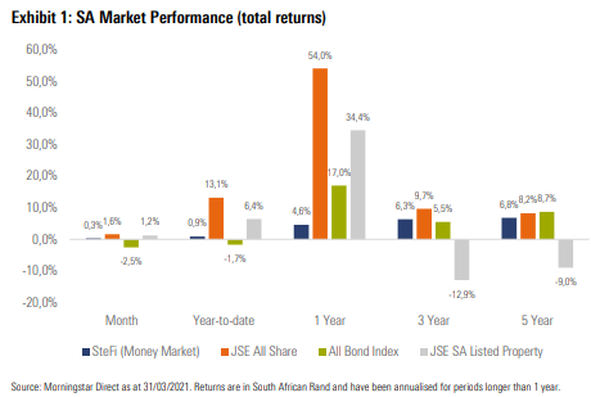

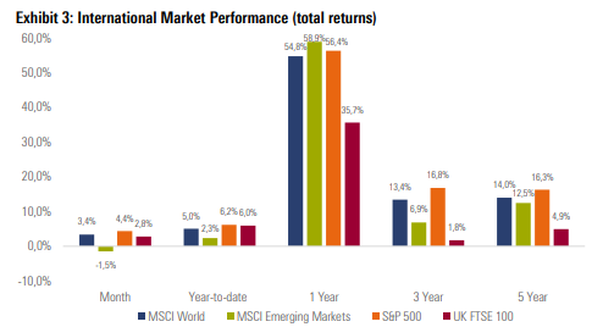

South African Market Update South African equities ended higher for a fifth consecutive month, with positive performance across all three major local equity sectors. Local bonds ended the month lower, despite positive news on lower-than-expected inflation, a reduction in government bond auctions, a lower-than-expected budget deficit and a stronger rand. The weak performance from bonds was largely driven by SA yields drifting higher (moving prices lower) in reaction to movements in global bond markets. Local listed property ended the month higher, however, weak performance from some of the larger counters including Growthpoint and Redefine led to muted returns from the SA Listed Property Index. The rand was stronger against most major developed market currencies, despite weakening significantly against the US dollar at the beginning of March, only to recover the lost ground towards the end of the month. South African Economic Update The South African Reserve Bank’s Monetary Policy Committee (MPC) announced during the month that it will leave the repo rate unchanged at 3.5%. This was the fourth consecutive meeting where the MPC decided to leave the rate unchanged, however, unlike recent meetings, the decision was unanimous, with all five members voting to keep rates on hold. Available data for Q1 2021 appears to indicate a slow start to the year for economic growth, which can largely be attributed to the introduction of adjusted level 3 lockdown restrictions during January in reaction to the second Covid-19 wave in the country. SA headline CPI moved lower to a year-on-year figure of 2.9% for February (from 3.2% in January). This was only the third time in over a decade that year-on-year inflation has fallen below the bottom end of the target band and was largely driven by the contribution of lower medical insurance costs.  Global Market and Economic Update Most major global equity markets ended the month with positive returns, as economic data reflecting the recovery from the Covid-19 pandemic continued to surprise on the upside. Equity investors continue to remain bullish, with another US stimulus package on the horizon, despite concerns around a ship stuck in the Suez Canal, which disrupted a major global shipping route for a few days during the month. March was dominated by market participants taking note of movements in global bond markets, as yields continued to move higher (moving prices lower), led by US Treasuries, as global bonds ended the quarter with their worst return in decades. The uptick in global bond yields appears to be connected to inflation expectations, with fixed income markets pricing in higher inflation in the medium term, which is likely to lead to interest rate increases from the US Federal Reserve (Fed). This, despite the Fed’s insistence that they will continue to keep monetary policy accommodative as the US economy continues its recovery from the shock of the Covid-19 pandemic.  Source: Morningstar

0 Comments

What is it:

It is a tax-free investment account. You can invest up to R36,000 a tax year into the account. You can do this for yourself, your spouse and your children. All your contributions, investment growth and interest in the account, and withdrawals are tax free, for life. You may withdraw at any time, although it is recommended that you invest for the long term (5 years +). You can contribute up to R500,000 in your lifetime. What is this product suited for? You may consider investing using this product if: you wish to save up to R36,000 per year, or up to R3,000 per month you wish to invest for your child's education fund you wish to supplement your pre-retirement savings you wish to pay no tax on your investment What is this product not for? It is not a transactional account. It is not for short-term investment What are the investment options? Allan Gray offers the Allan Gray Tax-Free Balanced Fund, which is a good option for most investors. We as a Financial Advisor can use external fund managers to put together a portfolio of funds for our clients. We currently recommend the Morningstar TFSA Portfolio. What are the costs? This is the part where it can be difficult to make sense of. Fund managers of the funds you invest in charge fund management fees. The Total Investment Charge (TIC) is expressed as a percentage. Allan Gray as a LISP (linked investment service provider) charges a platform fee of 0.58% per annum, this is deducted monthly, calculated on the account balance. A financial advisor charges an initial advice fee and an annual advice fee for the advice and services rendered. Why do we recommend Allan Gray Tax-Free Investment? 1. Reputable asset management company; 2. Financially sound; 3. Efficient administration platform; 4. Clever use of technology delivers excellent user interface; 5. Excellent staff delivers excellent client service; 6. Competitive platform administration cost; 7. Reduced admin fee for using Allan Gray funds; 8. Select range of good performing unit trusts; 9. Easily creates customisable, informative investment overview; 10. May nominate beneficiaries on the investment; 11. Enables clients to submit instructions online. To find out more how you may benefit from this investment, or to start such investment, please contact Kevin Yeh, email service@daberistic.com.  Around this time of the year, we would like to remind you to consider topping up your retirement annuity fund and tax-free investment.

