Discovery announced a number of key product enhancements that respond specifically to insurance needs around COVID-19, as well as the results of two critical research papers on COVID-19 in South Africa.

Hylton Kallner, Discovery South Africa CEO says, “Our response to the COVID-19 pandemic has been guided by our core purpose of making people healthier. In the context of this pandemic, it is more critical than ever that we work hard every day to support clients with access to healthcare cover and comprehensive financial protection, and that we provide them with the necessary tools to promote behaviour that encourages healthy lifestyle choices.” The Group earlier introduced healthcare cover specific to COVID-19 through the WHO Global Outbreak benefit and tailored Vitality to help encourage people to stay healthy and active at home. In partnership with Vodacom, the Group made online doctor consultations available to South Africans through a virtual healthcare platform that gives free access to reliable information, risk screening and the ability to effectively ‘dial a doctor’ from the safety of their home. Kallner explains, “Discovery has access to one of the largest population data sets on a variety of factors relevant to the COVID-19 experience. Ranging from clinical, to financial and behavioural data, we are in a unique position to understand the long-term impact of COVID-19 in South Africa, and to design the necessary product structures to better support clients.” Together with emerging experience from other parts of the world, Discovery data highlights the importance of regular screening, appropriate testing and understanding and managing an individual’s health risk. This has informed the expansion of new benefits in response to changes brought about by COVID-19. These provide clients with proactive risk monitoring and assistance; providing cover for different severe illness outcomes due to COVID-19; adequate health protection over a longer term; and rewards that adapt to new lifestyles. A new COVID-19 risk assessment tool to be made available to all South Africans “We have undertaken the analysis to create an accessible COVID-19 risk assessment tool, that will be released on the Discovery app and the website helping people to understand their risk for COVID-19, to know their health risks that increase the likelihood of hospitalisation, and access funding for testing and health monitoring for those at a high risk for compilations,” says Kallner. The assessment will look at a member’s risks compared with that of the membership base in an area. “Members will be able to complete the assessment over time and keep track of their history. When testing is recommended, the assessment tool guides them to an online doctor consultation in a network. More than 6 500 members of Discovery Health Medical Scheme (DHMS) have consulted with their doctors online over the past couple of months, helping to contain the spread of the virus,” he says. “What we know now is that high blood pressure, cholesterol, blood glucose and body mass index are leading risk indicators of developing complications. We want to help members on all health plans to understand and manage these factors to mitigate the risk of complications from COVID-19. From June, any result from a Vitality Health Check that places someone at a high risk for complications will trigger a referral for advice through one online doctor or nurse consultation in the network, which the Scheme will fund in full,” says Kallner. In addition to the forthcoming COVID-19 risk assessment tool, other key enhancements announced by the Group include: Discovery Health expands access to fully funded COVID-19 testing and high-risk monitoring The WHO Outbreak benefit, first announced in early March, has been enhanced further to provide comprehensive cover for COVID-19 over the longer term. It now provides cover for two PCR tests