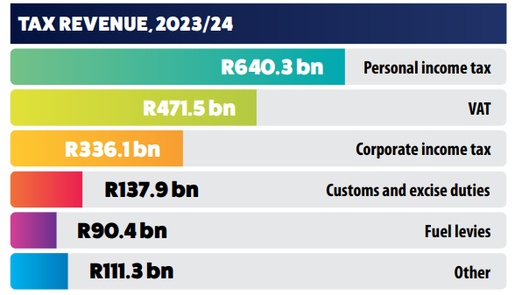

Where The Tax Comes From Highlights Of The BudgetSome of the things that stood out was incentivisation of rooftop solar, energy support packages as well as relief in terms of personal income tax. Energy support package

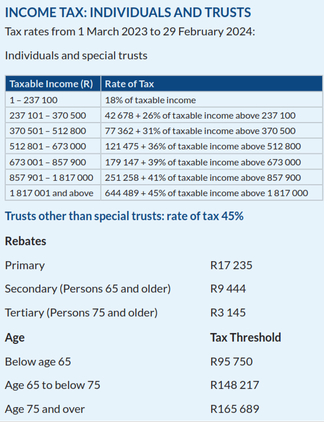

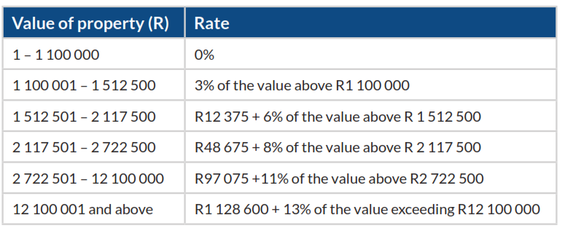

Income Tax - Individuals & Trusts Dividends: Dividends received by individuals from South African companies are generally exempt from income tax, but dividends tax, at a rate of 20%, is withheld by the entities paying the dividends to the individuals. Interest: A final tax at a rate of 15%, is imposed on interest from a South African source, payable to non-residents. Interest is exempt if payable by any sphere of the South African government, a bank, or if the debt is listed on a recognised exchange. Capital Gains Tax: Maximum effective rate of tax: Individuals and special trusts 18%, Companies 21.6%, Other trusts 36% Travelling allowance: Rates per kilometer, which may be used in determining the allowable deduction for business travel against an allowance or advance where actual costs are not claimed, are determined using the table published on the SARS Click here to view Transfer Duty: Transfer duty is payable at the following rates on transactions that are not subject to VAT: Acquisition of property by all persons:  Income Tax - Companies1. Small Business Corporations Taxable Income Rate of Tax 1 – 95 750 0% of taxable income 95 751 – 365 000 7% of taxable income above 95 750 365 001 – 550 000 18 848 + 21% of taxable income above 365 000 550 001 and above 57 698 + 27% of the amount above 550 000 2.Turnover for Tax For Micro Business Taxable turnover (R) Rate of tax (R) 1 – 335 000 0% of taxable turnover 335 001 – 500 000 1% of taxable turnover above 335 000 500 001 – 750 000 1 650 + 2% of taxable turnover above 500 000 750 001 and above 6 650 + 3% of taxable turnover above 750 000 Other Taxes, Duties and LeviesValue-added Tax (VAT): VAT is levied at the standard rate of 15% on the supply of goods and services by registered vendors. A vendor making taxable supplies of more than R1 million per annum must register for VAT. A vendor making taxable supplies of more than R50 000, but not more than R1 million per annum, may apply for voluntary registration. Certain supplies are subject to a zero rate, or are exempt from VAT. Estate Duty: Estate duty is levied on the property of residents and the South African property of non-residents, less allowable deductions. The duty is levied on the dutiable value of an estate, at a rate of 20%, on the first R30 million, and at a rate of 25% above R30 million. A basic deduction of R3.5 million is allowed in the determination of an estate’s liability for estate duty, as well as deductions for liabilities, bequests to public benefit organisations, and property accruing to surviving spouses. Donations Tax: Donations tax is levied at a flat rate of 20% on the cumulative value of property donated since 1 March 2018, not exceeding R30 million, and at a rate of 25% on the cumulative value of property donated since 1 March 2018 exceeding R30 million. The first R100 000 of property donated in each year by a natural person is exempt from donations tax. Securities Transfer Tax: The tax is imposed at a rate of 0.25 % on the transfer of listed or unlisted securities. Securities consist of shares in companies or member’s interests in close corporations. Tax on International Air Travel: R190 per passenger departing on international flights, excluding flights to Botswana, eSwatini, Lesotho and Namibia, in which case the tax is R100. Skills Development Levy: A skills development levy is payable by employers at a rate of 1% of the total remuneration paid to employees. Employers paying an annual remuneration of less than R500 000 are exempt from paying skills development levies. Unemployment Insurance Contributions: Unemployment insurance contributions are payable monthly by employers, on the basis of a contribution of 1% by employers and 1% by employees, based on the employees’ remuneration below a certain amount. Employers not registered for PAYE or SDL must pay the contributions to the Unemployment Insurance Commissioner. GrantsUpdated increases in social grants are as follows:

0 Comments

Leave a Reply. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|