Retirement Annuity According to the current legislation, you may contribute up to 27.5% of your taxable income (strictly speaking, non-retirement funding income) to a retirement annuity fund and enjoy tax deductions. As 28 February is the end of the tax year, you must calculate and pay the additional amount to your retirement annuity prior to this date, in order to qualify for tax deductions and tax refunds. Below is an example of topping up your retirement annuity: Ms Rama has a monthly salary of R80,000. In December she received a bonus of R100,000. Every month she contributes R5,000 to a personal retirement annuity fund. Her annual income is then R80,000*12 + R100,000 = R1,060,000. The maximum tax-deductible contribution to retirement annuity is R1,060,000 * 27.5% = R291,500. Over the year she has contributed the following to a retirement annuity fund: R5,000 * 12 = R60,000 The additional amount she may top up in his retirement annuity (RA) is R291,500 Less R60,000 = R231,500 Tax-free investment You may contribute up to R36,000 to a tax-free savings account in a tax year. You must calculate how much you have contributed so far since 1 March 2020 and pay the additional amount to your tax-free savings account prior to 28 February, in order to make use of current tax year's allowance. You can also start a tax-free investment in the name of your children. To top up your retirement annuity or tax-free investment, please contact service@daberistic.com  Around this time of the year, we would like to remind you to consider topping up your retirement annuity fund, or contribute to a tax-free savings account. It's perfectly legal. Save money for yourself, instead of giving to the taxman.

Such tax savings can amount to tens of thousands of Rands. Retirement Annuity According to the current legislation, you may contribute up to 27.5% of your taxable income to a retirement annuity fund and enjoy tax deductions. As 28 February is the end of the tax year, you must calculate and pay the additional amount to your retirement annuity prior to this date, in order to qualify for tax deductions and tax refunds. Below is an example of topping up your retirement annuity: Mr Mabasa has a monthly salary of R50,000. In December he received a bonus of R100,000. Every month he contributes R3,000 to a personal retirement annuity fund. His annual income is then R50,000*12 + R100,000 = R700,000. The maximum tax-deductible contribution to retirement annuity is R700,000 * 27.5% = R192,500. Over the year he has contributed the following to a retirement annuity fund: R3,000 * 12 = R36,000 The additional amount he may top up in his retirement annuity (RA) is R192,500 - R36,000 = R156,500 He can look to get a tax refund of R192,500 * 39% = R75,075. Attached is a document from Allan Gray summarising the differences between an RA and a tax-free investment. minimise-your-taxable-income_maximise-your-tax-savings---ra_tfi.pdf Speak to your Financial Advisor if you would like to exercise one of the two options, or email invest@daberistic.com.  We have all had our moments where we were convinced that our opinion on a particular subject was absolute, and no one or nothing could convince us of anything else… until we were proven wrong.

