The end of February is the end of the tax year. Carla Rossouw explains why this is a good time to take maximum advantage of the incentives the government has put in place to encourage us to save.

There are certain annual tax benefits available for you through your retirement fund and tax-free investment (TFI) account. You forfeit these if you don't act each year. As we approach the end of the tax year (28 February), it is worthwhile looking at your finances. If you have cash to spare, consider taking full advantage of the tax incentives. Individuals are allowed to invest R33 000 per year up to a lifetime maximum of R500 000 in a TFI account. Like a retirement fund, you benefit from growth free of dividends tax, income tax on interest and capital gains tax - a big win if you invest for the long term. In terms of flexibility, TFIs are similar to unit trust investments, but your return potential is higher than in a basic unit trust, as you can see in Graph 1, which shows the impact of tax over 10 years. The red line illustrates the 10-year return of the Balanced Fund, while the black line reflects the return an investor would receive after tax - although of course this differs for everyone as it is based on your personal tax rate and circumstances. The catch is that if you exceed the maximum investment amount in a TFI, the tax penalties are high. To top up or open up a Tax Free Savings account , please contact Kevin or Ray, email: invest@daberistic.com tel no: (011 658-1333) Source: Allan Gray

0 Comments

What is the fund’s objective? The Fund aims to outperform global stock markets over the long term, without taking on greater risk. Its benchmark is the FTSE World Index, including income.

How Allan Gray aims to achieve the Fund’s objective? The Fund invests only in the Orbis Global Equity Fund. The Orbis Global Equity Fund is managed to remain fully invested in selected global equities. Orbis uses in-house research to identify companies around the world whose shares can be purchased for less than Orbis’ assessment of their long-term intrinsic value. This long-term perspective enables Orbis to buy shares which are shunned by the stock market because of their unexciting or poor short-term prospects, but which are relatively attractively priced if one looks to the long term. This is the same approach as that used by Allan Gray to invest in South African equities, except that Orbis is able to choose from many more shares, listed internationally. Suitable for those investors who • Seek exposure to diversified international equities to provide long-term capital • growth • Wish to invest in international assets without having to personally expatriate rands • Are comfortable with global stock market and currency fluctuation and risk of • capital loss • Typically have an investment horizon of more than five years • Wish to use the Fund as a fully invested global equity ‘building block’ in a • diversified multi-asset class portfolio To invest in Coronation Fund, please contact Kevin or Ray, email: invest@daberistic.com tel no: (011 658-1333) Source: Allan Gray  Allan Gray launched an umbrella retirement fund in March, adding another player to the increasingly competitive retirement market space.

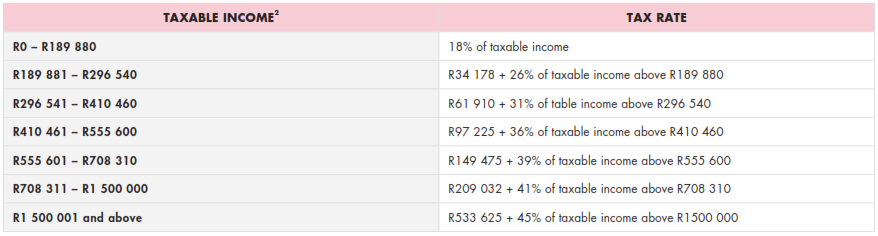

Umbrella retirement funds are funds that serve multiple employers, unlike traditional stand-alone employer-sponsored funds. More and more employers are going the umbrella route, largely because of the increasing burden of administering a retirement fund and having to comply with burgeoning regulation. Saleem Sonday, the head of group savings and investments at Allan Gray, says the South African retirement industry today (excluding the government pension fund) manages assets of around R1.8 trillion. Of this, around 49 percent is in non-commercial funds, 17 percent in commercial umbrella funds and about 34 percent in individual retirement annuity accounts and preservation funds. Over the last four years, the market share of commercial umbrella funds has increased by 70 percent, according to Credit Suisse, at the expense of stand-alone employer funds. “This should be a good thing. Since an umbrella fund clubs together multiple employers and its employees in a single fund with standardised rules and a single board of trustees, it is more efficient to govern and administer than a stand-alone employer fund,” Sonday says. The commercial umbrella fund market is dominated by the large life companies, which make up 85% of the market. “Although there are some funds that offer super-efficient administration and simple products that sell themselves, mostly umbrella funds today have a reputation for high costs, poor transparency and complexity. “We think this is an industry that could do with more competition. A new entrant using technology to provide better service than the incumbents at a competitive and more transparent price could win over clients,” Sonday says“The recently-launched Allan Gray Umbrella Retirement Fund aims to give employers and members a transparent and easy-to-understand retirement saving solution. It has a simple product and fee structure, which means that employers and their employees have clear sight of contributions, returns and charges. “Members benefit from superior service, competitive administration and investment management fees and there are no hidden costs,” he says. “The product makes things simple for employers and puts member needs at the centre by offering an unbiased, limited range of high-quality investment managers, fair and transparent pricing and great service.” If you would like to get a quote for an Umbrella Fund, please contact Kevin or Thato, email: invest@daberistic.com tel no: (011 658-1333) Source: Allan Gray  INCOME TAX Individuals and special trusts A new top bracket has been introduced for personal income tax - individuals’ taxable income above R1.5 million per year will be taxed at 45%. Previously, the top bracket of 41% was set at R701 301. The new top marginal income tax bracket is accompanied by partial relief for bracket creep 1. The personal income tax rates for the 2017/2018 tax year are listed below.  Companies and trusts

