Firstly, let me dedicate this report to my Lord and Saviour Jesus Christ, may honour and glory be to Him forever and ever! As a Financial Advisor with actuarial qualifications, I am particularly fascinated by investments. I have spent lots of time over the last 21 years studying the subject of investment. I have learnt and analysed all kinds of financial instruments, including shares, unit trusts, CFDs, futures, warrants and ETFs. Over the years the investment markets have taught me a lot of things. It has taught me to be humble. It has taught me to be a ready student, to continue to learn, think and reflect. In the past I have written about share analysis, technical analysis, and general investment advice. This is the first time I write and share a comprehensive report on unit trusts. Over the years I have appreciated the way good unit trusts, or Collective Investment Schemes, has helped me and my clients grow my wealth. They have provided many investors an excellent way of investing in a diversified portfolio of assets, that over the long term have demonstrated significant real returns. This first comprehensive report on unit trusts focuses on high-growth unit trusts. I share this report with my fellow financial advisors in the hope of helping you help your clients make better, independent, informed investment decisions. If you like this report and think this report has helped you, please like it on LinkedIn and share it with financial advisors. Please also comment on this report, so that I can know whether I am on the right track, and how I can continue to refine my investment thinking. Click the link below to download the report.

0 Comments

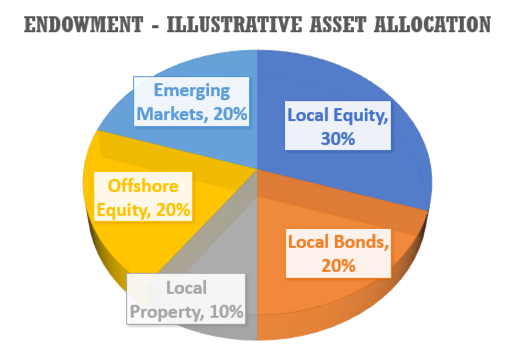

An endowment is a type of investment plan that can hold a variety of underlying investment options, including unit trusts and a share portfolio. It requires an investor to invest for a minimum period of five years. It provides investors with full access to their money after five years or when the policyholder dies. In South Africa, endowment plans are taxed at reduced rates (compared to the typical tax rate of an individual in the highest income tax brackets). When you do decide to withdraw your money, you won’t have to pay any further tax on your investment.

There are two main considerations around endowments: tax and estate planning benefits. Income received in an endowment is taxed at a flat rate of 30% for individuals and trusts, while capital gains is taxed at 12%. 20% dividend withholding tax also applies. Tax on returns is deducted and administered by the product provider. The Long-term Insurance Act that regulates endowments imposes a few restrictions: During the first five years of your investment, known as the restriction period, you may only make one withdrawal. The maximum withdrawal during this period is limited to the amount invested plus interest at 5%. The balance may be withdrawn after five years However, when you are not in a restriction period, you may withdraw from your investment at any time, or schedule regular withdrawals. Your five-year restriction period may be extended if you invest more over one year than 120% of your investments over either of the past two years. Most life insurance companies and investment platforms offer endowments. In the event of your death, your beneficiaries can receive your investment immediately and there are no executor's fees. This amounts to a saving of up to 3.99% of fund value. Tax administration is taken care of on your behalf (the insurance company calculates, deducts and pays the taxman). The entire value of the endowment will be protected against creditors after three years. This protection will continue until five years after the termination of the endowment. You are not restricted to maximum levels of equities and offshore investments, as in the case of retirement annuity. You can also use an endowment to draw income upon retirement, as long as the five-year restricted period has passed. You can do this on an ad-hoc basis, without being forced to draw income at specific intervals. Return profile: It will depend on the type of unit trust you invest in. If your underlying investments are income unit trusts, you may expect a net annualised return of 4% after fees and tax. If your underlying investments are high growth unit trusts, you may expect a net annualised return of 6.5% to 9% after fees and tax. Who is it suitable for:

This group of unit trusts typically has a relatively low weighting, up to 40% of the money, invested in the stock markets, or equities. Most Stable Growth Unit Trusts invest the majority, some up to 100%, of their money in fixed income instruments such as bonds and money markets. It may have some exposure to property and offshore fixed income.