for each beneficiary in a year, following screening by a healthcare professional and will be funded from the risk benefit regardless of the result. Healthcare professionals who are members of DHMS, will have cover for four PCR tests in a year. Discovery Health will assist members at higher risk of COVID-19 complications with funded telephonic consultations with a wellness specialist to monitor their current physical and mental wellbeing and make referrals to virtual healthcare services. DHMS will fund a pulse oximeter– used to monitor oxygen saturation from an early stage – for members at high risk of COVID-19 complications. This will be funded in full if obtained from a network provider. Members will also have access to three consultations with a wellness consultant to monitor oxygen and make a referral to a GP when necessary. Employer groups also have access to a variety of benefits that can help to manage COVID19 in the workplace. A comprehensive information hub, management of high-risk employees, contact tracing and access to screening and online doctor consultations are all available to employers through Discovery Healthy Company. Discovery Insure rewards clients for driving less Premium cash back even when driving shorter distances through the Dynamic Distance cash back that rewards low kilometres. Clients can earn up to 25% motor premium cash back every month when they drive between 0km and 249km in a month and they can still earn up to 50% fuel cash back when they drive more. Vitality Drive Active Rewards has been enhanced so that a client’s drive goal each week is based on their driving behaviour and not on the number of kilometres driven. Discovery Vitality tailored for seniors Vitality Health Check tailored for people aged 65 years and older, recommending specific and age-appropriate health screenings, preventive tests and vaccinations, including a risk assessment score for COVID-19. Three clinically validated screening tests help with early detection of age-related risks of hearing loss, visual perception, and balance and leg strength to prevent injuries from falling. The standard set of preventive tests follow, which include blood pressure, blood glucose, cholesterol, weight and smoking status. The acceptable ranges for weight and blood pressure are altered to consider the changes at an older age. Preventive steps include recommended vaccines such as the flu vaccine and the pneumococcal vaccine to prevent pneumonia. Results are summarised in reports and provide targeted health tracking, clinical risk projections and healthcare referrals based on the health assessment. It can be accompanied by a Vitality Functional Assessment which is an eight-part physical assessment to identify the risk of early frailty or disability and offers tailored workout routines to support healthy ageing. Discovery Life enhances Severe Illness Benefit to automatically cover multi-organ complications associated with COVID-19 Clients have full cover for COVID-19 related claims under their Discovery Life cover. A new multi-organ benefit has been included as a category under the Severe Illness Benefit to provide relevant cover for the complications associated with COVID-19. COVID-19 presents varying respiratory, cardiac, renal and liver complications. The multi-organ benefit is a category within the Severe Illness Benefit and complements existing severe illness body systems to provide payments by the level of acute multi-organ failure, resulting in payments of 50% to 100% of the severe illness benefit. Discovery Life is also taking a proactive approach to providing cover and is currently tracking 203 clients who haveCOVID-19 to manage claims from any of their available Life, Severe Illness and Income Continuation Benefits. If you would like more information on any of the products please contact Koketso email: info@daberistic.com tel:(011)658-1333 Source: Discovery