For years as a young boy, I believed that the title of a certain ABBA hit was “Jackie Chan”. I sang my heart out: “If you change your mind, Jackie Chan, I’m the first in line, Jackie Chan.” Many years later, and much to my embarrassment, I found out that my version of the song was completely wrong and that the actual title was “Take A Chance”. People often make the same mistakes when it comes to investments. They only hear snippets from a “song” and then proclaim their version to be the absolute truth. With this in mind, let’s take a look at one of South Africa’s latest investment hits, the tax-free investment, and how investors don’t quite have the lyrics down just yet. 1. “I don’t like to be restricted. What if I’m not happy with my financial provider in a year or so?” When tax-free investments were launched in March 2015, this person’s concern would have been more than valid, because you were unable to transfer your tax-free investment to another provider. Since 1 March 2018, however, regulation has become more flexible, allowing investors to transfer either the full tax-free investment, or a portion thereof to another financial services provider or providers (limited to a maximum of two transfers per year), without losing any of their benefits. This means that if another financial provider offers you the same investment option at a better price or product offering, you are free to switch all or part of your investment to that provider. 2. “I don’t plan to sell anyway. Aside from no capital gains tax, the product doesn’t really offer any other benefits.” This investor couldn’t be more wrong. Yes, tax-free investments are exempt from capital gains tax (CGT), but those aren’t the only words to the song. Whether you buy with the intention to sell or not, the benefits of tax-free investments do not end with CGT. You also do not pay any income tax or dividend withholding tax (DWT) over the entire span of this investment’s lifetime, and those benefits are bigger than investors may think. As an example, let’s suggest that investors A and B both invested R33 000 (the current allowed annual maximum contribution to a tax-free investment, and R500 000 maximum contribution in total per lifetime) per year over a period of 15 years in a tax-free investment. Investor A’s personal income tax rate is 28% and person B’s personal income tax rate is the maximum of 45%. To illustrate the benefits of the exemption of DWT, let’s suggest that both investors invested the full amount each year in the FTSE/JSE All Share Index (JSE). The total average return on the JSE over the past 15 years was 17% a year. Of this 17%, 3% in returns came from dividends, which means that at the current DWT rate of 20%, you could have earned an additional 0.6% per year in returns if you had followed the tax-free investment route. To illustrate the income tax benefits of this product, let’s suggest that both investors A and B invested the full R33 000 a year in the FTSE/JSE SA Property Index (SAPY) over the same 15-year period. If they had done so directly 15 years ago (by applying current tax legislation), investor A would have earned (after their income on interest were taxed) R35 600 less, while investor B would have earned R57 200 less. Percentage-wise, based on the total original contribution of R495 000 over this 15-year period, investor A would have earned 7.2% less on their investment, and investor B would have earned a whopping 11.6% less. 3. “CGT doesn’t make such a huge difference when considering the bigger picture.” Investors who believe this, aren’t only getting the words wrong, but are completely out of tune. CGT makes a massive difference. Let’s use the example of investors A and B again, their respective personal income tax rates, and the growth earned on the FTSE/JSE All Share Index over the past 15 years. Take note that tax-free investments were not available 15 years ago, and if both investors invested their annual R33 000 in the JSE, their investments would have grown to more than R1.6 million in total after 15 years. The problem is that that by applying current tax legislation, if they needed to sell, investor A would have paid R127 000 (8% of investment total) in CGT, while investor B would have paid R204 000 (13% of investment total) in CGT. If tax-free investments were available 15 years ago, they would have been able to sidestep the entire CGT charge today, so clearly the difference is very big. As with any financial product, it’s always important to do your homework and to make 100% sure that the product you choose will satisfy all of your investment needs. I believe that tax-free investments will remain one of those investment hits that will keep investors singing along for many years to come. If you are one of them, just make sure that you know the (right) lyrics. To get more information on Tax Free Savings , please contact Kevin or Ray, email: invest@daberistic.com tel no: (011 658-1333) Written By : Schalk Louw Source: Finance 24  The end of February is the end of the tax year. Carla Rossouw explains why this is a good time to take maximum advantage of the incentives the government has put in place to encourage us to save.

There are certain annual tax benefits available for you through your retirement fund and tax-free investment (TFI) account. You forfeit these if you don't act each year. As we approach the end of the tax year (28 February), it is worthwhile looking at your finances. If you have cash to spare, consider taking full advantage of the tax incentives. Individuals are allowed to invest R33 000 per year up to a lifetime maximum of R500 000 in a TFI account. Like a retirement fund, you benefit from growth free of dividends tax, income tax on interest and capital gains tax - a big win if you invest for the long term. In terms of flexibility, TFIs are similar to unit trust investments, but your return potential is higher than in a basic unit trust, as you can see in Graph 1, which shows the impact of tax over 10 years. The red line illustrates the 10-year return of the Balanced Fund, while the black line reflects the return an investor would receive after tax - although of course this differs for everyone as it is based on your personal tax rate and circumstances. The catch is that if you exceed the maximum investment amount in a TFI, the tax penalties are high. To top up or open up a Tax Free Savings account , please contact Kevin or Ray, email: invest@daberistic.com tel no: (011 658-1333) Source: Allan Gray  In March 2015 the then Finance Minister Nhlanhla Nene introduced Tax-free Savings Account, to incentivise the general public to save money. Any South African with a 13-digit ID number can invest in a tax-free savings account, with an annual maximum of R33,000 in a tax year and a lifetime contribution of R500,000.

All growth in your Tax-free Savings Account is completely tax-free. No capital gains tax, no dividends tax and no income tax from interest earned… ever! Withdrawals from your tax-free account are tax free. You may access your money at any time without penalty. Government stipulates that products are simple to understand, adequately transparent and suitable for investors. No performance fees are allowed. Most financial institutions offer Tax-free Savings Account: banks, life insurance companies, fund managers, investment platforms and JSE stockbrokers. Return profile: If it is a bank deposit product, you may get an interest rate of between 5% and 7%. If the underlying investments are unit trusts, it will depend on the type of unit trust you invest in. Who is it suitable for:

A word of advice: I consider Tax-free Savings Account to be the third Financial Wonder in South Africa. You should use Tax-free Savings Account as a long-term investment vehicle (10-years plus), using unit trusts with highest long-term expected return (such as Offshore Unit Trusts) as underlying investment. This way you will truly benefit from a Tax-free Savings Account. Don’t use Tax-free Savings Account as a normal savings account or transactional account. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|