The Health Plan Protector – ensuring your family’s healthcare costs are taken care of. The Health Plan Protector will cover your family’s monthly health plan contributions for a period of five or 10 years upon a valid claim. The benefit amount will increase each year in line with the medical scheme contribution increases, up to a maximum of 20% per year.

You may choose to cover yourself for death, disability and severe illness, or disability and severe illness, or death only. You also have the option to cover both yourself and your spouse. Every year we will calculate your unused health risk contributions by considering your medical scheme risk contributions and medical scheme risk claims over the previous year. These savings will be accumulated and a portion will be paid back to you, through either the Health Dividends or the Health Fund mechanism – depending on which option you choose. Health Dividends Allows you to receive up to 20% of your unused health risk contributions back every year, depending on your Vitality status, the number of years you have been a member of Discovery Vitality and whether you have a Discovery Card. The Health Fund Each year, your unused health risk contributions will be transferred into the Health Fund. Every five years, you can get up to 30% of your Health Fund back through the PayBack benefit, depending on your Vitality status. When you turn 65 or experience a lifechanging event, we will pay you the balance of your Health Fund. Request for a quote for your Health Protector Plan, please contact Kevin or Thato in our Life Department, email life@daberistic.com tel (011)658-1333 Source: Discovery

0 Comments

Do you think of yourself as a healthy person? If you exercise a few times a week, make mostly positive eating choices, and rarely become seriously ill, you might well consider yourself to be. In fact, the thought of contracting a severe illness has most likely never entered your mind. Until you arrive at work one day to find out that an apparently healthy colleague of the same age as you has just been diagnosed with cancer. And then the realisation hits. There's a chance it could just as easily have happened to you.

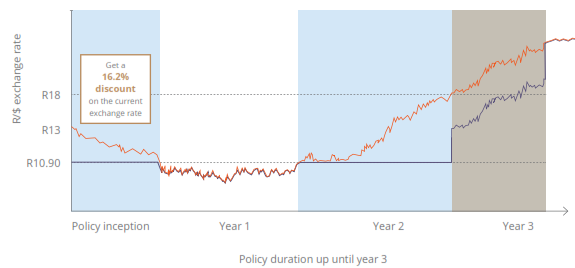

Suddenly you start to consider the possibility that a severe illness could become a reality in your own life. And that protecting yourself and your family against the risk of an illness is more than a nice-to-have it's a must-have in every way. Do I really need severe illness cover? It's a good question and if you're relatively young and in good health, you may think the answer to be a resounding no. But for a more accurate assessment of your potential risk factors, a look at actual statistics might help shed some valuable light. Over the past year, the severe illness claims paid out to Discovery Life clients have painted an interesting picture: On average, 38% of claimants in 2015 were female, while the majority of 62% were male. Of the claims made, a full 51% paid out to females were for cancer-related diseases, compared to 31% for men. While claims made for body systems such as gastrointestinal, ear nose and throat, respiratory, eye and musculoskeletal tended to be evenly paid out between genders, a total of 35% of claims made by men were due to heart and artery conditions, compared to just 8% for women. Finally, claimants between the ages of 41 and 60 were by far in the majority, representing 61% of claims made in 2015, with claimants from 26 to 40 representing only 16%. What these figures clearly indicate is that no matter your gender, age or health profile, severe illness cover always needs to be a priority not for you, then for the continued well-being and support of your family. Cover for severe illness When choosing your level of cover you should consider any outstanding debt and other liabilities that you would have to settle if you were to become severely ill. It is also important to consider the cost of modifications or lifestyle changes that would be required as a result of a severe illness. Please contact Kevin or Thato in our Life Department, email life@daberistic.com, tel (011)658-1333 to get a quote and more information on Severe Illness cover Source: Discovery  The R10.90/$1 Life Plan special offer allows clients to pay a guaranteed exchange rate of R10.90/$1 on their Dollar Life Plan for three years! Clients can pay a guaranteed exchange rate of R10.90/$1 on their Dollar Life Plan for three years, and if the exchange rate exceeds R18/$1, a 20% discount on the exchange rate will apply. This offer ends on 31 August 2017. As part of the limited offer, clients are able to pay premiums for a new Dollar Life Plan based on a maximum exchange rate of R10.90/$1 for the first three years of their policy, as long as the R/$ exchange rate is less than R18/$1. This amounts to an exchange rate of up to 39% better than the market exchange rate. If the R/$ exchange rate is higher than or equal to R18/$1 during the first three years of their policy, Dollar Life Plan clients are still able to pay premiums based on an exchange rate that is up to 20% better than the market. If the exchange rate drops below R10.90/$, normal market rates will apply. To sign up for this awesome limited offer, please contact Kevin or Thato, email: invest@daberistic.com tel no: (011 658-1333) Illustration of the preferential exchange rate for Dollar Life Plan clients  Here are useful guidelines when making a complaint to an insurance company in order to try to resolve the complaint before going to the Ombudsman:

