The IT3C certificate is all about capital gains. How much did your investment grow? Did you sell anything? Did you earn any profit by doing so? You’re only taxed on shares or unit trusts that you sell. Your IT3C certificate is going to show: A list of companies or unit trusts you’ve invested in; How many shares/units you have in each and how much you bought them for. Because you can buy shares for a certain price on one day, and then buy more of the same shares on another day when the price is different, the cost per share is going to be shown as an average of those prices – to keep things simple! So if you bought 1 share at R50 on Monday and another at R100 on Wednesday, you’d have two shares which you paid R150 in total for. Even though they were bought at different prices, the average cost per share is going to be: R150 divided by 2 shares = R75.00 per share. If you’ve sold a share at a higher price than when you bought it, you’ve made yourself some dosh haven’t you? SARS is going to want in on that. ‘Proceeds’ is going to reflect the amount you sold your shares at and ‘Profit/loss’ is going to reflect how much money you made or lost in that sale. The good news is that SARS is only interested in this amount if it is greater than R40 000 – that’s when you’ll start getting taxed on it. Adapted from: Easy Equities

0 Comments

Around this time of the year, we would like to remind you to consider topping up your retirement annuity fund and tax-free investment.

Retirement Annuity According to the current legislation, you may contribute up to 27.5% of your taxable income (strictly speaking, non-retirement funding income) to a retirement annuity fund and enjoy tax deductions. As 28 February is the end of the tax year, you must calculate and pay the additional amount to your retirement annuity prior to this date, in order to qualify for tax deductions and tax refunds. Below is an example of topping up your retirement annuity: Ms Rama has a monthly salary of R80,000. In December she received a bonus of R100,000. Every month she contributes R5,000 to a personal retirement annuity fund. Her annual income is then R80,000*12 + R100,000 = R1,060,000. The maximum tax-deductible contribution to retirement annuity is R1,060,000 * 27.5% = R291,500. Over the year she has contributed the following to a retirement annuity fund: R5,000 * 12 = R60,000 The additional amount she may top up in his retirement annuity (RA) is R291,500 Less R60,000 = R231,500 Tax-free investment You may contribute up to R36,000 to a tax-free savings account in a tax year. You must calculate how much you have contributed so far since 1 March 2020 and pay the additional amount to your tax-free savings account prior to 28 February, in order to make use of current tax year's allowance. You can also start a tax-free investment in the name of your children. To top up your retirement annuity or tax-free investment, please contact service@daberistic.com  Around this time of the year, we would like to remind you to consider topping up your retirement annuity fund. According to the current legislation, you may contribute up to 27.5% of your taxable income (strictly speaking, non-retirement funding income) to a retirement annuity fund and enjoy tax deductions. As 28 February is the end of the tax year, you must calculate and pay the additional amount to your retirement annuity prior to this date, in order to qualify for tax deductions and tax refunds.

Below is an example of topping up your retirement annuity: Mr Jackson has a monthly salary of R50,000. In December he received a bonus of R100,000. Every month he contributes R3,000 to a personal retirement annuity fund. His annual income is then R50,000*12 + R100,000 = R700,000. The maximum tax-deductible contribution to retirement annuity is R700,000 * 27.5% = R192,500. Over the year he has contributed the following to a retirement annuity fund: R3,000 * 12 = R36,000 The additional amount he may top up in his retirement annuity (RA) is R192,500 Less R36,000 R156,500 To top up your retirement please contact invest@daberistic.com  Let us use a case study to illustrate how financial planning can help a young family. Gavin lives in Joburg, 29 years old, is married to Ntombi with a 1-year old son Siya, named after the Sprinbok captain Siya Kolisi. Gavin works in a family business with a monthly salary of R30,000. In addition, he gets extra income of about 2,000 US dollars per year from YouTubing. The monthly expenditure of Gavin's family is R18,000. He can save about R10,000 a month. Looking at Gavin's personal balance sheet: He has no house, no car under his name, and no loans. He has R200,000 in bank deposit. He has a 10% stake in the family business. He has a life insurance policy with the following benefits: Life insurance R2, 361,000. Lump Sum Disability R2, 361,000 Severe Illness Benefit R944,400 Income disability benefit R7,300 per month He contributes R1,277 per month to a retirement annuity, retirement age 55, and current value R61,500. Gavin's family is on Discovery Essential Saver option, plus a gap cover policy to cover for medical expense shortfalls. The marriage between him and his wife is in the community of property. His wife is a housewife. His financial dependants are his wife and son. Gavin would like to buy a house of his own and invest overseas. Asked about his retirement planning, he says that he would like to retire at the age of 55 (although he knows it might be an unreachable dream), with a monthly income of R15,000 in today's money, plus travel abroad every year. The house and car loans will be paid off and there is an emergency reserve. For his children, he wants to provide for their education, until they complete their university degrees. I use a professional financial planning program to do financial needs analysis for Gavin and produce a financial need analysis report. Then I draft a proposed financial plan, with some preliminary recommendations to Gavin and Ntombi: 1. Risk planning Since Gavin has a single-income family, his child is still young, his life insurance is insufficient. He needs an additional R4,700,000 cover to provide protection for his family, especially his child's future education and living expenses. According to the financial analysis, he has enough severe illness insurance coverage and lump sum disability cover. His income disability benefit needs to be raised to R13,700 per month. The objective of income disability benefit is that when the insured is temporarily or permanently unable to work, the insurance company pays a monthly income as compensation until he goes back to work or until his retirement age. The cost of additional insurance benefits is R412 per month. I recommend that Gavin buys Discovery Global Education Protector, private school option. If he dies, is disabled or has a major illness, Discovery will cover the cost of tuition and extracurricular activities until the age of 24. It also includes a University Funder Benefit, which helps to pay part of his child's tertiary education fees . Monthly premium R358.07. 2. Investment planning I use the three-bucket approach to financial planning, which is easy for clients to understand.  The first bucket of money is the money needed in the next two years. It needs to be capital secure and highly liquid. It can be withdrawn at any time. It can be an emergency fund. I suggest that Gavin has R200,000 in the bank, in a high-interest account such as money market account or call account, which can withdrawn at any time.