0 Comments

Today is day 20 of the lockdown announced by President Ramaphosa. As we are in the 3rd week of lockdown, many people and businesses are affected, as people are not working and businesses are closed to operations. This leads to lost revenue and income. As a result, individuals and businesses are struggling financially during and beyond the lockdown period. In response to the government's call to action, most financial institutions have announced measures to provide financial relief. As the situation evolves from day to day, financial institutions continue to work with the government to reassess the situation, and further relief measures can be expected.

We have gathered below links to financial relief measures provided by financial institutions, we hope these can assist you during this difficult period. Note that the information may not be complete or the most up to date. Please speak to the bank, the insurance company, your broker or financial advisor to confirm. Banks Covid-19 debt assistance: https://www.nedbank.co.za/content/nedbank/desktop/gt/en/personal/covid-19-debt-relief.html?cmpid=dis:ned:ret:debtrelief:banner:ned Nedbank's relief measures for individual and small-business clients, including information on payment holidays, the newly announced SA Future Trust Fund for SMMEs, and other Nedbank debt relief actions, can be found on https://www.nedbank.co.za/content/nedbank/desktop/gt/en/info/campaigns/nedbank-covid19-page.html Select 'Business' then 'Covid-19 Relief'. Nedbank remains committed to meeting your banking needs through this challenging period. Standard Bank: https://www.standardbank.co.za/southafrica/personal/campaigns/covid-19 FNB: https://www.fnb.co.za/press-office/index.html ABSA: https://www.absa.co.za/personal/covid-19/ Capitec: https://www.capitecbank.co.za/global-one/banking_during_the_covid_19_lockdown/ • If you're worried about your income or your ability to make your Capitec loan repayments, talk to us – we can help. To make a payment arrangement, dial 0860 66 77 18 to speak to an agent Life insurance companies (Do consult your financial advisor on the best option for your personal circumstances) Discovery Life discovery_premium_relief.pdf Option 1 – Premium relief option: Qualification rules: The premium payer must be self-employed, a business owner or an employee of such businesses facing severely reduced income themselves, in an industry that is not an essential service as defined in the Labour Relations Act. This applies to small and medium enterprises (SMEs) that meet the definition of a Small Enterprise in South Africa as per the Department of Small Business Development. The policy must have been in force for at least two years. The client must not have received a credit control letter in the past two years. The policy must have Comprehensive Integration with the PayBack benefit. At the moment, the policy's accumulated Surplus PayBack fund or Five-yearly PayBack fund has at least enough funds for two months’ worth of premiums. Policies that are in claim or have a claim registered that is being assessed do not qualify. Option 2 – Suspended cover option (Cover-pause): Qualification Rules: The premium payer must be self-employed, a business owner or an employee of such businesses facing severely reduced income themselves, in an industry that is not an essential service as defined in the Labour Relations Act. This applies to small and medium enterprises (SMEs) that meet the definition of a Small Enterprise in South Africa as per the Department of Small Business Development. The policy must have been in force for at least six months. The client must not have received a credit control letter in the past six months. Policies that are ceded (given as security for a loan) do not qualify. Policies that are in claim or have had claims submitted do not apply Option 3 – Underwriting-free servicing option: • A completed servicing quote is required (reduction) • Removal of benefits will not form part of the offer when up-servicing after three months, free of underwriting Important: • The form for options 1 and 2 must be completed by the policy owner and sent from his or her email address on record. A policy owner is able to contact the Call Centre, be verified and update their email address – 0860 00 54 33. Old Mutual helping_your_customers_during_lockdown_-_rsa_2.pdf Sanlam Liberty life insurance policies riskpremiumbreak_final_.pdf Investment policies investmentpremiumbreak_1pager_.pdf Momentum momentum_myriad_covid19_ppo_information_leaflet.pdf momentum_myriad_covid19_ppo_faq.pdf PPS pps_option_1.png pps_option_2.png Short-term insurance companies Discovery Insure discovery_premium_relief.pdf Santam Premium relief is only available once a client has lapsed their premium. We support all actions being done with clients to restructure their existing cover and reduce their premiums such that they do not have to lapse their policies.  After you have engaged a financial planner to conduct a comprehensive financial needs analysis, the financial planner should have a subsequent meeting with you, to give you a proposed financial plan and discuss the findings with you. This meeting can be called Strategy Meeting or Recommendations Meeting. So what do you do when you have received the financial plan?

