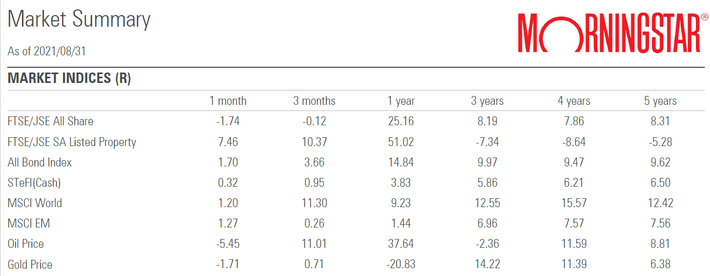

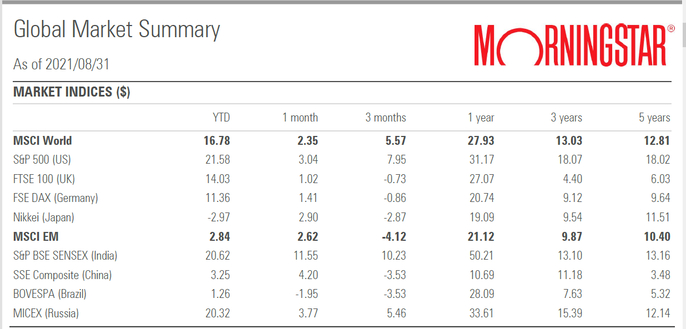

South African Market Commentary Global equity markets performed strongly in August, with many major global equity indices reaching new highs during the month, despite continued concerns around the spread of the highly contagious Covid-19 Delta variant across the globe. The US Federal Reserve (Fed) continued to allay fears of interest rate increases, with Fed Chair Jerome Powell reiterating his cautious stance at the Jackson Hole Economic Symposium held towards the end of August. Powell did concede, however, that the tapering of bond purchases is likely to start at the end of 2021. Powell’s dovish comments, as well as strong earnings updates from corporates, drove US equities to new highs, with the S&P 500 recording a seventh consecutive month of positive returns, its longest winning stretch since 2018. South African equities ended the month lower, as weak performance from Resource counters, as well as large index constituents Naspers and Prosus, weighed on the performance of the local equity index. Local bonds ended the month higher, as long dated nominal bonds delivered strong performance during the month and the nominal curve continued to flatten during August. Local listed property rebounded sharply in August, as sentiment towards the sector improved on the back of the move to an adjusted level 3 lockdown on 26 July and many REITs reporting better than expected recoveries from the riot damage caused by the civil unrest in July. The rand was stronger against most of the major developed market currencies, despite trading in quite a wide range during the month, in line with changes in global sentiment towards emerging market currencies. In terms of the Covid-19 response, the country remained on an adjusted level 3 lockdown, despite a decrease in the number of daily recorded infections during the month. Registration and vaccination for 18-34-year-olds opened on 20 August, with 12.6 million vaccines having been administered by the end of August. SA headline CPI moved lower to 4.6% year-on-year for July (from 4.9% in June), as fuel inflation continued to moderate, and SA inflation remained relatively muted due to weak pricing power in the local economy. SA’s trade balance came in at a surplus for August (R37 billion), following a revised surplus for July of R54 billion, as exports declined 11% month-on-month to R145 billion, higher than the 1% month-on-month decline in imports. StatSA’s periodic rebasing and reweighting of the national accounts data showed that the nominal size of the economy has increased by 11% from previous estimates, resulting in a lower-than-expected fiscal deficit and debt to GDP (71% at the end of 2020 compared with the previous estimate of 79%). Click here to read more  Global Market Summary Developed market (DM) equities had another good month, led by the major US Indices. The S&P500 and the Nasdaq reached record highs over the month with the former managing to close in the green for a seventh consecutive month. Economic data was supportive for the Financials sector at the beginning of the month as the 10-year US Treasuries rose on the back of a better than expected payrolls print. Despite a weaker than expected retail sales print and a resurgence in Covid-19 cases as a result of the Delta variant, markets still managed to power ahead on the back of bullish remarks from Fed chair Jerome Powell at the Jackson Hole symposium. Although Powell raised the possibility of tapering this year, he also highlighted that this should not be viewed as the start of the hiking cycle. He also reinforced the fact that the Fed would continue to tolerate higher inflation in pursuit of further labour market gains which served as support for the markets over the month. Click here to read more

0 Comments

Leave a Reply. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|