The second bucket of money is the money needed for years 3 to 10. It can partially invest in growth assets, but seek stability. A suitable investment vehicle is a conservative fund. Part of the child’s education fund belongs to this bucket. The third bucket is the money that is needed only after ten years, usually for retirement funding, child’s education fund and long-term capital growth. I suggest that Gavin invest in equity funds, which have shown to have the highest long-term returns over the long term, but have short-term fluctuations (volatilities). It can be done on a debit order basis, to benefit from a disciplined investment approach and Rand cost averaging. In addition, I suggest that he invest overseas, in US Dollars, to benefit from investment opportunities internationally, diversify risks, and hedge against long-term depreciation of the South African Rand. He can open an account with a minimum investment of 1,500 US dollars. 3. Education fund The analysis points out that Gavin needs to invest R6, 898 every month for the next 18 years, for his son's education. I suggest that he can start a tax-free investment account in his son's name and debit R2,750 from the bank each month to invest in a long-term growth portfolio. The investment value is expected to be R1,121,886 after 15 years. 4. Retirement planning In calculating the capital required for retirement, I used the following assumptions: Retirement age 65 (not client's wish of 55) Monthly income, today's value of R22,100. This is not the R15,000 Gavin indicates to me in the initial discussions, as after taking into account the medical expenses in the old age and the desire to travel abroad, this is the more realistic figure. Inflation rate 6% Investment return 8% The retirement capital required is R31, 415, 100. Gavins existing Retirement Annuity is expected to reach R6,077,840 on retirement. In order to achieve the retirement income target, Gavin needs to invest an additional R5,390 per month, increasing by 6% per year. 5. Estate planning I recommend that the Gavin and his wife make a joint will to distribute the estate in South Africa as he wishes. From this case study, you can get a glimpse of the process, details and the wide areas covered in personal financial planning, tailored to the needs of a person or a family. The more assets and the more complex a person's financial situations, the more complicated is the financial, tax and estate planning required.  [The tax e-filing season is upon us. If you need a tax consultant to help you with your e-filing, please contact Daberistic Accountants at 011-658-1333, email tax@daberistic.com.]

During a media briefing in Pretoria on Tuesday, new SARS Commissioner Edward Kieswetter told the South African public that the tax threshold for those who have to submit returns will be increased this season. Kieswetter’s announcement was initially delayed due to a massive power outage across the city. However, when the lights returned, the new tax chief dished out some encouraging news for those earning a low-to-mid range income. SARS tax threshold: Am I exempt from filing a tax return? Instead of requiring tax returns from everyone who earns R350 000 a year, that minimum figure has been increased to R500 000 a year. In monthly terms, the parameters have shifted from R29 166 to R41 666. However, it’s not all plain sailing for those of us making less than half-a-million per annum. The new threshold laws only apply to citizens if they meet the following set of criteria:

