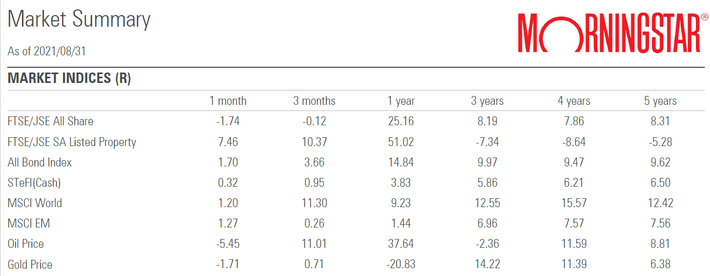

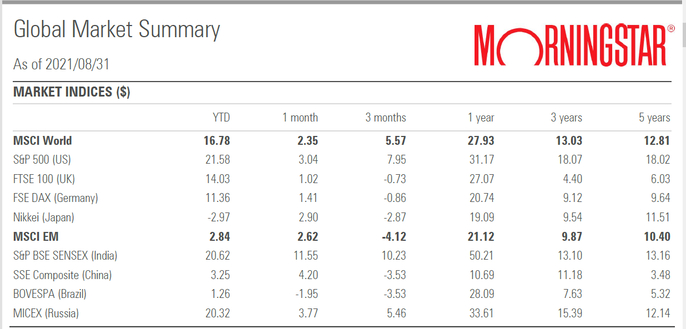

South African Market Commentary Global equity markets performed strongly in August, with many major global equity indices reaching new highs during the month, despite continued concerns around the spread of the highly contagious Covid-19 Delta variant across the globe. The US Federal Reserve (Fed) continued to allay fears of interest rate increases, with Fed Chair Jerome Powell reiterating his cautious stance at the Jackson Hole Economic Symposium held towards the end of August. Powell did concede, however, that the tapering of bond purchases is likely to start at the end of 2021. Powell’s dovish comments, as well as strong earnings updates from corporates, drove US equities to new highs, with the S&P 500 recording a seventh consecutive month of positive returns, its longest winning stretch since 2018. South African equities ended the month lower, as weak performance from Resource counters, as well as large index constituents Naspers and Prosus, weighed on the performance of the local equity index. Local bonds ended the month higher, as long dated nominal bonds delivered strong performance during the month and the nominal curve continued to flatten during August. Local listed property rebounded sharply in August, as sentiment towards the sector improved on the back of the move to an adjusted level 3 lockdown on 26 July and many REITs reporting better than expected recoveries from the riot damage caused by the civil unrest in July. The rand was stronger against most of the major developed market currencies, despite trading in quite a wide range during the month, in line with changes in global sentiment towards emerging market currencies. In terms of the Covid-19 response, the country remained on an adjusted level 3 lockdown, despite a decrease in the number of daily recorded infections during the month. Registration and vaccination for 18-34-year-olds opened on 20 August, with 12.6 million vaccines having been administered by the end of August. SA headline CPI moved lower to 4.6% year-on-year for July (from 4.9% in June), as fuel inflation continued to moderate, and SA inflation remained relatively muted due to weak pricing power in the local economy. SA’s trade balance came in at a surplus for August (R37 billion), following a revised surplus for July of R54 billion, as exports declined 11% month-on-month to R145 billion, higher than the 1% month-on-month decline in imports. StatSA’s periodic rebasing and reweighting of the national accounts data showed that the nominal size of the economy has increased by 11% from previous estimates, resulting in a lower-than-expected fiscal deficit and debt to GDP (71% at the end of 2020 compared with the previous estimate of 79%). Click here to read more  Global Market Summary Developed market (DM) equities had another good month, led by the major US Indices. The S&P500 and the Nasdaq reached record highs over the month with the former managing to close in the green for a seventh consecutive month. Economic data was supportive for the Financials sector at the beginning of the month as the 10-year US Treasuries rose on the back of a better than expected payrolls print. Despite a weaker than expected retail sales print and a resurgence in Covid-19 cases as a result of the Delta variant, markets still managed to power ahead on the back of bullish remarks from Fed chair Jerome Powell at the Jackson Hole symposium. Although Powell raised the possibility of tapering this year, he also highlighted that this should not be viewed as the start of the hiking cycle. He also reinforced the fact that the Fed would continue to tolerate higher inflation in pursuit of further labour market gains which served as support for the markets over the month. Click here to read more   South African Market Update South African equities ended higher for a sixth consecutive month, despite poor performance from large industrial counters including Naspers, Prosus and British American Tobacco acting as a headwind to the performance of the local equity index. Local bonds ended the month higher, supported by a stronger rand over the month and outperforming both aggregate developed and emerging market bond indices. Local listed property had a strong month, as the asset class continues its recovery amid the local economy returning to more normal levels of activity post the Covid-19 induced lockdown at the beginning of the year. The rand was largely stronger against most major developed market currencies over the month, receiving continued support from the positive trade balance caused by higher commodity prices and subdued imports. South African Economic Update Following weak economic data in January due to the Covid-19 induced restrictions, trade data for February (which was released in April) rebounded strongly. Wholesale and retail trade recorded month on month increases of 1.3% and 6.9%, after falling -0.9% and -2.4% respectively in January. SA’s trade surplus widened to R52.8 billion in March (from R31.2 billion in February), which is the widest surplus on record and continues to provide significant support to the rand, one of the best performing emerging market currencies year to date. SA headline CPI moved higher to a year-on-year figure of 3.2% for March (from 2.9% in February). Local inflation continues to surprise on the downside, however, inflation is expected to rise further over the next few months, largely due to base effects and higher international prices.  Global Market and Economic Update Global equity markets continued to climb higher in April, supported by surprises in terms of positive economic data and company earnings releases. As at the end of April, 87% of S&P 500 companies have posted Q1 2021 earnings which beat estimates, with earnings growing by an average of over 46% year on year. US President Joe Biden addressed a joint session of Congress during the month, motivating for a $2 trillion infrastructure plan and a newly unveiled $1.8 trillion plan for families, children, and students. President Biden is proposing that the American Families Plan is largely funded by additional tax of $1.5 trillion on the top 1% of earners as well as increased levies on capital gains and ordinary income for those earning more than $400,000 a year. The US is expected to reach its pre pandemic level of output midway through 2021, with record stimulus packages and low interest rates providing significant support to aid economic recovery. The positive moves in global equity markets came despite uneven Covid-19 vaccine distribution across developed and emerging markets, with many key emerging markets struggling to source and distribute vaccines, leading to spiking infection rates in certain countries (particularly India and Brazil).  Source: Morningstar

