|

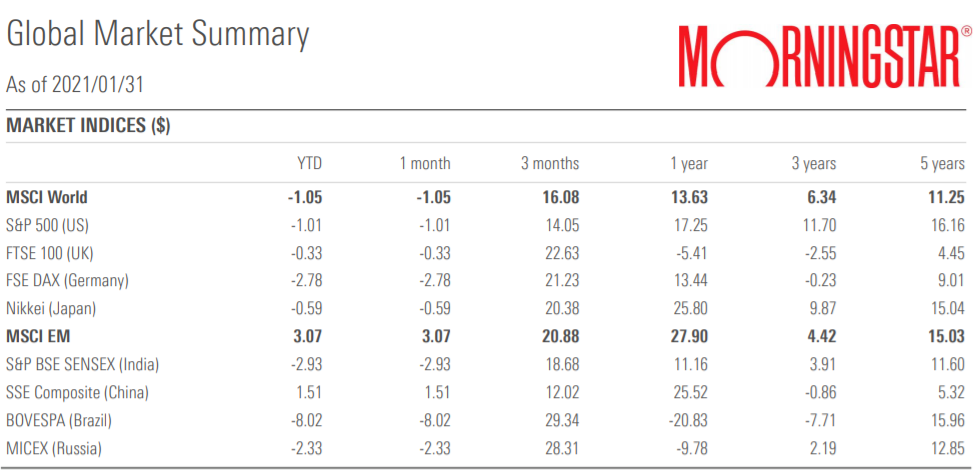

MARKET COMMENTARY The first month of 2021 proved to be very eventful for investors, with the news flow at the beginning of the month dominated by political headlines in the US as former president Donald Trump became the first US president to be impeached twice. This was after a group of Trump supporters stormed into Capitol Hill following “inciteful” tweets by Donald Trump in a bid to stop Congress from confirming Joe Biden’s electoral victory in the recently concluded presidential elections. The US political system, however, proved its resilience as lawmakers heavily condemned this behaviour and subsequently confirmed Biden’s victory which led to a successful inauguration which saw him become the 46ᵗ president of the United States. The month also saw the Democrats secure the two seats that they needed to control the senate in the Georgia run-off elections. These developments further increased investor expectations for additional stimulus by the new administration. The bond market reflected these expectations as yields on the benchmark US 10-year Treasury note rose above 1% for the first time since the pandemic started as the market priced-in expectations of higher future inflation on the back of the anticipated stimulus. In other news, “GameStop mania” overshadowed the developments on the vaccine roll-out front in the latter part of the month as market participants processed these developments. GameStop Corp is a struggling bricks and mortar video game retailer that is facing structural changes within its core market which had initially led to significant short positions on its stock by hedge funds in anticipation of an eventual demise. Retail investors, so called “Redditors” sparked a 1600% rally in the stock as they sought to bet against the big hedge funds via online trading platforms such as Robinhood. Frenzied buying amongst retail investors triggered a wave of “short covering” by institutional investors which further fuelled the stock’s rally, until online brokers stepped-in to impose restrictive limits on trading the stock. Moving over to market performance, returns were mixed, with the S&P 500 (-1.0%) ending the month lower and the NASDAQ 100 (+0.3%) managing to stay in the green amongst the major US equity indices. In Europe, the UK’s FTSE 100 (-0.3%) and Germany’s FSE DAX (-2.8%) both ended lower. Japan’s Nikkei 225 (-0.6%) followed other DM’s (developed markets) equities lower whilst China’s Shanghai SE Composite (+1.5%) ended on a positive note. EM’s (emerging markets) outperformed DM’s, with the MSCI Emerging Markets Index (+3.1%) ending the month on a strong footing on the back of positive performance by Asian EM’s such as China. Overall, the MSCI World Index delivered a return of -1.0% for the month, driven mostly by the poor performance across DM equities. Gold (-1.3%) gave up some of its gains from the previous month whilst Platinum (+10.0%) ended the month on a much stronger footing. Oil (+7.9%) followed up on last month’s performance with another positive showing. The US dollar was largely stronger against most of the major currencies for the month, appreciating against the Japanese Yen (+1.4%) and the euro (+0.7%), however, the greenback was weaker against the pound sterling (-0.5%).  *All data is sourced from Morningstar Direct as at 31/01/2021. The performance of global asset classes is quoted in US dollars. Source: Morningstar

0 Comments

Leave a Reply. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|