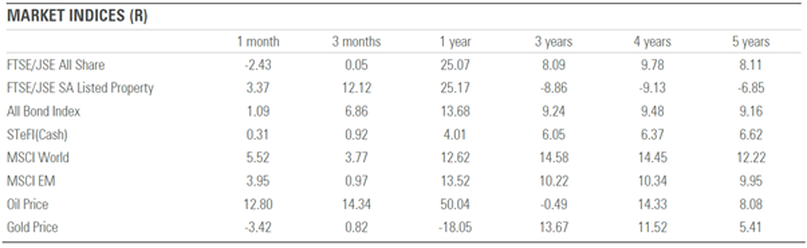

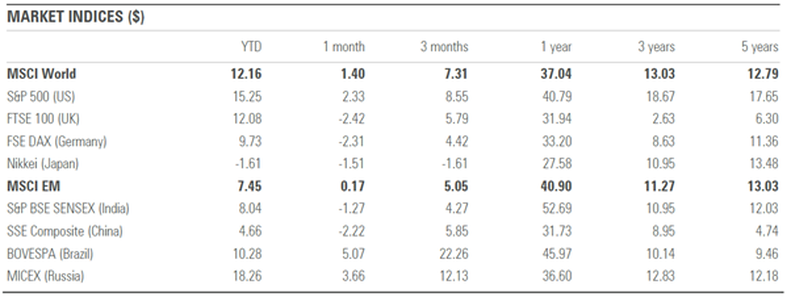

South African Market Update Most major global equity markets ended the month with either modest gains or in negative territory, as concerns around the rapid spread of the Covid-19 Delta variant spooked investors. That said, the vaccination drive in developed markets, particularly the UK and the US continued, with between 50-60% of the population in these regions at least partially vaccinated. The US Federal Reserve (Fed) met during the month and kept interest rates unchanged, however, its 2021 calendar year inflation forecast moved slightly higher. What surprised some market participants was the slightly more hawkish tone from the Fed, as they signalled that there could be two interest rate hikes in 2023, with the first hike expected in Q3 2023 (slightly earlier than the original early 2024 estimate). The Fed’s preferred measure of inflation, core personal consumption expenditure (PCE) moved higher to a year-on-year figure of 3.4% in May (the highest increase in prices since 1992) from 3.1% in April. The Fed has continued with its rhetoric that these price pressures are driven by supply bottlenecks and the reopening of the economy and are, therefore, transitory.  South African equities ended the month lower for the first time in eight months (since October 2020), as disappointing performance from resource counters (gold counters in particular) weighed on the performance of the local equity index. Local bonds ended the month higher, despite foreign selling (foreigners sold R14.2 billion of SA bonds in June) and a weaker rand acting as a headwind to the performance of the asset class. Local listed property delivered strong performance for the month, despite giving up some gains towards the end of June on the back of concerns around further Covid related restrictions. The rand reversed some of its recent impressive run, ending the month weaker against most major currencies as hawkish comments from the Fed proved supportive of the performance of the US dollar. South African President Cyril Ramaphosa announced that the country will move to an amended level 4 lockdown (effective from the 28th of June) which includes restrictions on alcohol sales, prohibiting indoor and outdoor gatherings and an extension of the overnight curfew. The harder lockdown measures come on the back of a surge in Covid-19 infections across the country as a result of the highly contagious Delta variant. SA headline CPI moved significantly higher to a year-on-year figure of 5.2% for May (from 4.4% in April), as the base effects of higher fuel and food prices filtered through to the inflation print. SA’s trade balance came in at a surplus for May (R55 billion), following a revised surplus for April of R51 billion, as exports increased 1.5% month on month and imports retreated slightly. The JSE All Share Index (-2.4%) ended lower for the month, as a stronger US dollar acted as a headwind to the performance of major commodity counters. Local equity sectors had mixed performance for the month, with Industrials (+0.4%) outperforming both Financials (-3.0%) and Resources (-6.4%). The top performing shares amongst the largest 60 companies on the JSE in June were Foschini Group (+20.0%), Exxaro (+9.5%) and Bid Corp (+6.6%). The worst performing shares in June were Harmony Gold (-28.7%), Gold Fields (-26.0%) and Anglogold Ashanti (-22.0%). Listed property (+3.4%) had a strong month, as positive performance from large index constituents including Growthpoint (+3.1%) and Redefine (+3.4%) acted as a tailwind for the performance of the local property index. Local bonds (+1.1%) ended the month higher, as the nominal yield curve continued to flatten during the month in reaction to the market pricing in expectations of future interest rate hikes. Cash delivered a stable return of +0.3% for the month. The rand was weaker against most major developed market currencies for the month. The rand depreciated against the US dollar (-3.9%), the euro (-0.9%) and the pound sterling (-1.1%) over the month. Click here to Read more Global Market Summar  June marked the end of the first half of 2021, with most major global equity markets managing to end on a positive footing. Within the US, the S&P 500 closed at a record high 4 297.50 points, registering a fifth consecutive monthly gain as well as its best first half performance since 2019. On the vaccination front, little was changed with regards to the divergence between developed market (DM) and emerging market (EM) vaccination rates. DM’s continued to show further progress relative to EM’s, with data showing that the US has now inoculated over 60% of its population, up from 50% in the previous month.

With regards to economic data, June soft and hard data continued to point towards a continued recovery. The US labour market continued to show signs of growth, with June’s non-farm payrolls coming in at 850 000, ahead of Dow Jones economist expectations of 706 000. More importantly, however, was the unemployment rate, that rose to 5.9% relative to market expectations of 5.6%, suggesting that there is scope for the Fed to continue with its support of the labour market. Consumer confidence as measured by the Conference Board also came in ahead of market expectations, recording a 16-month high of 127.3 points. This survey data places more emphasis on the labour market and June’s reading pointed towards an increase in durable goods demand and home purchases. On the inflation front, Core PCE (the Fed’s preferred inflation measure) came in at 3.4% year over year, but the real action was in the breakeven market, where both the 5-year and 10 year numbers have been trending lower, suggesting that the market could be re-calibrating its longer-run inflation expectations lower. The Fed’s quarterly forecasts suggested that it now has more members that expect inflation to surprise to the upside. There are now seven members (from four) out of eighteen that prefer an interest rate rise in 2022 and the median member also now expects at least two interest rate hikes in 2023 relative to past expectations that 2024 would be the starting point for any interest rate hikes. Against this backdrop, longer-term US rates dropped, resulting in a flattening of the US yield curve which suggests that the market interpreted the Fed’s comments as growth negative. Within equities, Financials sold-off as they bore the brunt of the flatter yield curve as they generally borrow on the short-end of the curve and lend on the longer-end of the curve. Click here to read more

0 Comments

Leave a Reply. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|