Generally this group of unit trusts invest its money to provide a relatively stable stream of income and return to its investors, so it is conservative in its risk management approach. The risk of capital loss over any 12-month period is low. Return profile: Expected stable high returns over the short term (1 to 5 years), on average 7% to 9% per annum. Volatilities: Stable Growth Unit Trusts’ price movements are muted compared to Balanced Growth Unit Trusts. Money Market unit trusts have a constant price of R1. Who is it suitable for: • Older, conservative investors for whom wealth preservation is very important. • Corporate cash management for enhanced yield. • Investors looking for short-term investment objectives (1 to 5 years). Many people have negative perceptions about retirement annuity. I must state categorically that this is a powerful tool in any investor’s financial and tax planning. A retirement annuity is a long-term investment structure for building retirement savings, either on a recurring basis or by making a lump sum investment. A retirement annuity offers significant tax advantages to people who are committed to investing their money until they are at least 55 years old. A portion of your retirement annuity contributions is tax deductible. The current legislation allows you contributions to retirement funds of up to 27.5% of your taxable income as tax deduction, subject to a maximum of R350,000 in a tax year.  All your investment growth, including interest, dividends and capital gains within a retirement annuity is tax free.

At retirement age, you may withdraw a portion of your retirement annuity account tax free. Currently the first R500,000 lump sum benefit is tax free. The balance of the account will be used to purchase a fixed annuity or living annuity, to give you a monthly income. You can select the underlying investment portfolios in a retirement annuity. These investment portfolios are compliant with Regulation 28 of the Pension Funds Act, to ensure your money is invested prudently across a number of asset classes. Before retirement, there are three scenarios where you may access money in your retirement annuity account: In the event of your death, the money is paid out to your beneficiary. In the event of ill health and you are unable to work, you lodge a claim for a disability benefit – and not a withdrawal benefit – from your retirement fund. When you emigrate or when you leave South Africa due to an expired work visa, you can withdraw the full value in cash (subject to tax). There are two types of retirement annuity products: Life assurer retirement annuity and unit trust retirement annuity. With a life assurer retirement annuity, you enter into a contract to commit to pay contributions until your selected retirement age. Should you reduce or stop contributions during the first half of the term, you will pay a penalty charge, which reduces your retirement annuity account value. Some life assurers will reward you with bonuses paid into your account for being disciplined with your monthly contributions over the term of the contract. While a life assurer retirement annuity is rigid, a unit trust retirement annuity gives you flexibility. You may increase, reduce or stop contributions at any time without penalties. You may wish to consider investing in a retirement annuity fund if:

A word of advice: If compound interest is the first Financial Wonder, then I consider retirement annuity to be the second Financial Wonder in South Africa.  This group of unit trusts has 100% of the money invested in offshore assets, predominantly in offshore equities. It may have some exposure to the listed property sector, as well as cash and bonds. Given the fact that South Africa only accounts for 0.5% of the world economy, and there are many excellent, well-known international companies not available for investing in South Africa, I encourage investors looking to maximise their returns over the long term to allocate a high percentage of their portfolio to Offshore Unit Trusts. You will also benefit from expected Rand depreciation against the US Dollar over the long term.

International giant brands not available for investing in South Africa include: Alphabet (parent company of Google) Amazon Apple Berkshire Hathaway Microsoft Nestle Samsung Unilever Return profile: Expected high returns over the long term (10 years plus), on average 12% to 16% per annum Volatilities: As stock markets fluctuate, reacting to news and market sentiments, offshore unit trusts also fluctuate daily. It goes up one day, down the next. It goes up one month, maybe down the next. In addition, there is also exchange rate fluctuation, which may magnify price movements if you invest in Rand-denominated Offshore Fund locally. Who is it suitable for:

This group of unit trusts typically has a relatively high weighting, up to 75% of the money, invested in the stock markets, or equities. Most balanced (or known as multi-asset, high-equity) unit trusts invest according to Regulation 28 of the Pension Funds Act, which means up to 75% of its money invested in equities, up to 25% invested offshore, up to 5% invested in Africa, with the balance invested in bonds, money market and property. It may have some exposure to precious commodities such as gold.