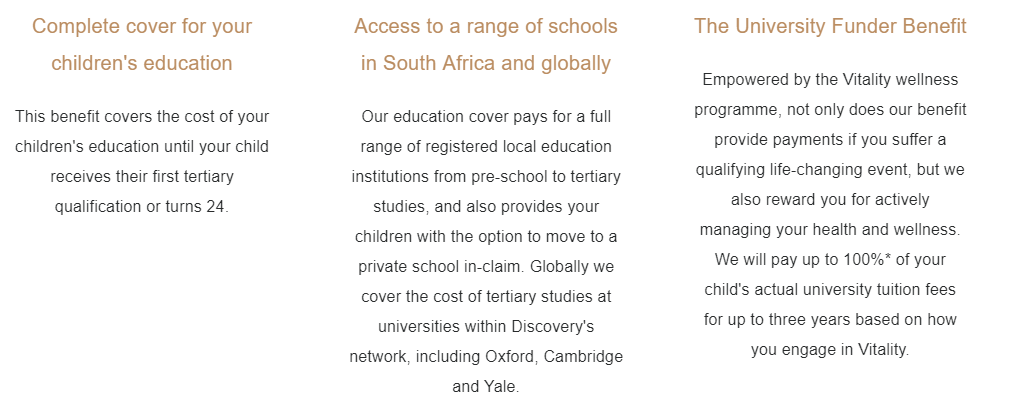

1. You are the co-creator of your financial plan. The financial planner is equipped with the professional knowledge and experience, to craft a financial plan that takes into account your personal circumstances, future inflation rate, investment returns, life expectancy and tax. However, the proposed financial plan is the starting point; this should not be your final plan. The proposed financial plan is what I call the theoretically ideal scenario. In practice you are in charge of the path you want to take. You need to decide what you want to do, how you want to do it, to achieve your financial and lifestyle goals. You give inputs, ask the financial planner to make changes, to get to a financial plan that is workable for you. 2. Ask questions. No questions are stupid questions. A good financial planner is also a good teacher, ready to answer your questions and explain financial concepts, relating to details of your plan, assumptions, terms and conditions, details of the financial solutions proposed to meet your needs. At times these financial jargons and concepts can seem daunting. Don't pretend you understand them if you don't. Ask questions. If a financial planner wants to rush through things, only interested in selling you the financial products he wants you to buy, without explaining to you all the details you would like to know, you should rather walk away. 3. Highlight issues not taken into account in the financial plan. There can be times a financial planner did not consider certain information discussed in the initial meeting, in developing your financial plan. Or you forgot to disclose material information. You should then bring it to the attention of the financial planner, so you can discuss about it, and the financial planner may have to re-work the plan. 4. Think about the implications of the recommendations. The value of a financial plan lies in the ability of the client to execute the plan successfully, over the long term, with the help of a financial planner. You need to think about the action items, whether you can mentally and financially commit to such actions over the long term. Does the plan give you flexibility? If your circumstances change, say you have one more child, or are retrenched, how would it impact your ability to continue with these financial products? Would you lose cover, benefits, or suffer financial penalties and charges? If your financial planner nudges you to be disciplined, would you toe the line? 5. Discuss the plan with the people affected by your plan. You do not live in a vacuum. You do not live alone. You have families and friends in your circle, that are going to be impacted by your financial plan and decisions. Specifically, people that are financially dependent on you, your spouse, children, sibling and maybe even parents. Discuss your financial plan with them, so you can consider their needs and inputs, in amending your financial plan. On the other hand, do not be a slave to your families' every wish. We do need to take care of our parents and siblings in need. However, every person needs to take own responsibility, to be useful and productive. In the Bible, 2 Corinthians 12:14 says, "... After all, children should not have to save up for their parents, but parents for their children." 6. Your are the owner of the financial plan. After you have discussed and finalised the changes to the financial plan with your financial planner, take ownership of the plan. It's your financial plan, not your financial planner's. Use the plan. Implement the plan. From time to time you may have to revisit and make changes to the plan, as your circumstances and needs change. The plan is the roadmap, to take you to your final destination, to realise your dreams and goals. There may be detours along the way, but adapt like our winning Springboks, be steadfast, and you will lift your own Webb Ellis Cup one day!  Discovery will pay your children's education fees when you can't. The Global Education Protector from Discovery helps to cover your children's education from crèche through to tertiary education, locally or abroad, if something happens to you. Cover your child's tertiary education fees by leading a healthy lifestyle If you don't claim and lead a healthy lifestyle with Vitality, you can get up to 100% of your child's tertiary fees funded. The percentage is based on your children's age when you take out the policy and the benefit option you select. Reasons to consider Discovery's Global Education Protector A good education is one of the best gifts you can ever give your children. With Discovery's Global Education Protector Benefit, the education cover will ensure that they'll always be provided for and that their future is bright. All benefit options automatically include cover for:

To get a quote for your Global Education Protection , contact Kevin and Ray in our Life department, email life@daberistic.com , tel (011)658-1333

Source: Discovery  In times of trauma or grief, you and your loved ones should not have to deal with the stress of having a life policy payment rejected or delayed.