When is tax season in South Africa for 2019? Kieswetter was also keen to encourage more citizens to start using SARS’ e-filing systems. He revealed to tax-paying South Africans that the programme has gone through several updates, and more improvements will be in place by August. One of the incentives for using the e-filing systems is that they help with time management. Yes, tax season will start on 1 August and end on 31 October, but electronic applications start at the beginning of July and remain open all the way through until the last day of January 2020. It’s also worth noting that returns filed via SARS’ app have a deadline of 4 December 2019. Depending on what you’re earning and the new tax threshold, this could be a trouble-free season for many of SA’s workers. Source: thesouthafrican  According to a study, 90% of people who retire with money from their retirement funds buy living annuities to provide them with a regular income in retirement. So what are living annuities? And what are life annuities? Are life annuities dead? I would like to explain these two types of products for provision of retirement income. It would be very beneficial for you to generate a more detailed financial plan to give you a better understanding of your options. You can use this tool from 10x. Life annuities and living annuities are the two main products that can provide you with an income from your retirement savings. A life annuity is an insurance-type product and a living annuity is an investment-type product. Each of these meets different needs so you will need to decide which will best meet your particular goals. Life Annuity Life annuity is also called fixed annuity or guaranteed annuity. A life annuity is a contract between you and a life insurance company. You give the life insurance company a retirement capital lump sum. In return, it secures you a pre-determined income for the rest of your life. There are different types of guaranteed annuities. Some provide an income that increases with inflation, others pay a level income and others yet may increase over time, subject to market returns. In order to ensure a level of income that sustains your lifestyle needs, you should consider an inflation-linked life annuity, which provides an income that keeps pace with inflation. Although your income is guaranteed for your whole life, your income ceases when you die. Your heirs won't be able to inherit whatever is left on the death. In other words, the capital dies with the investor. For the sake of guaranteeing value for money, I suggest you purchase a life annuity with an underlying guarantee of income for a minimum period, typically between 10 to 20 years. This period is called a guarantee period. A life annuity with a guarantee period will pay a slightly lower retirement income than one without a guaranteed period. Typically, you also have no say over the initial income and no flexibility to change your income or to move to another annuity or service provider once you've purchased the product. It is wise to use a financial advisor to get quotes from reputable annuity providers, to get the best initial income, terms and conditions. Living annuity On the other hand, a living annuity provides investors with flexibility to choose their income each year (subject to regulatory limits) and where their money is invested. This will give you the flexibility to draw a lower or higher income as and when your needs change. It will provide you with the flexibility to change service providers or purchase a guaranteed annuity at any time. Any remaining capital upon death passes to your heirs. However, in exchange for this flexibility, you take on the risk that the income may not last for your retirement years (on average about 30 years), as well as the risk that their investment returns are poor. This means that your future income could fail to keep up with inflation, or even that you outlive your savings. Below is a table summarising the difference between an inflation-linked guaranteed annuity and a living annuity:

Tax At retirement you may cash in up to 100% of the value of your provident fund, up to one-third of the value of your pension fund, and up to one-third of the value of your retirement annuity. However, there are potentially tax implications to taking a portion in cash. The table below shows you the tax rates for various cash amounts taken at retirement.

In addition to the tax above, the income you receive from either a life or living annuity would be taxed as per the applicable income tax table.

Which one should you buy? There are three possible options: A life annuity, a living annuity, or a combination of the two. Yes, it is possible to deploy your retirement capital to both types of products at the same time. There are two important factors to consider when you buy annuities: Health and flexibility. If you are healthy and your family exhibits a history of longevity, you should consider buying a life annuity with at least part, if not all of your retirement capital, with the balance in a living annuity. People that live longer will score with a life annuity, as they will get (a lot) more than they put in. While the liviing annuity gives you the flexibility to adjust your income as and when your needs change. If you are not healthy, e.g. having chronic conditions such as diabetes, heart conditions, hypertension, you may want to put most, if not all of your retirement capital into a living annuity. This way, you can enjoy the fruits of your years of hard work and savings while still alive, and able to leave the balance to your loved ones when you die. The balance is invested in a life annuity, to provide you with some guaranteed income. With a living annuity, the recommended drawdown rate, the percentage of the capital you draw as income, is 5% per annum. This would ensure the money should last you for up to 30 years in retirement. If you need a higher level of income, you should buy a living annuity, which allows you to withdraw up to 17.5% of your capital as income. Bear in mind that the more you withdraw, the quicker the money in a living annuity runs out. Allan Gray has provided an excellent summary of the 2019 budget speech. We would like to share with you here: What were the key changes? |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|