Generally this group of unit trusts invest its money for retirement fund members in South Africa, so it is fairly moderate in its risk management approach. It would not want to risk people’s retirement savings. It invests in quite a number of different assets and different companies to diversify. Return profile: Expected higher returns over the long term (5 to 10 years plus), on average 8% to 12% per annum. Volatilities: As stock markets fluctuate, reacting to news and market sentiments, balanced unit trusts also fluctuate daily. It goes up one day, down the next. It goes up one month, maybe down the next. However, the price movements are muted compared to High Growth Unit Trusts. Who is it suitable for:

Robert Kiyosaki multimillioanire and author of "Rich Dad, poor dad" wrote this blog about The mistake millenial parents mistake regarding their children and finance. This is what he had to say;

More and more there is an interesting trend: parents paying down the cost of their children’s debt. Whether it be student loans, home down payments, or living at home because of credit card debt, parents of millennials are footing the bill—or at least significantly helping pay down—for their kids’ big debt costs. On one level, I can understand this impulse. Parents naturally love their children and want to help them start life on the right foot. And the high levels of debt that most young people have, along with low salaries and poor job prospects, make it very tough for them to get ahead. But I believe that footing the bill for your kids actually hurts them more than it helps them. The pain of financial failure My first business sold nylon and Velcro surfer wallets. We worked out licensing deals with famous rock bands and put their logos on the wallets. The sold like hotcakes and the company grew very quickly. But I made a huge mistake. My attorney told me that I should patent my idea. When I heard that it would cost $10,000 to do so, I said no way. Soon another company came along and copied my idea, cutting into my market share. On top of that, I had a number of distributors who owed me money but were not paying. Soon my company was in dire straits and I decided to meet with my rich dad. What I hoped to get out of the meeting with rich dad and what I got were two very different things. My hope was that rich dad would show me a path forward to save my business—and maybe even to offer some financial support. Instead, rich dad looked over my financials, stared me in the eyes, and said, “Your company has terminal financial cancer. You have grossly mismanaged this business and it can’t be saved.” In my arrogance, I tried to convince him that he was wrong about my business, but deep down I knew he was right. Eventually I had to liquidate my business. In the process, I went $1 million in debt. The pain of this financial failure was very acute. Digging out of debt Soon after that, I met Kim. I didn’t think this beautiful woman would want to be with a guy whose business just failed and was $1 million in debt, but we fell in love and she stuck with me. Together, we worked hard to build a new business centered around financial education—at times living in our car or on friend’s couches to make ends meet. We both knew we didn’t want to simply go and get a good job. We wanted to build a company and we found our purpose in life. That clarity of vision allowed us to make the many sacrifices we needed in order to achieve our goal. Eventually, Kim and I paid of the $1 million in debt and built a successful business. Along the way we learned invaluable lessons not just about money but also about ourselves. The pain was necessary The easy path for rich dad would have been to placate me, sugar coat his assessment of my business, or even to give me a loan to see if I could turn it around. Any of those options would have done me a huge disservice. Ultimately, it was rich dad’s hard words—and the hard years that came after them—that led to my success later in life. I can confidently say that had it not been for the hard truth that rich dad gave me, I would not be where I am today. The financial pain was necessary for me, and it’s necessary for your kids. How to really help The easy way out for parents is to pay for their kids’ expenses and debt. The hard way forward is to watch them struggle financially while working with them to build their financial intelligence. Rather than foot the bill, I encourage all parents to invest in their children’s financial education. Don’t pay for the debt, but do take them to a seminar that can change their perspective on money and the world. Spend time rather than cash to go over their financial statements and coach them on how to make better financial decisions. And be there when they need a shoulder to cry on. Only by owning their own financial future will our children grow to prosper and thrive in a world where it is increasingly hard to financially survive. Where to start The good news is we have many resources to help you do this. Start with going over the new rules of money: Money is knowledge Learn how to use debt Learn how to control cash flow Prepare for bad times and you will only know good times The need for speed Learn the language of money Life is a team sport; choose your team carefully Since money is worth less and less, learn how to print your own From there, I encourage you to read and study Rich Dad Poor Dad, which has just been released in a new and updated edition, and take the time to play CASHFLOW together, which was created to put the rich dad principles into real world simulation. You can play online for free. Once these foundations of financial intelligence are in place, you can then begin advanced work with a coach, as well as attend specialized workshops and seminars. And best of all, you can formulate a plan to even invest together. Kim and I started the Rich Dad Company many years ago precisely because we want to see you and your kids enjoy the financial success that comes from the lessons handed down to us and learned along the way. Why not start today? To get get assistance for your financial planning for your whole family, please contact Kevin or Thato in our Invest Department, email invest@daberistic.com, tel (011)658-1333 Written by: Robert Kiyosaki Source: Richdad |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

||

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|