In times of trauma or grief, you and your loved ones should not have to deal with the stress of being denied disability benefits or having a life policy payment rejected or delayed. “Ensuring that you are paid when you call on life or disability cover requires a little more than just paying a monthly premium” advises Selwyn Kahlberg, Managing Director, Alexander Forbes Life Limited. For cover to remain valid, policyholders need to comply with all requirements in the policy. While this should not be a difficult task, Kahlberg urges consumers to be aware of the following pitfalls when taking out or maintaining a life and disability policy: 1. Failing to disclosure all relevant information on your application Deliberately withholding or giving misleading information to your insurer is a direct violation of your policy agreement. This can result in all claims being rejected. Policy holders should fully disclose any previous medical conditions when applying for life and disability cover. If, for example, you have suffered a heart attack and it re-occurs, your insurer may refuse to settle your claim if you did not inform them of the first attack. 2. Taking out insufficient cover Life cover is meant to provide financial security for your family when you die. Similarly, disability cover needs to ensure that you and your dependents are able to maintain your lifestyle should you not be able to perform your current job. As such, “it is important to draw up a budget reflecting your family’s daily needs and expenses when deciding on the level of cover required” advises Kahlberg. It is also important to continue to revisit your insurance requirements as circumstances change. At the very least you should take account of inflation to ensure that your benefits do not lose their purchasing power over time. 3. Not informing your insurer that you have changed jobs Changed employment terms can affect the cost and level of your cover. For example, if you were an office clerk and get a new job as a fire fighter, your risk level would increase substantially and your insurer would need to review your policy. 4. Failing to inform loved ones of your cover or whereabouts of documentation If you do not inform your loved ones about your life or disability cover, there is a possibility that they may never claim when the need arises. As such, it is “advisable to keep the policy in a safe place, telling loved ones where the policy is and who they should call in the event that it is needed” advises Kahlberg. 5. Failing to inform insurers of a claim within the required time Almost all policies require that claims are notified to the insurer within a specified time where after the claim can be declined. This is one of the most common reasons for claims not being paid. Dependants may forfeit their benefits if they delay telling the insurer about a claim or do not supply the required documents to the insurer within the times specified. 6. Not keeping the nominated beneficiaries up to date Always ensure that you let the insurer know about changes to the nominated beneficiaries on all your policies. Once a claim arises, the insurer will always pay according to what you last instructed them. For example, if you have had another child and want a specific amount set aside for it you will need to change the beneficiary forms held by the insurer. 7. Not providing full information when making a claim Always insure that the insurer is given as much accurate information and documentation as possible. This is especially the case on disability claims. Incomplete or conflicting information will cause delays in getting a claim paid. For example, “if you forget to provide your insurer with your dependents’ ID numbers, or supply incorrect or different numbers” warns Kahlberg. 8. Not disclosing that you have taken on additional risk, like smoking or engaging in dangerous activities Insurers charge higher premiums for individuals that smoke or are at higher risk of getting ill or dying.“If you sign on as a non-smoker and then start smoking and develop lung cancer, your insurer is within their rights to reduce your benefits or maybe even repudiate your claim” warns Kahlberg. Similarly, if you are disabled in a once-off parachute jump you will not qualify for disability cover if you have not listed this as one of your pastimes which the insurer has accept 9. Not familiarising yourself with the circumstances under which your policy will not pay There are times when a policy will not pay out even if you have made full disclosure to the insurer. “These circumstances should be clearly set out in your policy under the exclusions heading and you should take the time to understand these exclusions before signing up” recommends Kahlberg. Typical exclusions relate to alcohol consumption, drug usage, suicide and violation of the laws of the land. 10. Allowing your insurer to repudiate your claim without good reason Consumers should not sit back and allow insurers to repudiate claims except for valid and legal reasons. If you believe you have a strong case, yet your insurer refuses to settle, Kahlberg recommends that consumers take the matter to the insurance ombudsman. The ombudsman acts as a mediator to settle disputes between insurers and their clients and is an inexpensive alternative to litigation. Getting all this right is important as the onus falls on the insured to make sure that they understand all terms and conditions that they have been told about by the insurer when taking out a life and disability cover. The first step is to read all the documentation they receive from the insurer. “If you are unsure of any clause during the application process or anything in the policy wording once you receive the policy document you should ask your insurer to explain” concludes Kahlberg. Written by: Selwyn Kahlburg Source: Health24  If you wake up in the morning, look in the mirror and think, ‘Wow, my family is lucky to have me’ then congratulations, your self-esteem game is strong. But, many of us don’t tend to give it much thought. We take for granted that we’re able to spend time with and provide for our families. And this, in a nutshell, is the importance of life insurance.