* It is usually best to complain in writing. But if you phone, ask for the name of the person to whom you speak, as well as the reference number for the call. Keep a note of this information, with details such as the date and time of your call and what was said. With the smartphone technology available nowadays, you may also make a recording of the telephone call. This may be required at a later stage. * Remain calm and polite, however emotional, angry or upset you may be. You are more likely to explain your complaint clearly and effectively if you can stay calm. * Initially attempt to contact the person with whom you originally dealt. If he/she cannot help, indicate that the matter will be taken further. Seek details of the insurer’s complaints procedure. Attempt to take up the matter with a senior official at the insurer. * When you write a letter of complaint, set out the facts as clearly as possible. * Write down the facts in a logical order and stick to what is relevant. Include important details such as your claim number or your policy number. * Keep copies of any letters between you and the insurer. This may be in the form of email, electronic documents, scanned copies or hard copy. It is trite law that a person can nominate a minor as a beneficiary on a life insurance policy. Remember, the minor will not be regarded as a party to the contract (i.e. the policy) between the policyholder and the insurer.

The issue of contractual capacity, which is required for a contract to be considered valid and binding in South Africa, thus doesn’t come into play. Contractual capacity refers to the legal capacity of an individual to enter into valid agreements. The true nature of a beneficiary nomination on a life insurance policy is that of a stipulatio alteri. The common law principle of stipulatio alteri refers to a contract between two persons, but for the benefit of another. The policyholder contracts with an insurer for the policy proceeds to be paid by the insurer to a third party, i.e. the nominated beneficiary. When you take out a life policy, you will be asked to nominate a beneficiary. The policyholder is of course not compelled to nominate a beneficiary – he/she has the right to nominate a beneficiary. If no beneficiaries have been nominated, the proceeds of the policy will be paid to the deceased estate upon the death of the policyholder. The obvious benefit to nominating a beneficiary is to thereby exclude the proceeds of the policy from the deceased estate (which means no executor’s fee will be payable on the benefit). The problems with nominating a minor It is common for parents to nominate their children as beneficiaries on policies – which children are often minors at the time of death. In the above instance the proceeds of the policy will (usually) be paid to the minor’s guardian. The problem with this is that the proceeds might never reach the minor for whom it was intended. Consider the situation where the parents are divorced. The proceeds will be paid to the ex-spouse (assuming he/she is the minor’s guardian) and could end up being utilised for other things – which is exactly what the policyholder wanted to avoid by nominating the minor child as the beneficiary and not his/her ex-spouse.Another problem would be where there is more than one guardian. The Children’s Act No 38 of 2005 defines a “guardian” as “a parent or other person who has guardianship of a child”. In a culture as diverse as ours it is thus possible for a minor to have more than one guardian at the time of death of the policyholder. In terms of section 18(4) of the Children’s Act each of the persons qualifying as the minor’s “guardian” would be competent to act independently and without the consent of the other. Another problem is where the minor doesn’t have a legal guardian (or no legal guardian has been appointed yet). In such an instance the proceeds will have to be paid to the Guardian’s Fund until the minor reaches the age of majority. In terms of the Children’s Act 38 of 2005 the age of majority is 18 years.Click to read more Please contact Kevin and Thato in our Life Department; email life@daberistic.com , to get your personalised quote for your Life policy. Source: Glacier The Discovery Dollar Capital Plus Fund

