The 2017-18 budget provided limited relief for fiscal drag and introduced a personal income tax of 45% for individuals earning R1.5m or more. The previous top bracket of 41% was set at an income of R701,301. Tax collections have fallen sharply in light of poor econo-mic growth and the Treasury has had its worst performance in collections since the 2009 recession. So the trend of increasing taxes seems likely to continue as the Treasury sets about on what it calls a "measured, prudent course of fiscal consolidation". In the light of this, it is now more important to plan your financial affairs effectively from a tax point of view. There are several structures you can employ legally, without much cost, that can be quite effective in reducing the amount of tax you pay on your investments. One such structure is an endowment, which has potential tax advantages for investors in higher tax brackets and can also be used for estate planning. There are typically two types of endowments: "traditional" and new-generation unit trust-based endowments. Traditional endowments tend to have an insurance element linked to the structure, usually in the form of life insurance. They are less flexible in that you don’t have control over the underlying investment and may be charged fees or penalties when changing the contribution amount or withdrawing early.  New-generation endowments tend to be more flexible and give you choice over the underlying investment portfolio.

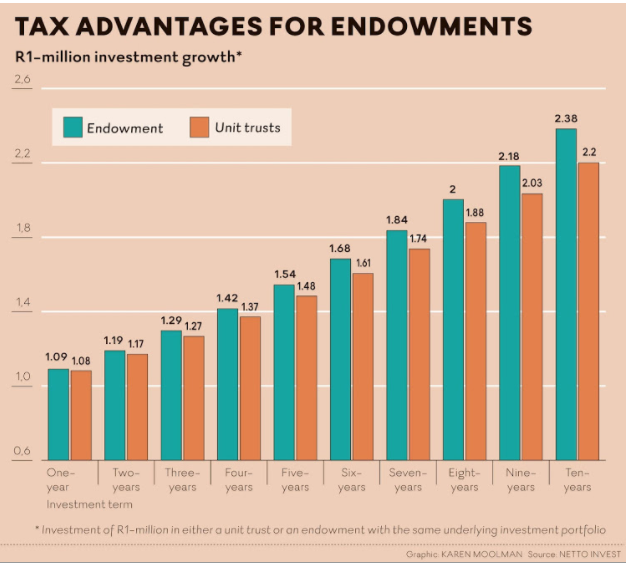

There are no asset class restrictions on endowments (unlike retirement funds investments). This means that you are free to invest in any allocation of equities, bonds, property and cash (including the offshore version of each). Endowments present valuable tax arbitrage opportunities. Tax on income is levied at a flat rate of 30% within the endowment. This is attractive when you compare it to the 45% applicable to investors in the highest tax bracket. Capital gains tax is levied within endowments and varies according to the legal nature of the owner. Within an endowment, investors in the top tax bracket will pay capital gains tax at an effective rate of 12% (40% inclusion rate multiplied by 30% tax within the endowment). In a unit trust, the same investor could pay an effective rate of 18% on capital gains (40% inclusion rate multiplied by 45% marginal tax rate). If you are an individual with a tax rate of less than 30%, investing in endowments for tax reasons alone, probably does not make sense. Endowments can also be a useful estate planning tool as they allow you to nominate beneficiaries The tax arbitrage opportunities within an endowment can be explained by comparing the after-tax return to that of a unit trust. Assume Steve is in the top tax bracket and under the age of 65. He has already used the interest exemptions (R23,800) and capital gains tax exemptions (R40,000). Steve has the choice to invest R1m in either a unit trust or an endowment with the same underlying investment portfolio. The investment is in a typical balanced fund with a blend of asset classes returning 10.8% over the period. At the end of the 10-year term the endowment will be worth R2,383,048 and the unit trust will be worth R2,788,673. However, in the unit trust, the tax on the interest (payable annually) and capital gains tax on withdrawal at the end of the term amount to R587,806 and reduces the proceeds to R2,200,867. The after-tax return of the endowment beats the after-tax return of the unit trust by 0.86% over the period. Steve would be better off opting for the endowment. Endowments can also be a useful estate planning tool as they allow you to nominate beneficiaries. That is, a nominated person can receive direct ownership of, or payment from, your endowment in the event of your death. This means that the beneficiary receives the value of the endowment without having to wait for the estate to be wound up first. What’s more, no executor fees (which can be as high as 3.99%) are charged on the value of endowments received by beneficiaries. There are some other subtle-ties to bear in mind. An endowment is a long-term investment vehicle by nature, with the minimum investment term being five years. It is possible to access some funds before the five-year period in the event of an emergency, but there are limits imposed as to how much you can withdraw. If you are unsure whether an endowment is appropriate for your circumstances contact our Financial advisor, please contact Kevin or Ray, email: invest@daberistic.com tel no: (011 658-1333) Source: Businesslive

0 Comments

Leave a Reply. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|