If you had to stop and think about it, the feeling that comes with being able to look after your family and your dependants is pretty amazing. You get to show exactly how precious they are to you by keeping them safe and comfortable. But, life can be about as unpredictable as the quality of aeroplane meals, and you don’t know for sure that you’ll always be around to look after them. This is where life insurance comes in. Life insurance gives you a way to make sure that your dependants stay looked after if anything should happen to you (touch wood). A Closer Look at Life Insurance Life insurance is a type of insurance cover that pertains specifically to your life. Should you pass away unexpectedly while you are insured, your policy would pay a sum of money to your family. Essentially, you decide how much cover you need, and the length of time you might need it for. You then pay monthly premiums for the length of your policy. This gives you the peace of mind that comes with knowing that, if something should happen to you, your family would stay financially stable. Life insurance is exceptionally valuable if you have: Dependants If you have children or a partner relying on your income, life insurance is vital. This will let you enjoy your life with them without having to worry about what would happen if you were to pass away. It is also important to consider life insurance for your partner. The loss of an additional income or even the time contribution of a homemaker would certainly be felt. A Mortgage The last thing you would want is for your family not to have a place to stay if you were to pass. If you have a mortgage, a life insurance claim could pay this off, ensuring that your loved ones will always have a roof over their head. Life Insurance Means Total Peace of Mind When you wake up tomorrow morning, take a look in the mirror and think to yourself that your family is lucky to have you, and you’re lucky to have them, too. And, because of this, you should enjoy the time that you have with them and not spend a second worrying about how they would cope if you were to pass away. Get a quote for your life cover, please contact Kevin or Ray in our Life Department, email life@daberistic.com, tel (011)658-1333 Source: Hollard  The Smart Life Plan was designed with younger clients in mind by using an efficient and relevant product chassis with simplified benefit options. It offers comprehensive and dynamic cover that protects both your clients’ future lifestyle and their families’ financial security. The Smart PayBack Fund allows your clients to receive up to 100% of their qualifying Smart Life Plan premiums back for managing their health and wellness and practising good driving behaviour. Key issues faced by young professionals  The Smart Life Plan was designed with younger clients in mind by using an efficient and relevant product chassis with simplified benefit options. It offers comprehensive and dynamic cover that protects both your clients’ future lifestyle and their families’ financial security. The Smart PayBack Fund allows your clients to receive up to 100% of their qualifying Smart Life Plan premiums back for managing their health and wellness and practising good driving behaviour.

Unique features on Smart Life Plan

Smart Payback Fund Qualifying clients will accrue a minimum of 50% of their qualifying premiums annually towards their Smart PayBack Fund. The value of this Fund is automatically added to their Classic Life Plan PayBack on conversion (at age 30 or earlier through servicing) and is paid on their first policy anniversary at least five years after conversion. Clients can increase this accrual to up to 100% of their qualifying premiums by being healthy and driving well. UP TO 39% UPFRONT PREMIUM DISCOUNT By linking their Smart Life Plan to their other Discovery products, clients can receive an upfront premium discount of up to 39% through the power of Integration. Source: Discovery |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|