Discovery Invest has just introduced a new structured fund, the Discovery Dollar Capital Plus Fund, which provides investors with exposure to the performance of the US and European equity markets in US Dollars. The Discovery Dollar Capital Plus Fund is based on a global portfolio comprising 30% S&P 500 and 70% Eurostoxx 50 indices, with a minimum return in US Dollars of 40%, if the return of the global portfolio is flat or positive at the end of five years. Some capital protection in US Dollars is provided for falls in the global portfolio of up to 30% during the five-year term. The Discovery Dollar Capital Plus Fund opened on Monday, 22 February 2016. This offer will expire when capacity runs out but will not be available later than 8 April 2016. Please see the Discovery Dollar Capital Plus Fund Factsheet for more information on this special offer. If you are interested in investing in this special offer, please speak to Kevin Yeh or Thato Merementsi to apply, email invest@daberistic.com, Tel 011-658-1333 or 083-633-4671. Introducing the R12/$1 Life Plan Limited Offer! Buy a Dollar Life Plan policy before 31 March 2016, and get a guaranteed exchange rate of R12/$1 on your premium for the next three years! In November 2014, Discovery Life launched the Dollar Life Plan, a first-to-market offshore life insurance policy that offers clients comprehensive risk protection in US dollars. With the Dollar Life Plan, clients can be sure that their risk protection will remain relevant in the long term, regardless of their changing lifestyle needs. Why offshore life insurance makes sense: 1. Sound long-term financial planning With an offshore life insurance policy, denominated in US dollars, clients are protected against the financial impact of a life-changing event – no matter where they may find themselves in the future. 2. Matching liabilities Many clients either have, or could in the future have, offshore liabilities such as a bond, children’s education costs or estate duty in a foreign country. Clients may also be impacted by a fluctuating rand, which typically results in an increase in the cost of goods and services available locally. Risk protection denominated in dollars is therefore critical to ensure that a client’s liabilities are fully matched. 3. Diversification Discovery Life provides an efficient vehicle for clients to supplement and diversify their retirement savings into offshore markets by allowing them to convert their future health and wellness into a tangible offshore financial asset. Clients can further supplement their retirement savings in dollars through three unique features:

The minimum premium on the Dollar Life Plan has been reduced to $50 per month. This allows more clients to access the benefits of an offshore life insurance policy. You can increase the value of the rand with future certainty! For a limited time only, you will be able to pay the premiums on a new Dollar Life Plan at a substantially lower exchange rate than the market. You will be charged a premium based on a maximum exchange of R12/$1 for the first three years of their policy. This is provided that the exchange rate remains less than R20/$1 And if the exchange rate is higher than (or equal to) R20/$1, you will be charged a premium based on an exchange rate that is 20% less than the rest of the market. For more information, refer to this brochure and limited offer technical document. If you are interested in investing in this special offer, please speak to Kevin Yeh or Thato Merementsi to apply, email invest@daberistic.com, Tel 011-658-1333 or 083-633-4671. Source: Discovery Introducing the R12/$1 Life Plan Limited Offer! If you buy a Dollar Life Plan policy before 31 March 2016, you can get a guaranteed exchange rate of R12/$1 on their premium for the next three years! In November 2014, Discovery Life launched the Dollar Life Plan, a first-to-market offshore life insurance policy that offers clients comprehensive risk protection in US dollars. With the Dollar Life Plan, clients can be sure that their risk protection will remain relevant in the long term, regardless of their changing lifestyle needs. Why offshore life insurance makes sense: 1. Sound long-term financial planning : With an offshore life insurance policy, denominated in US dollars, clients are protected against the financial impact of a life-changing event – no matter where they may find themselves in the future. 2. Matching liabilities : Many clients either have, or could in the future have, offshore liabilities such as a bond, children’s education costs or estate duty in a foreign country. Clients may also be impacted by a fluctuating rand, which typically results in an increase in the cost of goods and services available locally. Risk protection denominated in dollars is therefore critical to ensure that a client’s liabilities are fully matched. 3. Diversification : Discovery Life provides an efficient vehicle for clients to supplement and diversify their retirement savings into offshore markets by allowing them to convert their future health and wellness into a tangible offshore financial asset. Clients can further supplement their retirement savings in dollars through three unique features:

You can increase the value of their rand with future certainty! For a limited time only, clients will be able to pay the premiums on a new Dollar Life Plan at a substantially lower exchange rate than the market. Clients will charged a premium based on a maximum exchange of R12/$1 for the first three years of their policy. This is provided that the exchange rate remains less than R20/$1 and if the exchange rate is higher than (or equal to) R20/$1, clients will be charged a premium based on an exchange rate that is 20% less than the rest of the market. Click here for full brochure Source: Discovery |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|