|

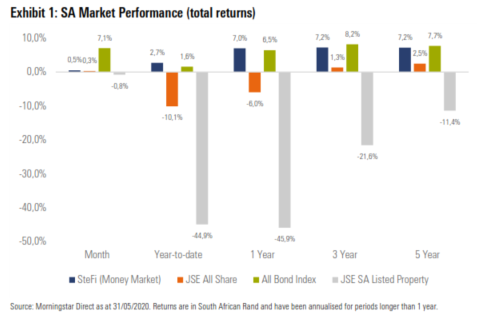

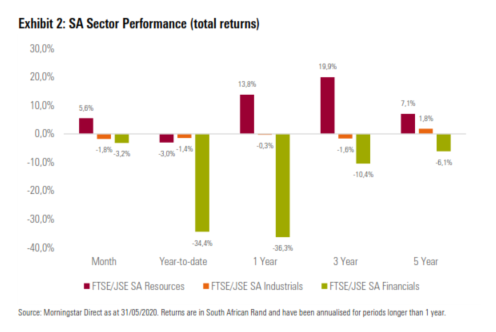

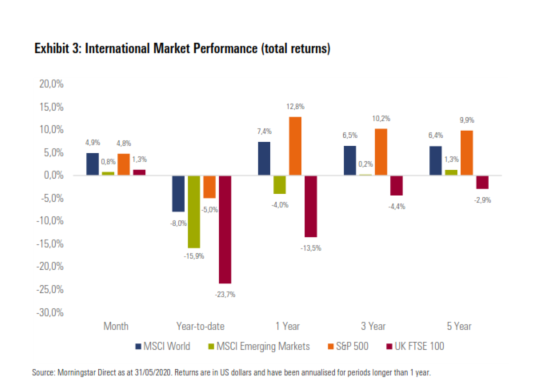

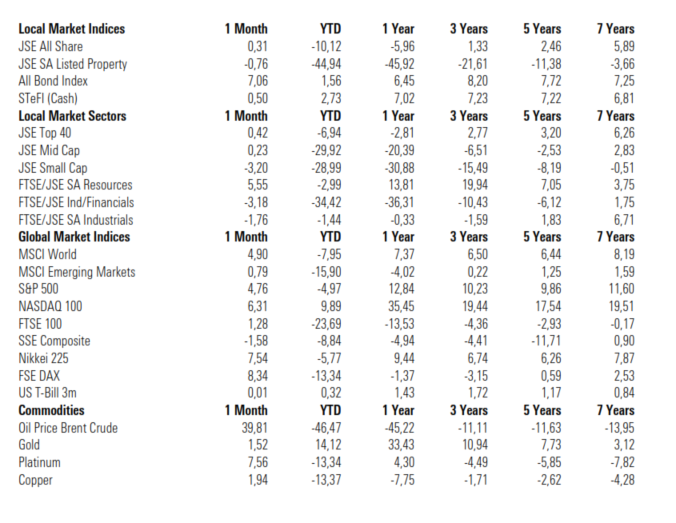

Global markets continued to climb higher in May following a strong rebound in April, as investors reacted positively to the news of many economies reopening following the Covid-19 induced lockdowns. The positive performance generated by most global equity markets came despite concerns around a possible second wave of infections and political tensions between the US and China, initially around Covid-19 and later around Beijing’s treatment of Hong Kong. Economic data continues to show signs of the damage caused by the Covid-19 pandemic, with forecasts indicating that the US economy lost another 8.3 million jobs in May, following the 20.5 million lost in April. This would push the US unemployment rate to close to 20%, after it ended April at a level of 14.7%.  South African equities ended the month largely flat, however, there was significant dispersion among the index constituents during the month. Platinum group metals counters (PGM’s) and diversified miners delivered strong performance during the month, however, this was offset by continued weakness in banking and financial counters. Local bonds were the standout performer during the month in terms of local asset classes. Yields continued to fall dramatically during May (moving prices higher), as the asset class delivered its best monthly performance since July 2008. Local listed property continued to struggle during the month as the benefit of lower interest rates appeared to be offset by tenants struggling to deliver on contractual rental obligations. The rand was significantly stronger against most major developed market currencies during the month, recovering some lost ground following significant depreciation since the start of the year. The Governor of the South African Reserve Bank (SARB), Lesetja Kganyago, announced another reduction in the repo rate of 50 basis points during May, bringing the rate to a record low of 3.75%. President Cyril Ramaphosa announced the re-opening of some sectors of the economy under Level 4 lockdown restrictions and also announced that the country will move to Level 3 from the 1 st of June, which will allow many businesses to return to full operation. Local equity sector performance was mixed, with Resources (+5.6%) delivering strong performance, while Industrials (-1.8%) and Financials (-3.2%) fared slightly worse.  Most major developed equity markets ended the month higher, as investors welcomed the reopening of many global economies post the lockdowns in countries around the world. The MSCI World Index delivered a return of +4.9% for the month. Emerging market equities managed to deliver positive performance for the month, however, returns were slightly more muted than those in developed equity markets. The MSCI Emerging Markets Index delivered a return of +0.8% for the month. Most major equity markets ended the month with strong returns, with Germany’s FSE DAX (+8.3%), Japan’s Nikkei 225 (+7.5%) and the UK’s FTSE 100 (+1.3%) ending the month higher. China’s Shanghai SE Composite (-1.6%) bucked the global trend, ending the month lower. US equities also ended the month higher, with both the NASDAQ 100 (+6.3%) and the S&P 500 (+4.8%) both delivering strong returns.  Impact on client portfolios Most portfolios ended May with positive returns, largely driven by strong performance from the SA bond market as well as continued strength in global equity markets. Rand strength during the month against major developed market currencies did detract slightly from the positive contribution from global exposures. Income focused investors received decent returns from portfolios during the month, as local bond allocations drove positive performance during May. What is apparent is that despite global economic data showing strain from the impact of the global lockdowns, markets appear to be reacting positively to the gradual opening of industries across the world. The significant amount of monetary and fiscal stimulus announced by governments and central banks has also provided significant support to global markets. We will continue to follow a disciplined valuation driven approach in managing client portfolios, with risk management currently more important than ever given the noisy market environment. Click here to download market performance

0 Comments

Leave a Reply. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|