TAX RATE The income tax rate for companies has remained unchanged at 28%, while the income tax rate for trusts (other than special trusts) has increased to 45%. TAX THRESHOLDS Tax thresholds have increased to: „„ R75 750 for taxpayers younger than 65 „„ R117 300 for taxpayers aged 65 to below 75 „„ R131 150 for taxpayers aged 75 and older REBATES The primary rebate (deductible from tax payable) has increased to R13 635 per year for all individuals. The secondary and tertiary rebates have increased to: „„ R7 479 for taxpayers aged 65 and older „„ R2 493 for taxpayers aged 75 and older INTEREST EXEMPTIONS Interest exemptions have remained unchanged at: „„ R23 800 per annum for individuals younger than 65 years „„ R34 500 per annum for individuals 65 years and older MEDICAL TAX CREDITS Monthly tax credits for medical scheme contributions will increase from: 1.R286 to R303 per month for the person who pays the contributions and the first dependant on the medical scheme 2.R192 to R204 per month for each additional dependant Bracket creep occurs when the income tax tables are not fully adjusted for inflation, and inflationary salary adjustments increase an individuals’ effective tax rate, reducing real income. As the increases to taxable income brackets, the tax thresholds, and the rebates are below the expected level of inflation, taxpayers will face a real increase in their effective personal income tax rate in 2017/2018. INTEREST WITHHOLDING TAX (IWT) AND DIVIDEND WITHHOLDING TAX (DWT) Interest Withholding Tax (IWT) on interest from a South African source payable to non-residents has remained unchanged at 15%. Interest is exempt if payable by any sphere of the South African government, a bank or if the debt is listed on a recognised exchange. Dividend Withholding Tax (DWT) on dividends paid by resident companies and by non-resident companies for shares listed on the JSE has increased from 15% to 20%, effective 22 February 2017. The exemption and rates for inbound foreign dividends have also been adjusted in line with the new local DWT rate, resulting in a maximum effective rate of 20%. TAX-FREE SAVINGS ACCOUNTS The annual limit on contributions to tax-free savings accounts has increased from R30 000 to R33 000. RETIREMENT LUMP SUM TAXATION At retirement: The retirement lump sum tax table is unchanged. The table below illustrates how retirement lump sums will be taxed. Click to read more If you have any queries on your personal or business tax, contact our Finance Department, email finance@daberistic.com, tel (011)658-1333 Source: Allan Gray At various stages of one’s life, financial needs may differ. For this reason it is important to change financial strategies and instruments used to fulfill those needs. The investment behaviour of women differs to that of men. Women often feel comfortable with “secure” and “predictable” investments, explained Christelle Louw, advisory partner at Citadel. “The problem is that these investments mostly do not offer the required performance after inflation and tax to achieve their financial goals,” she said.

For this reason, equities are becoming an important element to include in their portfolios. This is also true as women become more sophisticated investors, with surplus income to invest. Over the past few years women have been playing a bigger and more prominent role in business and their earnings are increasing. This is contributing to their empowerment. The global income of women will grow from $13trn to $18trn over the next five years worldwide, according to the CFA Institute. Women are also living longer than men. According to the World Health Organisation's 2015 data for global life expectancy, women will live five years longer than men. More women are seeing the need for inflation-beating investments to sustain their lives once their partners are gone. “It is important to ensure that they have made financial provision beyond the life expectancy of their husband or male partner,” said Louw. Click to read more To review your investments and to ensure they still meet your needs, please contact Kevin or Thato, email: invest@daberistic.com telephone: (011)658-1333 Source: Fin24 What is it?

Tax Free Investments were introduced as an incentive to encourage household savings. This incentive is available from 1 March 2015. How will it work? The tax free investments may only be provided by a licenced bank, long-term insurers, a manager of registered collective schemes (with certain exceptions), the National Government, a mutual bank and a co-operative bank. Service providers must be designated by the Minister in the Gazette. As per the current Regulation, only the above are designated. This is how it will work:

Around this time of the year, we would like to remind you to consider topping up your retirement annuity fund. According to the current legislation, you may contribute up to 27.5% of your taxable income (strictly speaking, non-retirement funding income) to a retirement annuity fund and enjoy tax deductions. As 28 February is the end of the tax year, you must calculate and pay the additional amount to your retirement annuity prior to this date, in order to qualify for tax deductions and tax refunds.

Below is an example of topping up your retirement annuity: Mr Jackson has a monthly salary of R50, 000. In December he received a bonus of R100, 000. Every month he contributes R3, 000 to a personal retirement annuity fund. His annual income is then R50, 000*12 + R100,000 = R700,000. The maximum tax-deductible contribution to retirement annuity is R700, 000 * 27.5% = R192,500. Over the year he has contributed the following to a retirement annuity fund: R3, 000 * 12 = R36,000 The additional amount he may top up in his retirement annuity (RA) is R192,500 Less R36,000 R156,500 He can expect a tax refund of R156, 500*39% = R61, 035 from his additional retirement annuity contributions. Should you require assistance to calculate the retirement annuity top-up amount, please contact your accountant or financial advisor, or speak to Koketso on tel 011-658-133, email office@daberistic.com. Source: Kevin Yeh |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|