Tammy Hua, one of our team members, shares her personal experience of investing with Easy Equities.

What can you buy through Easy Equities?

How much fees and brokerage do they charge?

How does Easy Equities help you invest?

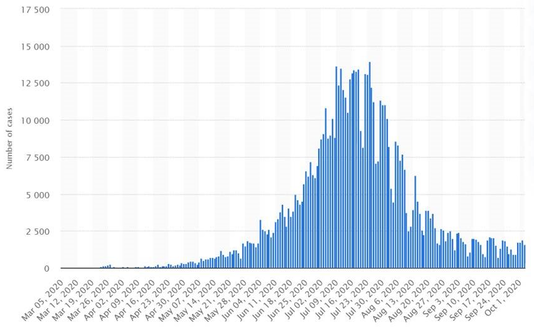

South African Market Update South African equities tracked global markets lower during the month, weighed down by poor performance from some large industrial and resource shares, despite strong performance from the local banking sector. Local bonds ended the month largely flat, as appetite for emerging market debt remained subdued, despite the attractive yields on offer. Local listed property continued to face headwinds from uncertainty regarding earnings and distributions, which has deterred investment in the asset class due to the historical reliance on income as a source of return. The rand was stronger against most major developed market currencies for the month, which detracted from the contribution of the performance of global asset classes. South African Economic Update South Africa moved to a level 1 lockdown on 21 September, as daily local Covid-19 infections continued to decline during the month and the recovery rate improved to a figure of around 90%. SA’s Q2 2020 GDP data was released during the month, indicating that GDP fell 17.1% year-on-year for the second quarter, as the hard lockdown took its toll on the local economy. South African Reserve Bank Governor Lesetja Kganyago announced that the Monetary Policy Committee has decided to leave the repo rate unchanged at 3.5%. The decision by the MPC was split, with 2 of the 5 members favouring an interest rate cut. SA headline CPI fell to a year-on-year figure of 3.1% to the end of August (from 3.2% in July), close to the bottom end of the target range of between 3% and 6%. Chart of the month: Daily confirmed Covid-19 cases continued to fall in South Africa during the month as the country moved to a level 1 lockdown. (Source: Statista)  See below for a summary of the key market movements for the month of September:

Please click on the links below to download the Market Summary PDF and the Market Commentary PDF, intended to be ‘end investor friendly’ Morningstar Market Commentary SA September 2020.pdf 2020_09_Morningstar Market Summary.pdf *All data is sourced from Morningstar Direct as at 30/09/2020. The performance of South African asset classes is quoted in rands and the performance of global asset classes is quoted in US dollars. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|