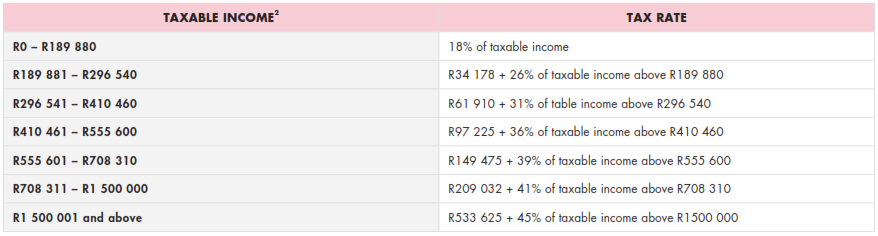

INCOME TAX Individuals and special trusts A new top bracket has been introduced for personal income tax - individuals’ taxable income above R1.5 million per year will be taxed at 45%. Previously, the top bracket of 41% was set at R701 301. The new top marginal income tax bracket is accompanied by partial relief for bracket creep 1. The personal income tax rates for the 2017/2018 tax year are listed below.  Companies and trusts

TAX RATE The income tax rate for companies has remained unchanged at 28%, while the income tax rate for trusts (other than special trusts) has increased to 45%. TAX THRESHOLDS Tax thresholds have increased to: „„ R75 750 for taxpayers younger than 65 „„ R117 300 for taxpayers aged 65 to below 75 „„ R131 150 for taxpayers aged 75 and older REBATES The primary rebate (deductible from tax payable) has increased to R13 635 per year for all individuals. The secondary and tertiary rebates have increased to: „„ R7 479 for taxpayers aged 65 and older „„ R2 493 for taxpayers aged 75 and older INTEREST EXEMPTIONS Interest exemptions have remained unchanged at: „„ R23 800 per annum for individuals younger than 65 years „„ R34 500 per annum for individuals 65 years and older MEDICAL TAX CREDITS Monthly tax credits for medical scheme contributions will increase from: 1.R286 to R303 per month for the person who pays the contributions and the first dependant on the medical scheme 2.R192 to R204 per month for each additional dependant Bracket creep occurs when the income tax tables are not fully adjusted for inflation, and inflationary salary adjustments increase an individuals’ effective tax rate, reducing real income. As the increases to taxable income brackets, the tax thresholds, and the rebates are below the expected level of inflation, taxpayers will face a real increase in their effective personal income tax rate in 2017/2018. INTEREST WITHHOLDING TAX (IWT) AND DIVIDEND WITHHOLDING TAX (DWT) Interest Withholding Tax (IWT) on interest from a South African source payable to non-residents has remained unchanged at 15%. Interest is exempt if payable by any sphere of the South African government, a bank or if the debt is listed on a recognised exchange. Dividend Withholding Tax (DWT) on dividends paid by resident companies and by non-resident companies for shares listed on the JSE has increased from 15% to 20%, effective 22 February 2017. The exemption and rates for inbound foreign dividends have also been adjusted in line with the new local DWT rate, resulting in a maximum effective rate of 20%. TAX-FREE SAVINGS ACCOUNTS The annual limit on contributions to tax-free savings accounts has increased from R30 000 to R33 000. RETIREMENT LUMP SUM TAXATION At retirement: The retirement lump sum tax table is unchanged. The table below illustrates how retirement lump sums will be taxed. Click to read more If you have any queries on your personal or business tax, contact our Finance Department, email finance@daberistic.com, tel (011)658-1333 Source: Allan Gray

0 Comments

Leave a Reply. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|